The markets are back, baby. The Dow Jones was the worst-performing index yesterday, up 2.49%, on news that the war in Iran would soon be over—woot woot.

Seriously, though, President Trump will speak live to the nation at 9 p.m. ET about his plans to end the war. That could mean more gains today and tomorrow. The S&P 500 is up nicely in Wednesday morning trading, while the VIX is down.

Honestly, I’ve given up trying to figure out the direction of stocks in 2026. I think most investors are in the same boat. We’re just along for the ride.

Yesterday, 128 NYSE stocks hit 52-week lows, while 57 hit new highs. Over on the Nasdaq, 187 hit new 52-week lows, while 69 hit new highs.

I want to focus specifically on the 128 NYSE stocks that have hit new 52-week lows. Of those, five have share prices of $100 or higher. Three of them are possible buy-on-the-dip candidates.

I rate them from the worst to the best opportunity.

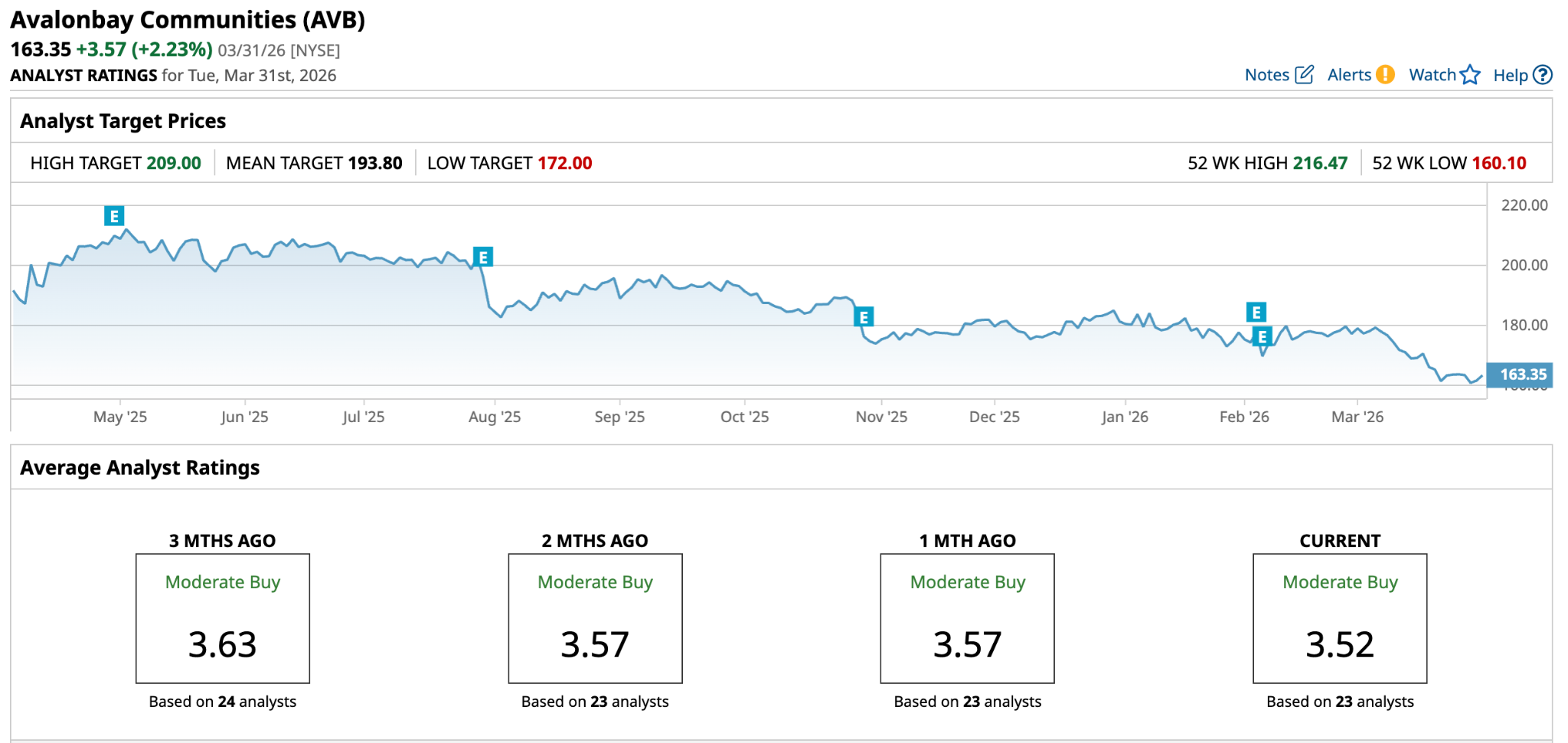

AvalonBay Communities (AVB)

AvalonBay Communities (AVB) hit a new 52-week low of $160.10 on Tuesday. It is the 12th new 52-week low in the past 12 months. In that time, its shares have lost 24% of their value. They’re down nearly 13% over the past five years.

