With a market cap of $24.3 billion, Corpay, Inc. (CPAY) is a global payments company that helps businesses and consumers manage vehicle-related expenses, lodging, and corporate payments across the United States, Brazil, the United Kingdom, and other international markets. It offers a wide range of solutions, including fuel and fleet payments, AP automation, virtual and corporate cards, cross-border payments, and workforce lodging services.

The fuel card and payment products provider's shares have lagged behind the broader market over the past 52 weeks. CPAY stock has decreased 8.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied 11.7%. However, shares of the company are up 15.4% on a YTD basis, outpacing SPX’s marginal return.

Looking closer, shares of the Atlanta, Georgia-based company have underperformed the State Street Financial Select Sector SPDR ETF’s (XLF) 1.3% rise over the past 52 weeks.

Shares of Corpay climbed 11.6% following its Q4 2025 results on Feb. 4 after the company posted a strong earnings beat, with revenue rising 21% year-over-year to $1.25 billion, organic revenue growth of 11% for the third straight quarter, and adjusted EPS up 13% to $6.04, all exceeding expectations. The results highlighted robust underlying demand, led by 16% organic growth in the corporate payments segment despite a 200-basis-point headwind from lower interest rates.

For the fiscal year ending in December 2026, analysts expect Corpay’s EPS to grow 21.5% year-over-year to $24.56. The company’s earnings surprise history is promising. It beat the consensus estimates in the last four quarters.

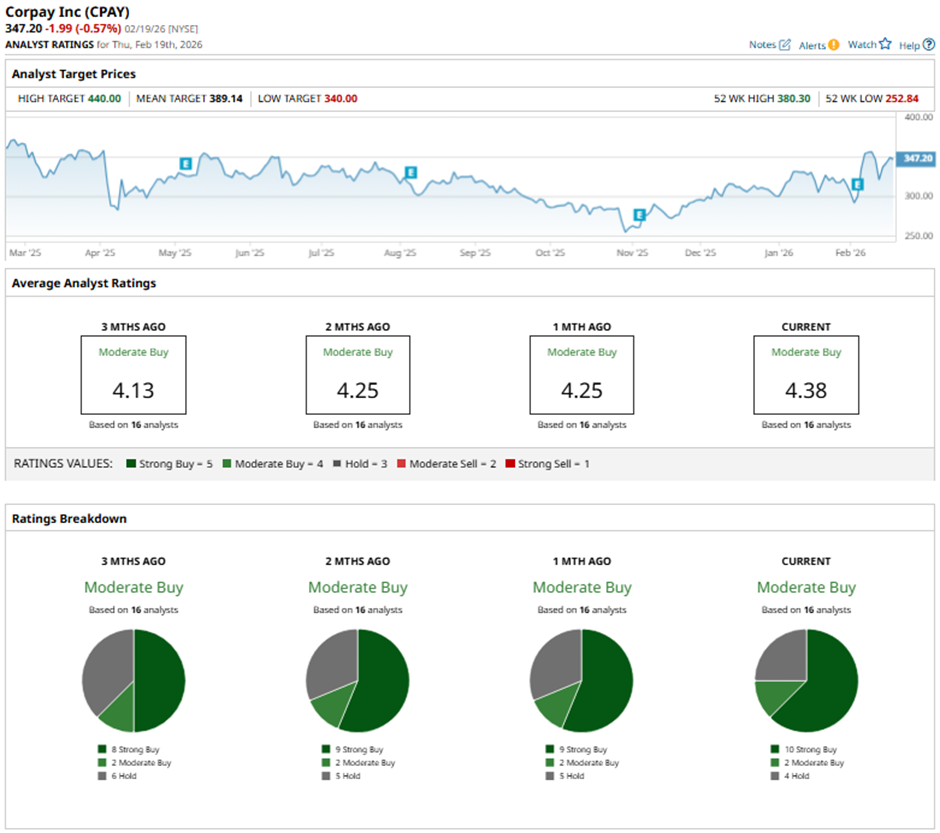

Among the 16 analysts covering the stock, the consensus rating is a “Moderate Buy.” That’s based on 10 “Strong Buy” ratings, two “Moderate Buys,” and four “Holds.”

On Feb. 5, RBC Capital raised its price target on Corpay to $363 and maintained a “Sector Perform" rating.

The mean price target of $389.14 represents a 12.1% premium to CPAY’s current price levels. The Street-high price target of $440 suggests a 26.7% potential upside.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Dear IonQ Stock Fans, Mark Your Calendars for February 25

- As Tesla Launches FSD Subscriptions, Should You Buy, Sell, or Hold TSLA Stock?

- Why Michael Saylor Isn’t Worried About MicroStrategy Stock Unless Bitcoin Drops Below $8,000

- This High-Yield Dividend King Has 56 Years of Raises and Wall Street Is Screaming ‘Buy’