Artificial intelligence has moved from a promising idea to a massive buildout of real-world infrastructure, and the spending numbers are huge. Projections put the AI data center chip market at about 207 billion dollars in GPU and accelerator shipments in 2025, with total demand expected to reach 286 billion dollars by 2030 as AI infrastructure spending likely peaks around 2026.

That kind of money is flowing through every part of the ecosystem, from power and cooling specialists like Vertiv (VRT), which is working through a roughly 15 billion dollar backlog tied to AI data centers, to high-speed networking and analog chip suppliers racing to keep up with the power and bandwidth needs of new AI clusters.

It also helps explain why a well-known billionaire who built his reputation as one of Tesla’s (TSLA) largest individual shareholders has shifted more focus to Nvidia, the company many analysts now refer to as the “Godfather of AI.” He recently revealed the purchase of 1 million Nvidia (NVDA) shares, describing it as both a bet on AI’s long runway and a move to steady what he views as a nervous market that is starting to question how far this AI spending cycle can go.

If institutional forecasts still point to AI chip spending climbing into the hundreds of billions over the next few years, and billionaire “AI insiders” are adding to Nvidia at this point in the cycle, should everyday investors be thinking about doing the same or wondering whether this is undoubtedly when caution matters most? Let’s find out.

Inside Nvidia’s Numbers

Nvidia (NVDA) makes most of its money from graphics processing units (GPUs) that power data centers, gaming, and AI infrastructure, which sit at the core of its business.