AvalonBay is a real estate investment trust (REIT) that owns multi-family buildings with nearly 100,000 apartments in 10 regions of the country. Since its IPO in November 1993, it’s delivered a 10.8% total shareholder return. That’s nothing to sneeze at.

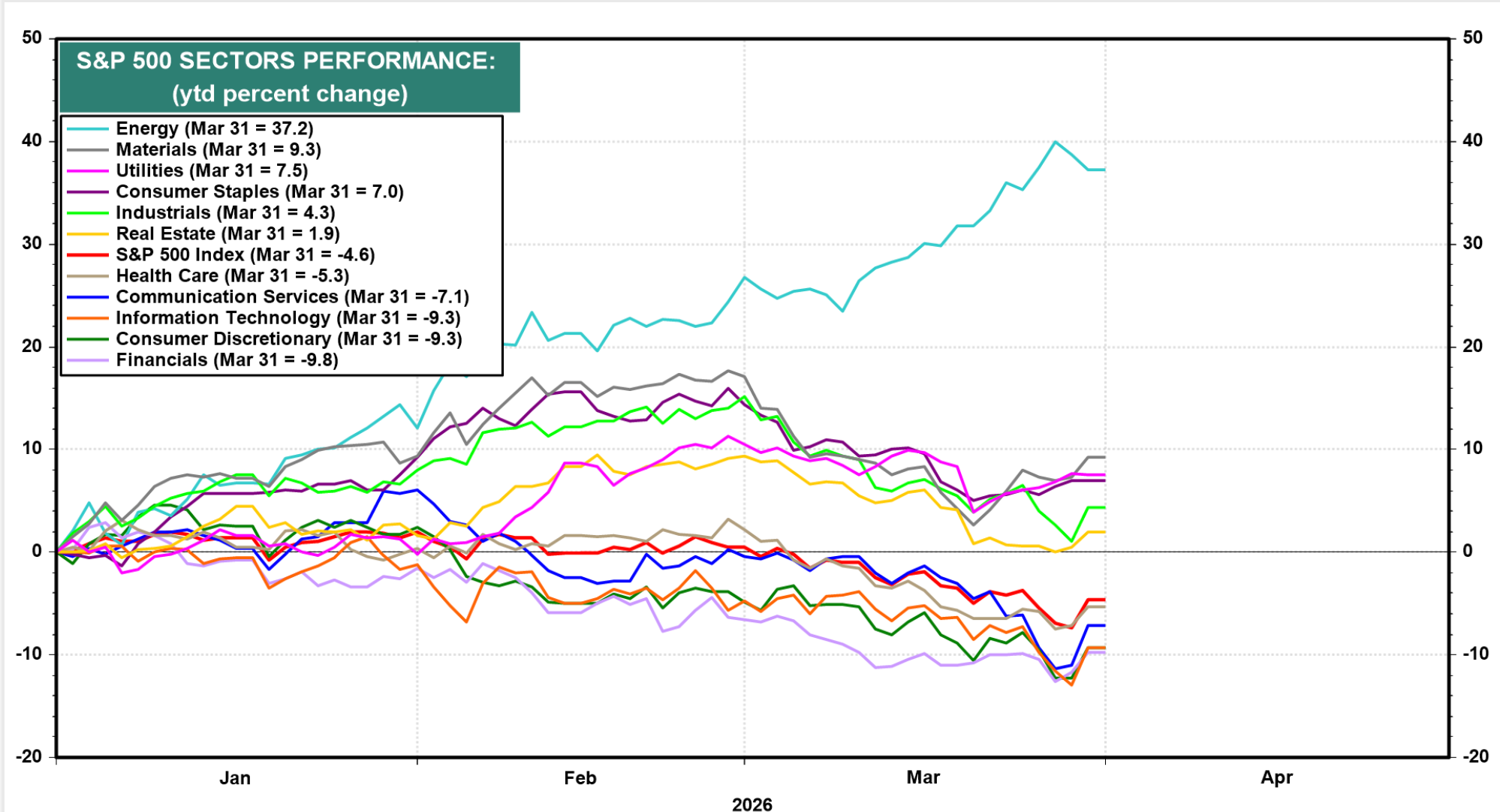

AVB is one of 31 companies in the S&P 500 real estate sector. Since October 2022, the sector has had the second-lowest cumulative return at 22% through March 31.

The good news is that its stock is bound to move higher at some point. As recently as Nov. 27, 2024, it traded at a penny under $240. Is now the time?

Analysts aren’t sold. Of the 23 covering it, only 6 rate it a Buy (3.52 out of 5), with a target price of $193.80, which is 19% above its current share price.

The thing to wonder about is higher interest rates. If $100 oil holds for the next year and inflation rises significantly, that will put downward pressure on its property valuations, at which point its stock becomes dead money.

I rate it C, primarily because I don’t see multi-family residential real estate staying down for too long, given the housing shortage.

Abbott Laboratories (ABT)

Abbott Laboratories (ABT) hit a new 52-week low of $100.88 on Tuesday. It is the 11th new 52-week low in the past 12 months. In that time, its shares have lost 22% of their value. They’re down nearly 14% over the past five years.

Since October 2022, according to Yardeni Research, the S&P 500 healthcare sector has delivered the worst performance of the 11, up 20.3% through March 31. That explains some of Abbott’s lagging performance.

But clearly there’s more to the story. Yesterday, Barchart contributor Rich Duprey wondered when ABT stock would bounce back.

He pointed out several things to like about the drug stock: 54 consecutive years of dividend growth, strong free cash flow, healthy 10% earnings growth in 2026, and an acquisition (Exact Sciences) that gives it a strong position in cancer detection and screening.

Abbott’s been around forever. It’s got a healthy dividend. Income-focused investors should consider it.

However, based on an enterprise value (EV) of $184.65 billion and annual free cash flow of $7.4 billion, its free cash flow yield is 4.0%; I consider anything below 4% to be overvalued. It’s on the cusp.

