Energy technology company GE Vernova (GEV) is looking at a multi-billion-dollar opportunity, as President Trump and Japanese Prime Minister Takaichi are set to announce a $40 billion nuclear power project based in Tennessee. The project, a part of a $550 billion fund the U.S. and Japan have planned as part of a deal that included lower auto tariffs and other levies, is set to feature GE Vernova and Hitachi (HTHIY) in the construction of BWRX-300 small modular nuclear reactors.

Against this backdrop, should you consider buying GE Vernova’s stock?

About GE Vernova Stock

GE Vernova is a global energy technology company that builds and supports systems for generating, transmitting, and managing electricity worldwide. It runs three main operations: conventional and clean power generation, wind energy, and grid modernization solutions which provide equipment, software, and long-term services to utilities, industries, and governments. Headquartered in Cambridge, Massachusetts, the company has a market capitalization of $229.39 billion.

GE Vernova’s stock has risen over the past year because investors expect strong, long-term demand for power generation and grid modernization equipment, especially from data centers and AI-driven infrastructure.

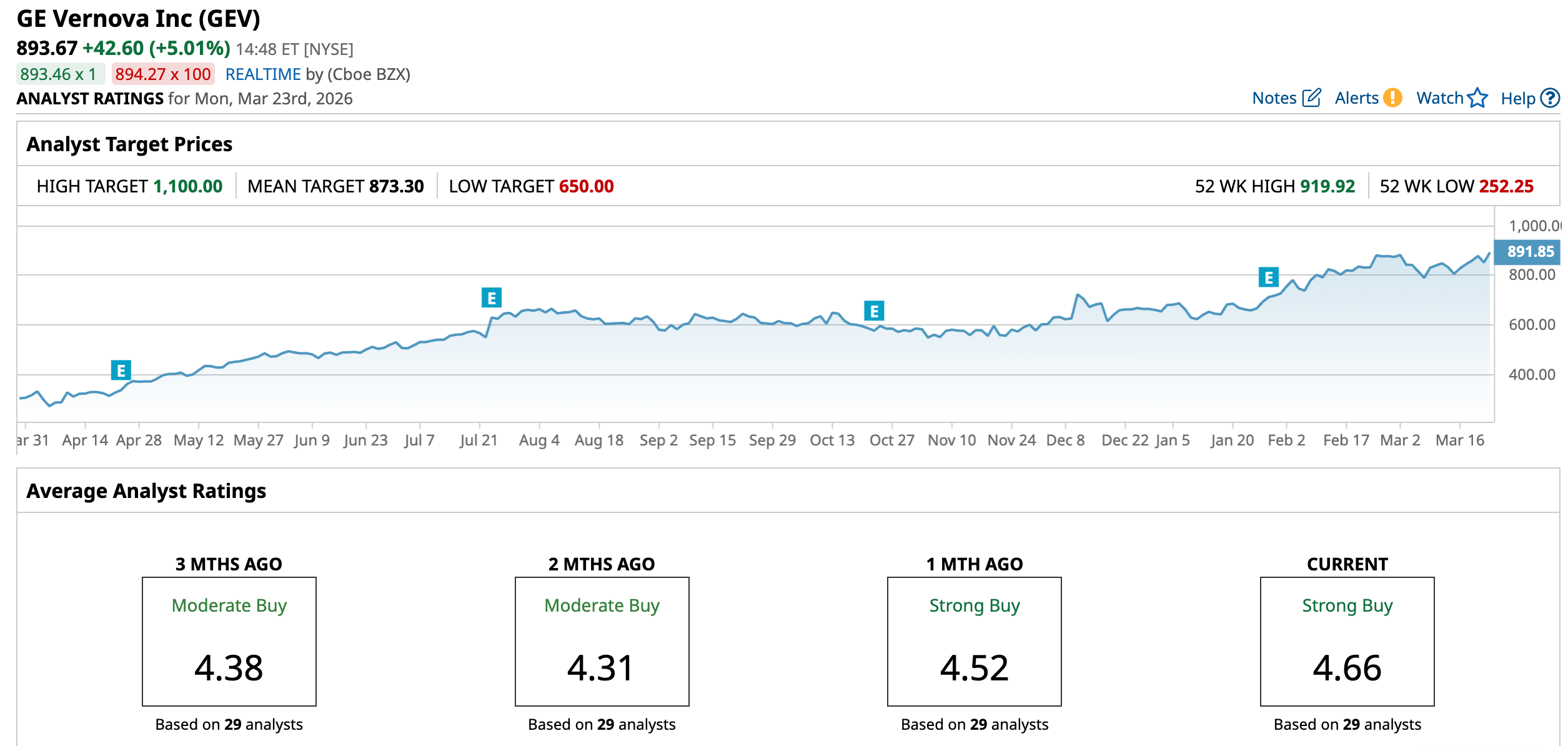

Over the past 52 weeks, the stock has gained 167.06%, while it has been up 36.42% year-to-date (YTD). Just for comparison, the S&P 500 index ($SPX) is up 16.57% over the past 52 weeks and is down 3.5% YTD. The company’s shares reached a 52-week high of $920.63 on March 23, but are down 2.65% from that level.

After this surge, the stock’s valuation has become stretched compared to its peers. Its forward-adjusted price-to-earnings ratio of 62.83 times is significantly higher than the industry average of 18.61x.

GE Vernova’s Q4 Results Robustly Surpassed Expectations

For the fourth quarter of fiscal 2025, GE Vernova reported 65% organic year-over-year (YOY) order growth to $22.20 billion, with expansion reported across all segments. The company’s total revenues increased 4% from the prior-year period to $10.96 billion, exceeding the $10.08 billion that Wall Street analysts had expected. Its organic revenues grew by 2% YOY.

