Expedia (EXPE) is an American online travel conglomerate. Over time, the company has evolved into a massive ecosystem of travel brands, including names like Expedia.com, Vrbo, and Hotels.com. Expedia Group operates through four main segments: Core OTA (Online Travel Agency), Trivago, Vrbo, and its quickly expanding B2B segment that helps provide travel infrastructure to airlines and banks.

Founded in 1996 as a division of Microsoft (MSFT), the company became independent in 1999 and is now headquartered in Seattle, Washington.

Expedia’s Slow Start to 2026

Expedia’s stock enjoyed a fruitful 2025, gaining 52%, but has faced some pressure in the first quarter of 2026, trading 20% below year-to-date (YTD) and 13% since its quarterly results. This pullback reflects investors' cautiousness regarding the company’s outlook. However, despite the dip, Expedia has performed strongly over the years, providing a 36% return in 52 weeks, 71% in two years, and 152% in the last three years.

In comparison to the S&P 500 Consumer Discretionary Index ($SRCD), Expedia has underperformed in early 2026. The benchmark index has declined roughly 9% YTD against Expedia’s 20% in the same time. This suggests investors be cautious of travel-based stocks, citing global travel challenges.

Strong Results on Weak Outlook

Expedia reported stellar fourth-quarter results in February 2026, with revenue touching $3.55 billion, delivering an 11.4% increase year-over-year (YoY). On the other hand, adjusted EPS came to $3.78, jumping 58% YoY and easily surpassing analyst estimates of $3.36 per share.

The report was headlined by its B2B segment, which saw bookings surge by 24% to $8.7 billion, marking its 18th consecutive double-digit quarterly growth. This helped adjusted EBITDA reach $848 million, a 32% spike from the same quarter last year, while margins expanded to 23.9%.

However, despite the strong financial beat, management provided a cautious 2026 outlook, expecting revenue growth at 6-9% with margin expansion capped at 100-125 basis points. This deceleration comes as the company shifts towards reinvesting in AI, machine learning, and B2B expansion. Nevertheless, the company instilled confidence in its cash flow generation by raising dividends by 20% to $0.48 per share, and with $3.1 billion in annual cash flow and a $240 billion travel backlog, it enters its second quarter on high margins.

Expedia Upgraded by Analyst

Jefferies has upgraded Expedia to a “Buy” rating with a raised price target of $300, reflecting an upside potential of 30% from current levels, citing the company as a prime beneficiary of the AI revolution. Analyst John Colantuoni believes the recent selloff opens a strategic entry point for EXPE stock, with “Answer Engine Optimization” becoming a key growth driver. The analyst pointed towards OpenAI’s strategic shift towards advertising and referral traffic instead of opting for a direct consumer-facing commerce, which allows Expedia to capture high-quality leads from AI platforms.

This upgrade demonstrates how large language models (LLMs) serve as a powerful performance channel, enabling seasoned players like Expedia to enhance their market share. By integrating AI with its customer service, like the “Romie” assistant, the analyst expects Expedia to reduce customer acquisition costs significantly while improving product velocity.

Should You Buy EXPE Stock?

