Over the last six months, Bath and Body Works’s shares have sunk to $20.79, producing a disappointing 8.7% loss - a stark contrast to the S&P 500’s 9% gain. This might have investors contemplating their next move.

Is now the time to buy Bath and Body Works, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Is Bath and Body Works Not Exciting?

Despite the more favorable entry price, we’re sitting this one out for now. Here are three reasons you should be careful with BBWI, plus one stock we’d rather own.

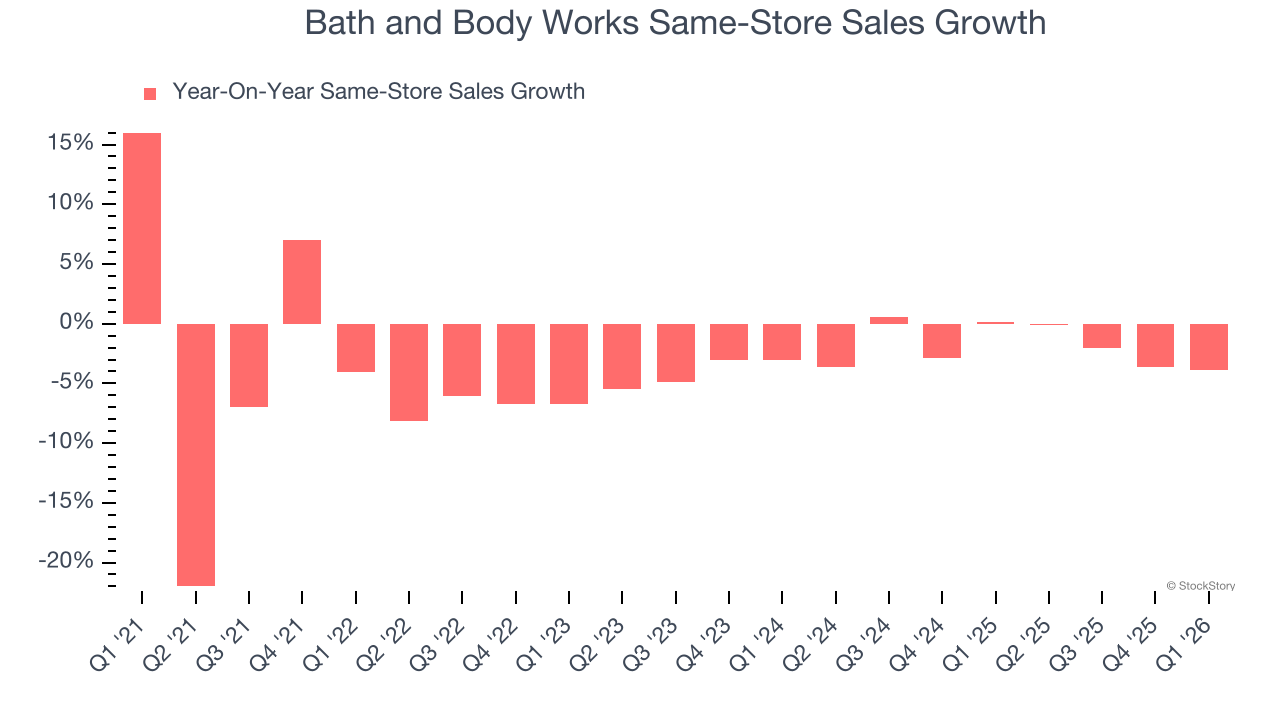

1. Shrinking Same-Store Sales Indicate Waning Demand

Same-store sales show the change in sales for a retailer’s e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Bath and Body Works’s demand has been shrinking over the last two years as its same-store sales have averaged 1.9% annual declines.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Bath and Body Works’s revenue to drop by 1.7%, close to This projection is underwhelming and indicates its newer products will not accelerate its top-line performance yet.

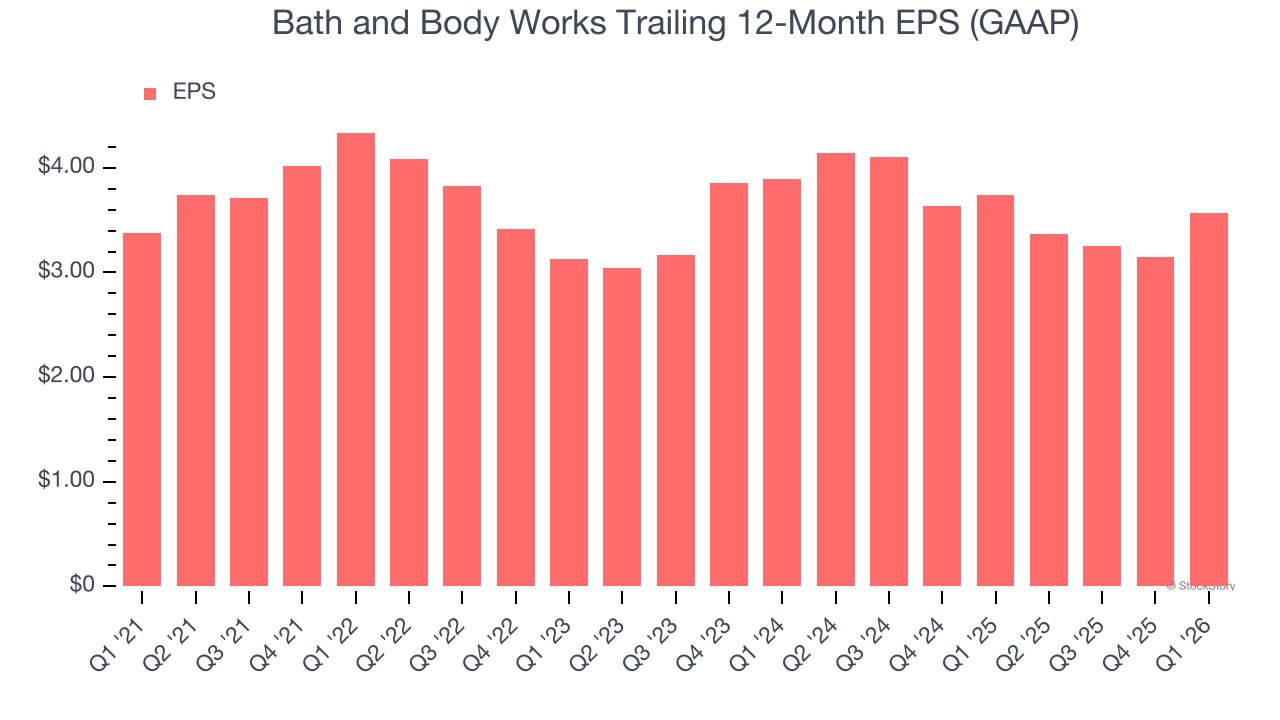

3. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Bath and Body Works’s EPS grew at 4.5% compounded annual growth rate over the last three years. On the bright side, this performance was better than its 1.2% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Final Judgment

Bath and Body Works isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 8.1× forward P/E (or $20.79 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We’re pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI is taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.