Apple (AAPL) just crossed a milestone few tech companies ever see, hitting its 50th anniversary on April 1, 2026, five decades after Steve Jobs and Steve Wozniak turned a garage project into one of Wall Street’s most-watched stocks.

Over that span, a hypothetical 100-share allocation at Apple’s IPO price in 1980 would now be worth more than $5.5 million, showing the power of its long-term return story in the public markets.

Yet as the birthday candles are being lit, AAPL’s recent tape tells a more complicated story, with the stock down 6% year-to-date (YTD), leaving it behind both the S&P 500 Index ($SPX) and the broader technology sector over various time frames.

At the same time, Apple is no longer the undisputed market-cap king, having given up ground to Nvidia (NVDA) after its mid-single-digit pullback so far in 2026, even as investors debate whether its AI and services pivot can drive the next phase of growth.

With Apple turning 50 amid sector rotation, AI-fueled enthusiasm elsewhere in Big Tech, and clear signs of relative underperformance in its own chart, is AAPL at this anniversary moment a tired slice of overbaked mega-cap tech or a still-sweet piece of stock-market cake worth going back for? Let’s find out.

How Apple’s Numbers Stack Up

Apple may have turned 50, but its business model still leans on the same mix of hardware, software, and services that has defined it for decades. From the iPhone to its fast-growing Services segment, Apple still runs as an ecosystem company that monetizes devices and daily habits of more than a billion users worldwide.

Over the past 52 weeks, AAPL has gained 14.17%, which shows steady investor confidence, but it is down 5.75% over the past three months.

At a forward price-to-earnings multiple of 30.23 times, compared with the industry average of 21.41 times, Apple trades at a clear premium.

The numbers help explain why. With a market capitalization approaching $3.75 trillion and annual sales of $416.2 billion, Apple delivered first-quarter revenue of $143.8 billion, up 16% year-over-year (YOY), and earnings per share of $2.84, beating estimates and lifting net income to $42.1 billion.

Its payout ratio is 12.95%, which supports a quarterly dividend of $0.26 per share and extends a 14-year streak of consecutive increases. The yield sits at a modest 0.41%, but that dividend profile highlights how Apple balances returning cash to shareholders with keeping plenty of room to keep investing in its business.

What’s Still Powering Apple’s Growth Engine

Far from cooling, Apple is expanding its U.S. manufacturing footprint, with a major buildout of its Houston operations where Mac mini production is set to begin later this year. The same site will also handle advanced AI server manufacturing and run an Advanced Manufacturing Center to train future workers, a push expected to create thousands of jobs and double the size of the campus.

At the same time, Apple has signed a multi-year partnership with Alphabet (GOOG) (GOOGL) to incorporate Google’s Gemini models into Siri and other products. The deal will provide large-scale AI infrastructure and cloud power, marking an important step in Apple’s careful entry into the AI space. Gemini is set to support new AI-driven features across Apple’s ecosystem, with rollout expected later this year.

On top of that, Apple has launched Apple Creator Studio, a subscription bundle that pulls together professional creative tools like Final Cut Pro, Logic Pro, Pixelmator Pro, and others. Built with new intelligent features and a strong focus on privacy, the suite is meant to serve creators across many fields while keeping them inside Apple’s hardware and software ecosystem, adding another stream of recurring services revenue.

Wall Street’s Taste Test

Consensus estimates put Apple’s current-quarter (March 2026) earnings at $1.88 per share, up 13.94% from $1.65 a year ago. For the June quarter, earnings are expected at $1.70, up 8.28% YOY, while full-year fiscal 2026 projections sit at $8.40 per share, a 12.6% increase from the prior year, which points to steady growth even for a company of Apple’s size.