The Power segment recorded a 78% YOY growth in its orders, driven by Gas Power equipment tripling YOY due to higher volume and pricing. In the Wind segment, a 55% order growth was driven by improved Onshore Wind equipment, primarily outside North America, while in the Electrification segment, a 55% order growth was driven by strong demand for grid equipment.

GE Vernova’s EPS climbed considerably YOY from $1.73 to $13.39, also heftily surpassing the $3.05 figure that Wall Street analysts had expected. Moreover, its free cash flow increased from $572 million to $1.81 billion over the same period. The company really did end the year on a high, with backlogs increasing by $15 billion sequentially from equipment and services at the Power and Electrification segments.

Based on these solid results, GE Vernova raised its 2026 revenue outlook from a range of $41 billion-$42 billion to $44 billion-$45 billion, while its free cash flow outlook was raised from $4.5 billion-$5 billion to $5 billion-$5.50 billion. However, Wall Street analysts have a mixed view of the company’s future bottom line. For fiscal 2026, its EPS is expected to decline by 21% YOY to $13.97, followed by a 55.6% improvement to $21.73 in fiscal 2027.

What Analysts Think About GE Vernova Stock

This month, analysts at Rothschild Redburn double upgraded their rating on GE Vernova’s stock from “Sell” to “Buy,” while raising the price target from $560 to a Street-high of $1,100, citing stronger demand for power equipment and services as AI boosts data center expansion, increasing the need for gas turbines.

In January, RBC Capital maintained an “Outperform” rating on GE Vernova’s stock, while raising the price target from $761 to $800, following a “strong quarter ahead of expectations,” as the company shows positive prospects for the foreseeable future. RBC Capital analysts also noted the acquisition of electrical transformer and related equipment maker Prolec GE as a contributor to GE Vernova’s results, faster than modeled.

On the other hand, Baird analysts downgraded the stock from “Outperform” to “Neutral” and lowered its price target to $649 from $816, citing rising investor concerns about a possible oversupply of power generation capacity, sparked by recent announcements from competitors entering the power sector.