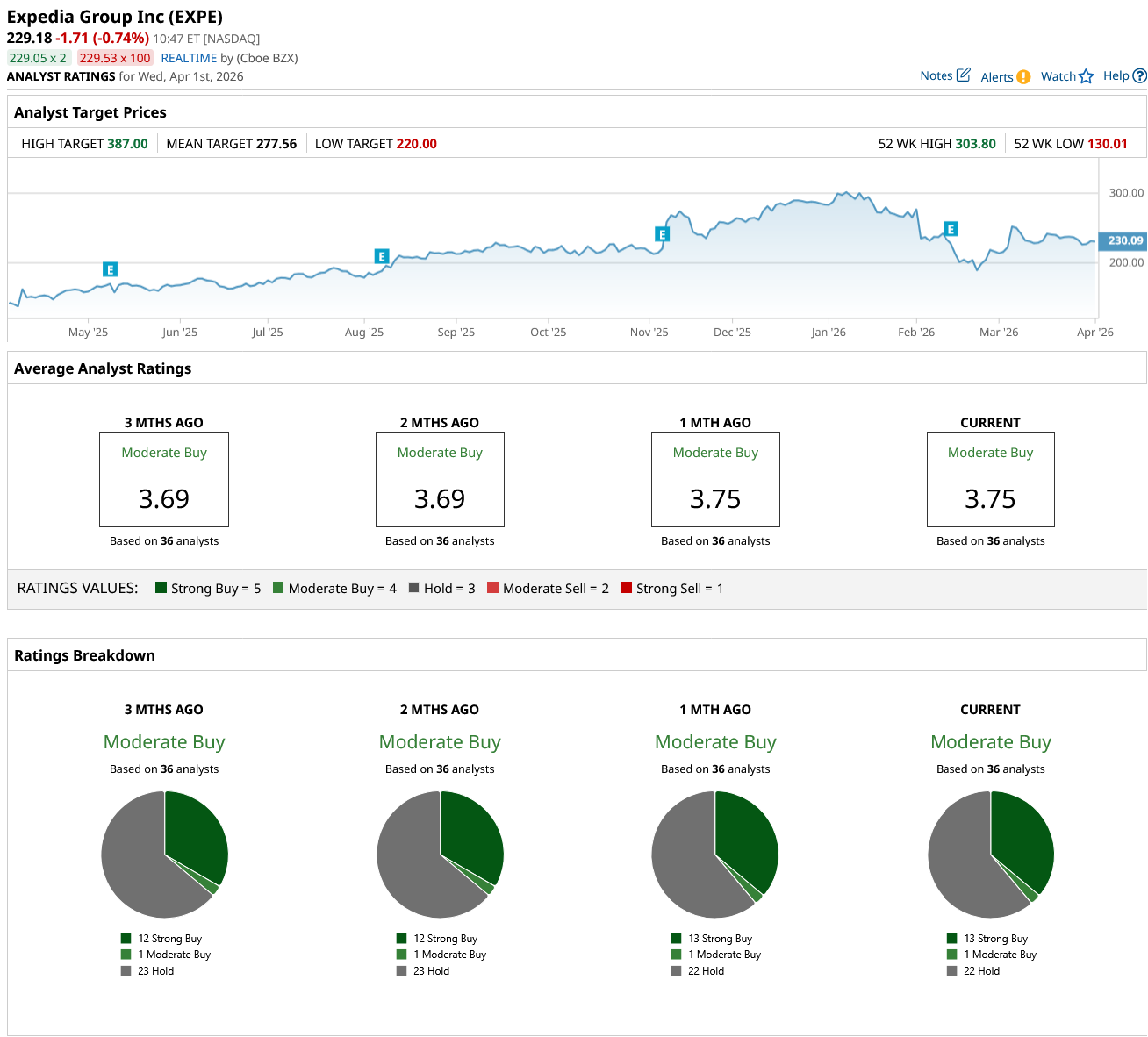

With Jefferies’ recent upgrade on EXPE stock, Expedia is increasingly being viewed as a top value play in the tech travel sector. The stock currently has a “Moderate Buy” consensus rating among Wall Street analysts, with 13 “Strong Buy” ratings, one "Moderate Buy" and 22 “Hold” ratings among 36 ratings.

While the mean price target sits at $277.56, reflecting 21% upside, its street high of $387 signals a possible 69% upside from current levels. As the company continues its aggressive share buyback and high-margin B2B expansion, investors are presented with a rare opportunity on this tech-enabled travel platform.

On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- A Giant Meatpacking Strike Isn’t Enough to Dent the Bull Case for JBS Stock, According to Bank of America

- TotalEnergies Is ‘Dominating’ Amidst Iran War Oil Disruptions. Should You Buy TTE Stock Now?

- Gold’s 200-Day Bounce: Reversal Signal or Market Trap?

- Want to Invest Like Jensen Huang? Here Are the Top 3 Stocks to Buy for April 2026.