Currently, Boeing (BA) is perhaps one of the most complex assets available for purchase. If you look exclusively at valuation multiples, then your first reaction will be the desire to forever close out this ticker. The company is a synonym of corporate disaster: its book value collapsed into a deep negative zone, its net debt is huge, and its multi-year losses force investors to doubt the very viability of the business.

On the chart above you can easily see how a cascade of crises destroyed the capitalization of the company. At the current price around $195 and a market capitalization of $148.5 billion, Boeing trades on levels that reflect the maximal fear of investors.

But sometimes financial reports act simply as a rear-view mirror. They fixate on past catastrophes but do not speak to what is happening in the assembly shops today. Right now, Boeing’s physical production contradicts its financial accounting.

And exactly on this border of fear and reality opens a unique opportunity for long-term investors.

In the beginning of 2026, Boeing unexpectedly bypassed its competitor Airbus (EADSY) by delivery rates, having transferred to customers 46 commercial aircraft against 19 from Airbus.

This is not simply a statistical anomaly of one quarter. This is the first powerful signal that Boeing has finally broken through the multi-year production, regulatory, and certification blockade. In order to understand the scale of the upcoming turnaround, investors must understand how the company found itself in this deep hole and how it began to exit.

The Trap of Perfection: How Did Boeing End Up ‘On Pause’?

Many investors do not understand the real reasons behind the drawn-out Boeing crisis, writing off everything onto an abstract “bad management.” The root of the problem lies much deeper — in the very nature of modern aviation engineering and how regulators react to it.

Airplanes of past generations, such as the legendary Boeing 747, were, figuratively speaking, “robust.” Into their construction was laid down a giant reserve of strength, backlashes, and mechanical duplications. A millimeter gap in the skin or an insignificant deviation in dimensions was not a critical problem for those standards. Modern liners though — like the 787 Dreamliner or new modifications of the 737 MAX — these are the peak of technological optimization. They are brought to absolute engineering perfection for the sake of extreme economy of weight and fuel.

But this perfection requires true flawlessness. Even a microscopic deviation from the ideal (for example, those very “microscopic gaps” in the docking of carbon sections of the fuselage of the 787), which earlier nobody would have noticed, today are perceived by regulators (FAA, EASA) as a potential risk. Due to the tragedies of 2018-2019 years with the 737 MAX, aviation authorities began to study Boeing’s airplanes literally under a microscope.

As a result, regulators simply stopped whole production programs and introduced harsh limits on release. Boeing found itself in a situation where it had colossal demand from airlines but for years did not legally have the right to assemble and deliver airplanes in the needed volume.

These regulatory and certification hurdles, and not the absence of buyers, burned the book value of the company.