If it were me, I’d wait for it to fall into the $90s before buying on the dip. That said, it last traded in the $90s in November 2023, so ABT might not get there.

I rate it B. Consistent dividend-paying stocks remain an important component of any core investment portfolio. A 10-year total return of 10% is not unreasonable from Abbott.

Progressive (PGR)

Progressive (PGR) hit a new 52-week low of $196.38 on Tuesday. It is the 22nd new 52-week low in the past 12 months. In that time, its shares have lost 30% of their value. However, they’re up nearly 108% over the past five years.

S&P 500 financials, on the whole, have performed the worst of any sector in 2026, down 9.8% year to date through March 31. Property & casualty insurers have done a little better -- Progressive is a leader in the industry -- down 3.9% YTD.

Source: LSEG Datastream and Yardeni Research, Standard & Poor’s

Progressive’s CEO, Tricia Griffith, is one of the best in P&C, or any industry for that matter. The P&C market has enjoyed significant profit growth in recent years. That could be coming to a close. The industry has become more competitive, and repairs are more costly, putting downward pressure on these profits. That’s a big reason PGR has stalled.

However, 2025 was a record year for the company. It generated $17.55 billion in cash from its operations, up from $15.12 billion in 2024 and $2.29 billion in 2015, a 10-year compound annual growth rate of 22.6%.

Known for data-driven underwriting, it strives to keep the combined ratio below 96.

The combined ratio is a combination of the loss ratio, which indicates how much it pays out for claims as a percentage of premiums earned, and the expense ratio, which indicates the cost of acquiring business as a percentage of premiums.

In 2025, it was 87.4 (lower is better); in 2024, it was 88.8; and in 2023, it was 94.9. The combined ratio was last this low in 2006. Yet it trades at 12.0 times the 2026 EPS estimate of $16.21, according to S&P Global Market Intelligence.

I rate it an A. It’s well run, everyone needs P&C, and historically, forward P/E hasn’t been this low since June 2021, and September 2011 before that.

On the date of publication, Will Ashworth did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.