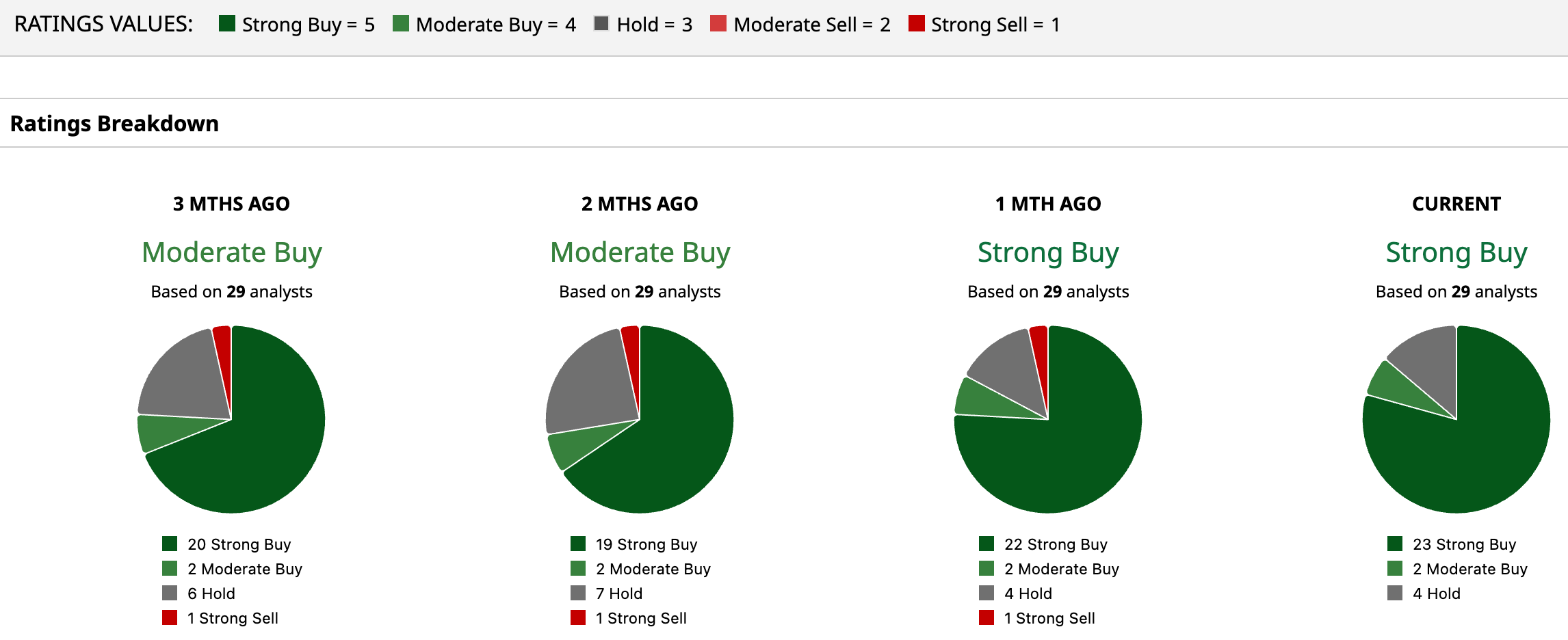

GE Vernova has grabbed Wall Street's limelight, with analysts awarding it a consensus “Strong Buy” rating. Of the 29 analysts rating the stock, a majority of 23 analysts have rated it a “Strong Buy,” two analysts suggest a “Moderate Buy,” while four analysts are playing it safe with a “Hold” rating. The consensus price target of $873.30 represents a slight downside from current levels. However, the Street-high Rothschild-given price target of $1,100 indicates a 23% upside.

Key Takeaways

With solid fundamental growth and a lucrative opportunity, alongside bullish analyst sentiments, GE Vernova’s stock might be a buy here.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.