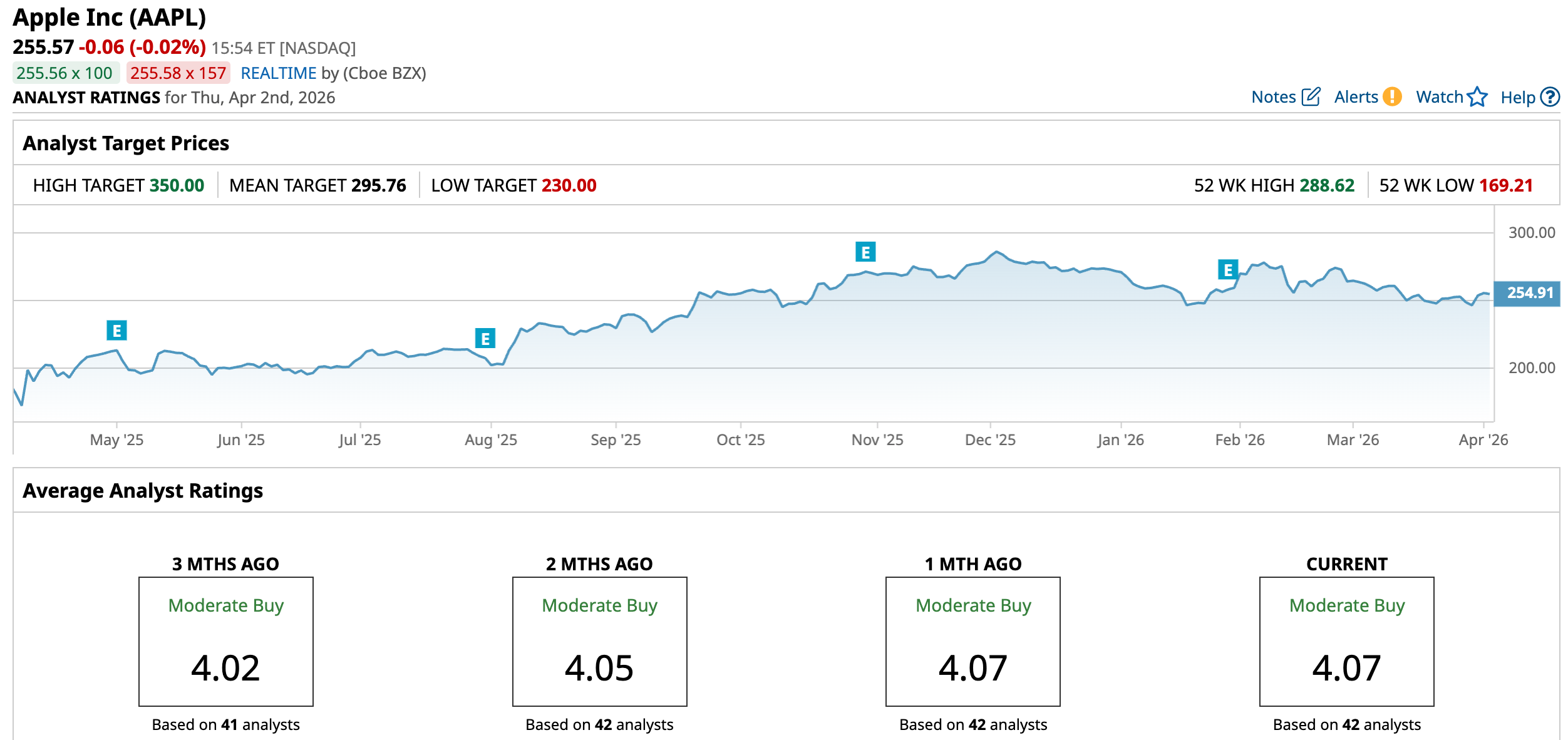

Wedbush’s Dan Ives, one of Wall Street’s most vocal Apple bulls, is sticking with that view. His team keeps an “outperform” rating and a $350 price target in place, telling investors to “ignore the panic and keep buying.” Ives thinks concerns about Apple being late to the AI race are overdone and is betting that upcoming Siri upgrades, built around new AI features and key partnerships, can bring fresh interest back to the stock and kick off another product cycle.