Turnaround Is Confirmed by the Numbers

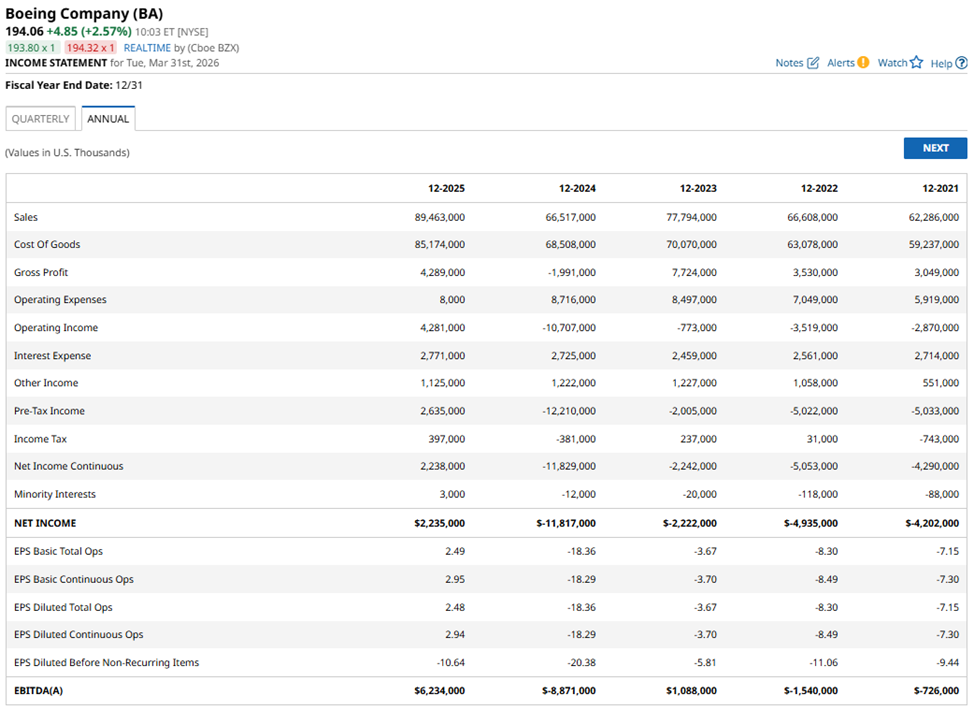

If we look at actual financial tables from Barchart, we will see a confirmation of our thesis: the company began to pass the bottom.

Yearly data shows us a catastrophic 2024, when the company reported a yearly loss of $11.8 billion at a gross loss of $1.991 billion. This was the bottom of the crisis of deliveries. However, look at the results of 2025: revenue grew to $89.463 billion, and gross profit became positive — +$4.289 billion. The company finally began to generate profit from operational activity.

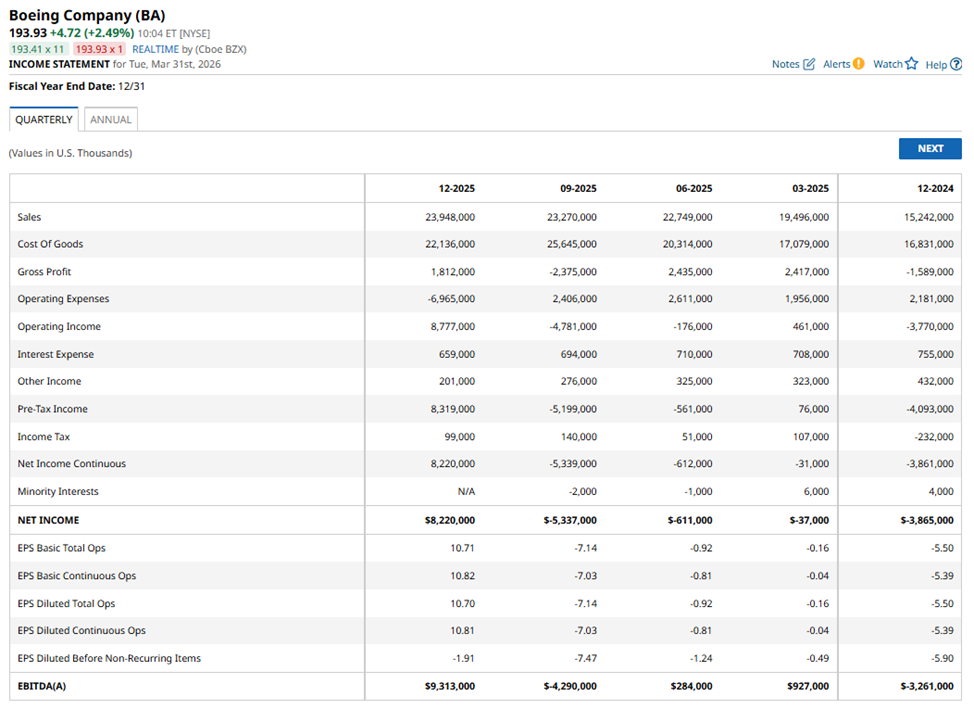

Quarterly data show how this occurred. We see volatility. After the failure of gross profit in the third quarter of 2025 to -$2.375 billion, the company performed a sharp rebound in the fourth quarter, delivering +$1.812 billion of gross profit. This is a brilliant confirmation that the production rhythm is restoring itself.