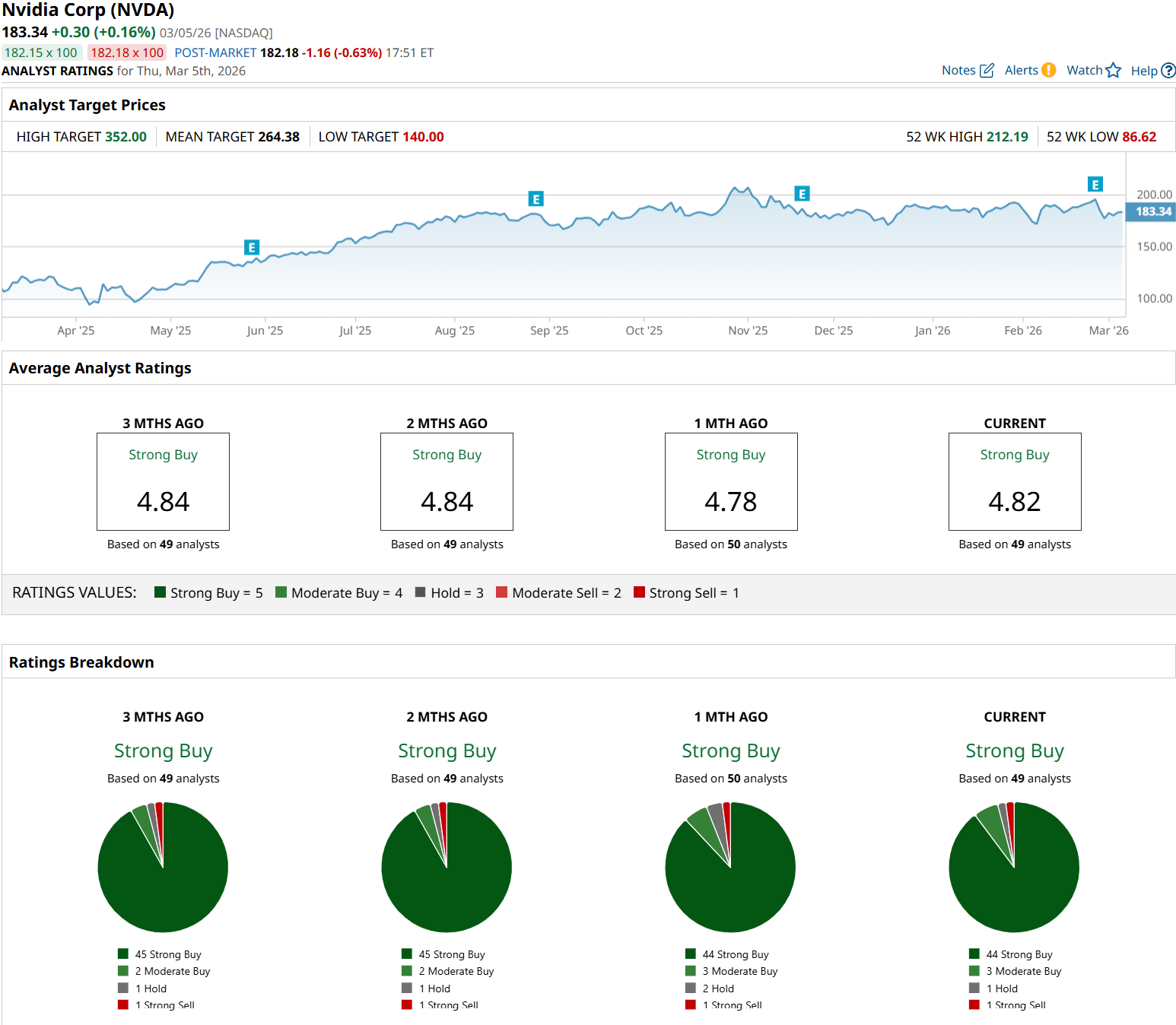

Over the past year, the stock has been difficult to ignore, climbing 56.28% over the last 52 weeks, even though it is down 1.71% year-to-date (YTD) after a very strong 2025.

Even with that recent pullback, Nvidia still trades at a premium. Its forward price-to-earnings ratio is 24.31x, slightly above the sector average of 21.83x, which shows investors are still pricing in faster growth. The trailing P/E is 39.40, backed by earnings per share of 4.57. The dividend story is modest but disciplined: a 0.04% yield (0.02% annualized), two straight years of dividend increases, a low forward payout ratio of 0.87%, and a most recent quarterly dividend of $0.010 paid on Dec. 4, 2025.

On the financial side, Nvidia keeps setting records. For Q4 FY2026, it reported revenue of $68.1 billion, up 20% from the previous quarter and 73% year over year (YoY), bringing full-year fiscal 2026 revenue to $215.9 billion. Annual net income reached $120.1 billion, supported by gross margins of 71% and GAAP EPS of $4.9. Over the same fiscal year, Nvidia returned $41.1 billion to shareholders through buybacks and dividends and still has $58.5 billion left under its repurchase authorization, showing clear confidence in its long-term story.

The Engines Behind the Surge

Nvidia signed a multiyear deal with Coherent (COHR) to push next-generation optics technologies that are essential for scaling AI data centers. The agreement includes a multibillion-dollar purchase commitment from Nvidia and a $2 billion investment to grow Coherent’s U.S. manufacturing capacity and R&D. The work centers on optical interconnects and advanced package integration, which are needed for high‑bandwidth, energy‑efficient AI connectivity.

Nvidia followed that with multi-year agreements with Lumentum Holdings (LITE) to keep pushing forward in optics. This partnership closely resembles the Coherent deal, with another $2 billion investment aimed at building a new U.S. fab and locking in capacity for key laser components used in AI systems. By leaning into optical integration, Nvidia is reinforcing the base of large AI factories and improving energy efficiency across its data infrastructure.

On top of these chip and optics investments, Nvidia has teamed up with major global telecom players, including Ericsson, Nokia, Cisco, BT Group, SoftBank, and T‑Mobile, to lead the development of 6G networks built on AI‑native, open, and secure platforms. This effort places Nvidia at the center of the next generation of connectivity and intelligent infrastructure.

How Analysts See Nvidia’s Next Chapter

Nvidia’s outlook for the first quarter of fiscal 2027 calls for revenue of around $78 billion, plus or minus 2%, and that guidance does not include any data center compute revenue from China because of current export limits.

Analysts expect earnings of $1.67 per share for the current quarter (April 2026) and $1.80 for the next quarter (July 2026). On a full-year view, earnings are projected at $7.52 for fiscal 2027, which works out to strong YoY growth rates of 116.88%, 81.82%, and 64.55% across the near-term periods already in focus.

Major research firms are lining up behind that story. Wedbush’s Dan Ives describes 2026 as an “inflection point” for the global AI buildout and sees Nvidia as the top AI chip supplier and main winner from rising enterprise and hyperscaler spending. His $275 price target suggests roughly 50% upside from where the stock traded when he published that view. Rosenblatt Securities is just as upbeat, lifting its target from $245 to $300, which was the biggest percentage increase among the major firms covering the name.

Across the Street, 49 analysts currently rate NVDA as a consensus “Strong Buy,” with an average price target of $264.38. That consensus target points to about 44.2% upside from its recent trading level.

Conclusion

For everyday investors, this looks less like a moment to “back up the truck” blindly and more like a situation where the odds still lean in Nvidia’s favor if you can live with volatility. The company is riding a massive AI build‑out, backing it with record financials, deep strategic partnerships, and an analyst community that still sees meaningful upside from here. Over the next few years, the most likely path is higher prices punctuated by sharp pullbacks as AI enthusiasm ebbs and flows, which means disciplined, staged buying probably makes more sense than an all‑in bet at once.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart