Highlands Ranch, Colorado-based UDR, Inc. (UDR) is a leading multifamily REIT with a demonstrated performance history of delivering superior and dependable returns by successfully managing, buying, selling, developing and redeveloping attractive real estate communities in targeted U.S. markets. Valued at $11.4 billion by market cap, the company owns, operates, and develops apartment communities.

Shares of this leading multifamily REIT have underperformed the broader market considerably over the past year. UDR has declined 22% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 13.4%. In 2025, UDR’s stock fell 22.2%, compared to the SPX’s 14.3% rise on a YTD basis.

Narrowing the focus, UDR has also lagged behind the Residential REIT ETF (HAUS). The exchange-traded fund has declined about 11.4% over the past year. Moreover, the ETF’s 9.3% losses on a YTD basis outshine the stock’s double-digit dip over the same time frame.

On Oct. 29, UDR shares closed down more than 4% after reporting its Q3 results. Its FFO per share of $0.65 surpassed Wall Street expectations of $0.63. The company’s revenue totaled $431.9 million, representing a 2.8% year-over-year increase. The company expects full-year FFO in the range of $2.53 to $2.55 per share.

For the current fiscal year, ending in December, analysts expect UDR’s FFO per share to grow 2.4% to $2.54 on a diluted basis. The company’s earnings surprise history is impressive. It beat or matched the consensus estimate in each of the last four quarters.

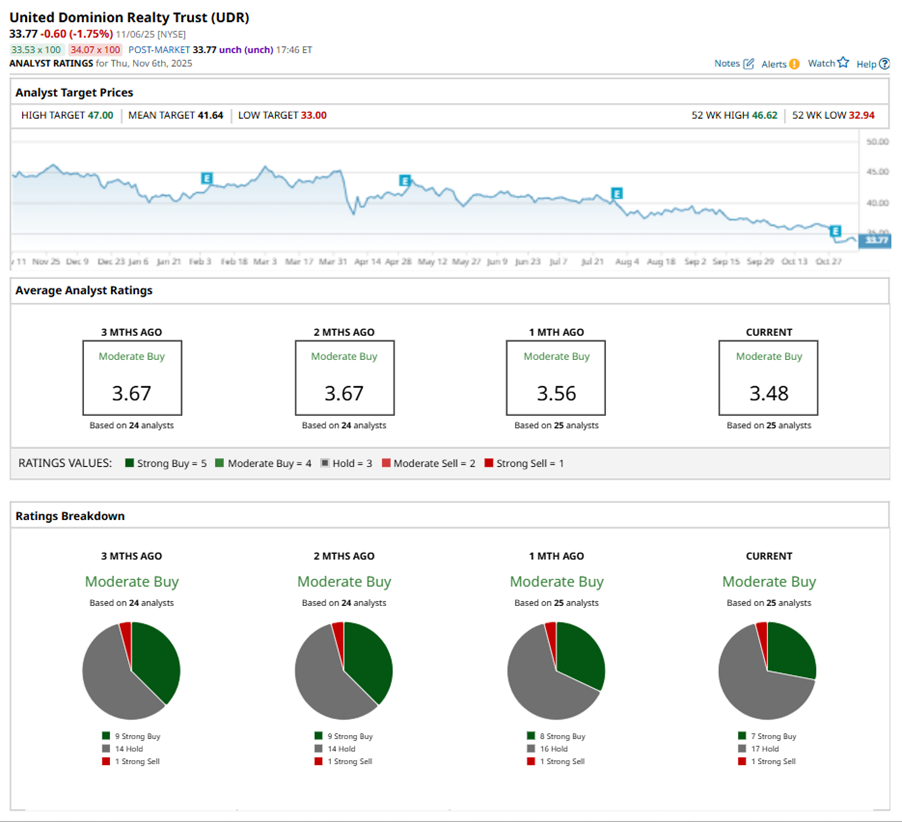

Among the 25 analysts covering UDR stock, the consensus is a “Moderate Buy.” That’s based on seven “Strong Buy” ratings, 17 “Holds,” and one “Strong Sell.”

This configuration is less bullish than a month ago, with eight analysts suggesting a “Strong Buy.”

On Nov. 4, Brad Heffern from RBC Capital maintained a “Hold” rating on UDR with a price target of $38, implying a potential upside of 12.5% from current levels.

The mean price target of $41.64 represents a 23.3% premium to UDR’s current price levels. The Street-high price target of $47 suggests an ambitious upside potential of 39.2%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Nvidia Stock 2026 Prediction: Can NVDA’s Gravity-Defying Rally Continue?

- These 3 Tech Stocks Have Been Red-Hot in 2025 but Their Charts Are Screaming ‘Danger’

- Stock Index Futures Slip as Valuation and Economic Concerns Persist, U.S. Confidence Data on Tap

- Verizon Is Getting an Amazon Data Center Boost. Should You Buy the High-Yield Dividend Stock Here?