Macroeconomic Emptiness

Yes, the macroeconomic background looks tense. Prices for oil (CLK26) are high, and expensive aviation fuel lays down a burden on airlines. Expensive tickets can cool down the demand for passenger transportations.

The global aviation industry did rebound after the pandemic. But if we look at the aggregate revenue of the duopoly of Boeing and Airbus, then we see a paradox: it is significantly less than it was in 2018. Over the last several years, the world bought just half of the airplanes that it needs.

The aviation industry has created a “supply void” worth billions of dollars. Fleets of airlines are aging, they need replacements for more fuel-effective machines. And high oil prices can even spur the demand for new airplanes which economize on 15%-20% more fuel than machines of the past generation.

Airbus physically cannot close this gap. Its capacities on A320neo work on the limit, and the queue for airplanes stretches out to 2030 and further due to the shortage of engines in Europe. Boeing is the only one who can quench this production hunger.

Additionally, the market seems to ignore that there is still a real need for true, large airplanes. And no one is producing them. Airbus conclusively buried its giant A380, and the old passenger version of Boeing 777 faded into memory.

To replace its old fleet, Boeing rolled out the model 777X. This aircraft has a giant capacity of more than 400 passengers, and no one is competing with it. The problem is that due to the heightened caution of regulators, this airplane got stuck in the process of certification. And in the outcome, a whole production direction at Boeing today stands idle. And of course this idle standing reflects itself both in revenue and profit.

As soon as the FAA certifies the 777X, Boeing will be covered by an avalanche of orders. The postponed demand in this segment is colossal, because for airlines there is simply nowhere to buy similar machines. Yes, certification is a long process (possibly, still a year or two away). But this asset appears a hidden spring, which will cardinally change the revenue of the company.

Absolute Economic Moat

Many investors are afraid to buy shares of old industrial giants. We saw how electric vehicles (EV) destroyed the capitalization of traditional auto manufacturers.

But to apply this logic to Boeing is a fundamental mistake. There is no technological threat to commercial aviation. Neither right now, nor in 20 years, will there be a viable alternative to jet liners. People will not cease to fly, and airplanes will not begin to fly on batteries.

China actively is developing its COMAC C919. But without certificates of EASA and FAA, this airplane is locked inside Chinese borders. The global duopoly of Boeing and Airbus for now still is indestructible.

Risks and Perspectives

Does this mean that the path of Boeing will be smooth? No. The main risk for investors today consists in the dragging out of terms.

If regulators again find microscopic defects in new batches of airplanes or the process of certifying the 777X stretches out for several more years, Boeing will continue to burn cash. In such a scenario, the company will not go bankrupt – it is too important for the national security of the U.S. But avoiding bankruptcy could require a new large-scale additional capitalization, which would dilute current shareholders (this already occurred in 2024 when the company attracted $21 billion).

And nevertheless, the last data about deliveries shows that Boeing has broken through the regulatory “jam.” 737 MAX again massively descends from the conveyor. FAA limitations have been removed, and the company plans to soon launch a fourth assembly line.

The Path to $300 Billion

According to its own reports, Boeing believes it will generate positive free cash flow in 2026. If it returns to the levels of 2018, it is capable of generating $120-$130 billion in revenue and $12-$13 billion in net profit annually.

Given that the historical price-earnings ratio for shares in the U.S. is higher than those in Europe, where Airbus trades with a P/E of less than 30x, Boeing could reach a market cap of $300 billion when a normal production cycle resumes by 2030.

Therefore, I believe it is worth closely looking at Boeing shares here.

But of course, there is no reason to hurry with a purchase. However, on the next wave of growth, the shares of Boeing deserve the attention of investors.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Sysco Just Announced a $29.1 Billion Acquisition and Wall Street Is Nervous. Can a 3% Dividend Sweeten the Deal?

- Plug Power Just Scored a New Deal in Canada. Should You Buy Plug Stock Here?

- Why Bernstein Thinks You Should Buy the Dip in Sandisk Stock Here

- Should You Chase the Amazon-Driven Rally in Globalstar Stock Today?