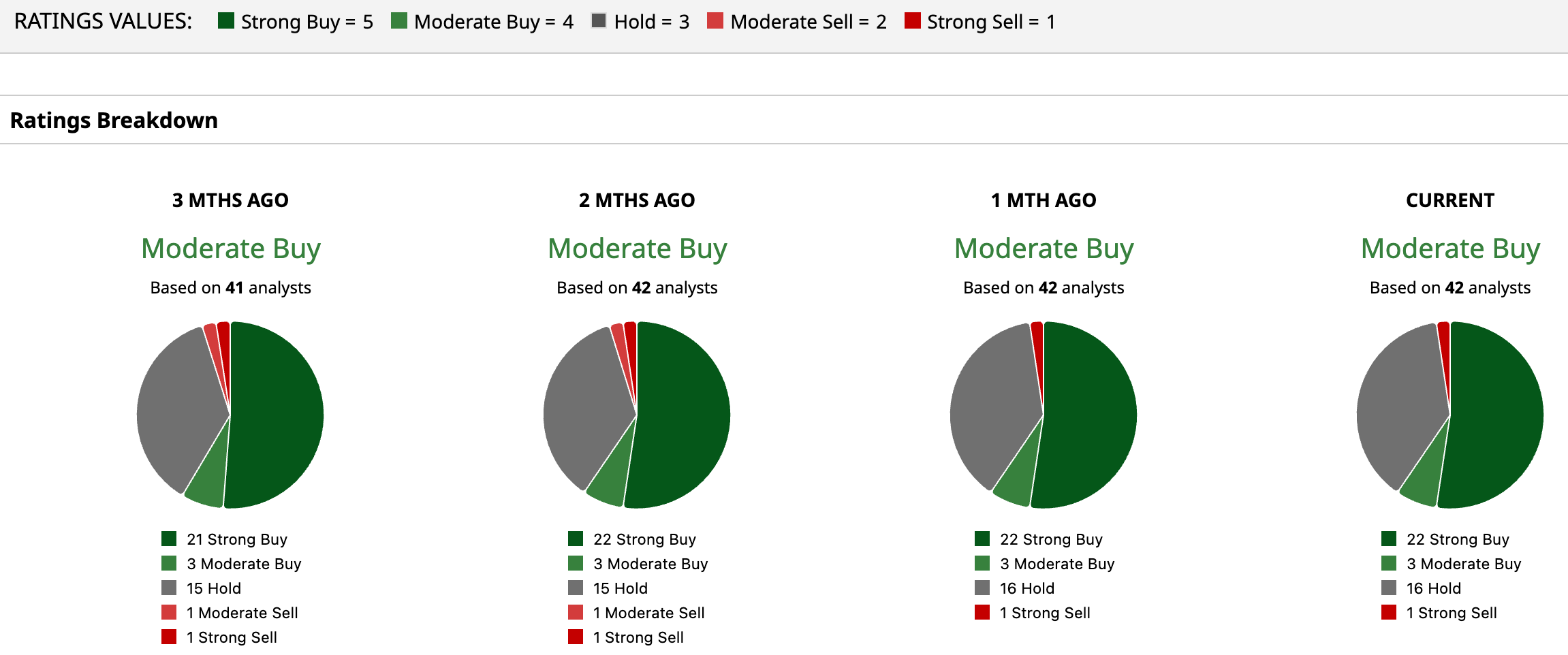

Across Wall Street, the tone is still broadly positive. All 42 analysts tracked sit at a “moderate buy” consensus, with an average price target of $295.76, which works out to roughly 15.7% upside from the current share price.

Conclusion

At 50, Apple’s stock still looks sweeter than stale. The company isn’t acting like a business that’s out of ideas, and the numbers backing its next chapter are more growth-like than sunset-stage. With earnings expected to rise solidly this year and next, a clear AI roadmap finally taking shape, and Wall Street still leaning “moderate buy” with meaningful upside to current targets, the risk-reward skews in favor of patient bulls. From here, AAPL shares look more likely to grind higher than roll over, even if the ride is choppier than in Apple’s earlier, hyper-growth decades.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Sysco Just Announced a $29.1 Billion Acquisition and Wall Street Is Nervous. Can a 3% Dividend Sweeten the Deal?

- Apple Just Turned 50 Years Old. Is the AAPL Stock Cake Stale or Sweet?

- Dear Delta Air Lines Stock Fans, Mark Your Calendars for April 8

- The Iran War Thrust Aluminum Prices Into the Spotlight, but Is There a Long-Term Bull Case for Rio Tinto Stock?