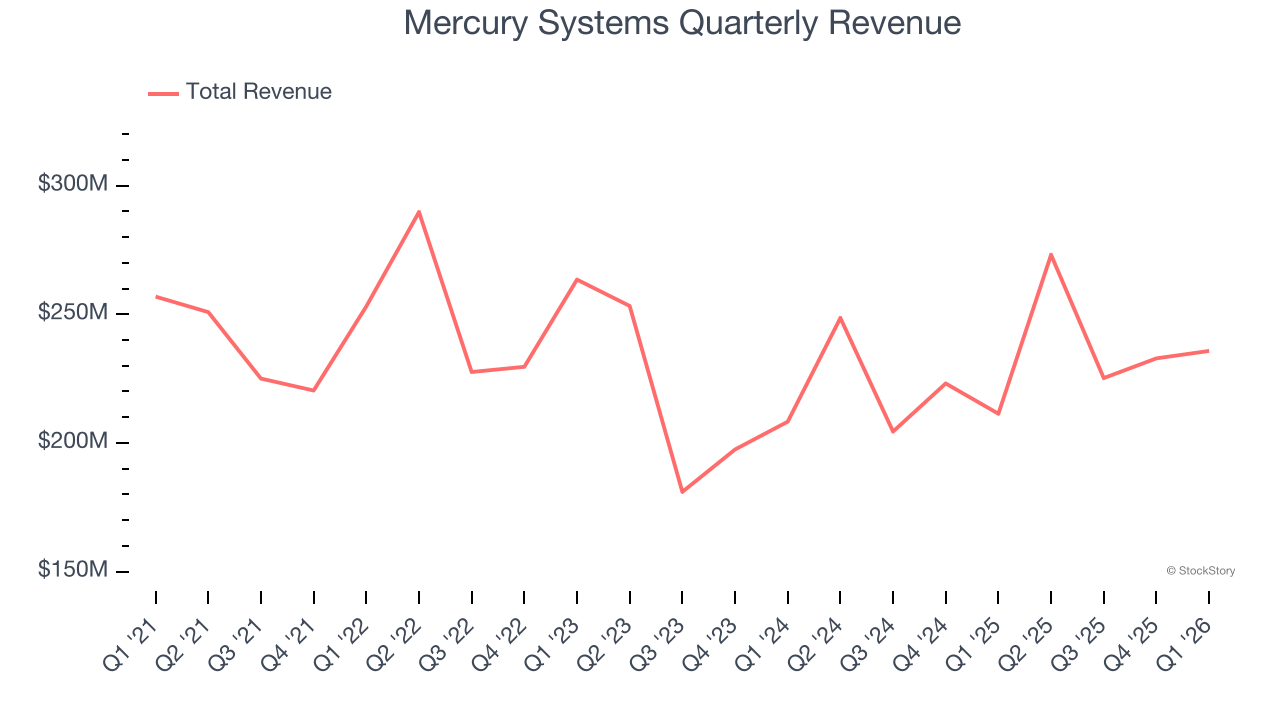

Aerospace and defense company Mercury Systems (NASDAQ: MRCY) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 11.5% year on year to $235.8 million. Its non-GAAP profit of $0.27 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Mercury Systems? Find out by accessing our full research report, it’s free.

Mercury Systems (MRCY) Q1 CY2026 Highlights:

- Revenue: $235.8 million vs analyst estimates of $206.4 million (11.5% year-on-year growth, 14.2% beat)

- Adjusted EPS: $0.27 vs analyst estimates of $0.07 (significant beat)

- Adjusted EBITDA: $36.09 million vs analyst estimates of $21.52 million (15.3% margin, 67.7% beat)

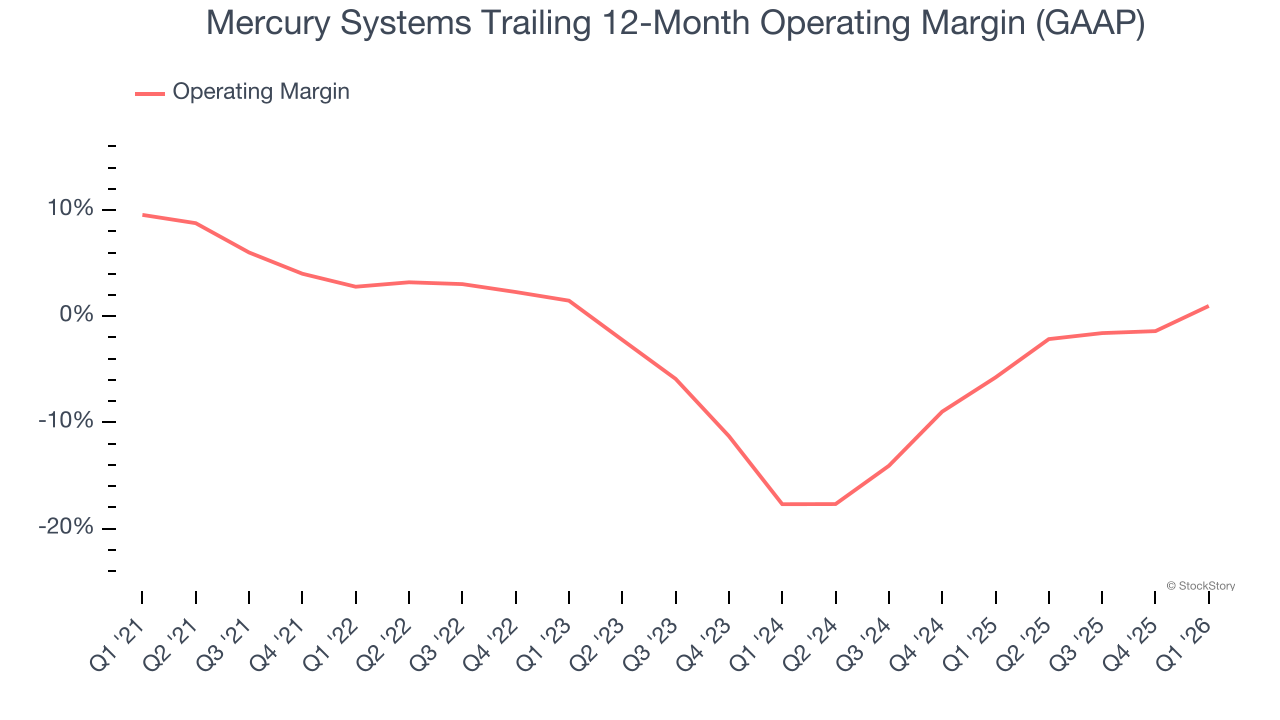

- Operating Margin: 2.2%, up from -8.2% in the same quarter last year

- Free Cash Flow was -$1.82 million, down from $24.06 million in the same quarter last year

- Backlog: $1.6 billion at quarter end, up 19.4% year on year

- Market Capitalization: $4.71 billion

“We delivered third quarter fiscal 2026 results that were ahead of our expectations, with significant year-over-year growth in backlog, revenue, and adjusted EBITDA,” said Bill Ballhaus, Mercury’s Chairman and CEO.

Company Overview

Founded in 1981, Mercury Systems (NASDAQ: MRCY) specializes in providing processing subsystems and components for primarily defense applications.

Revenue Growth

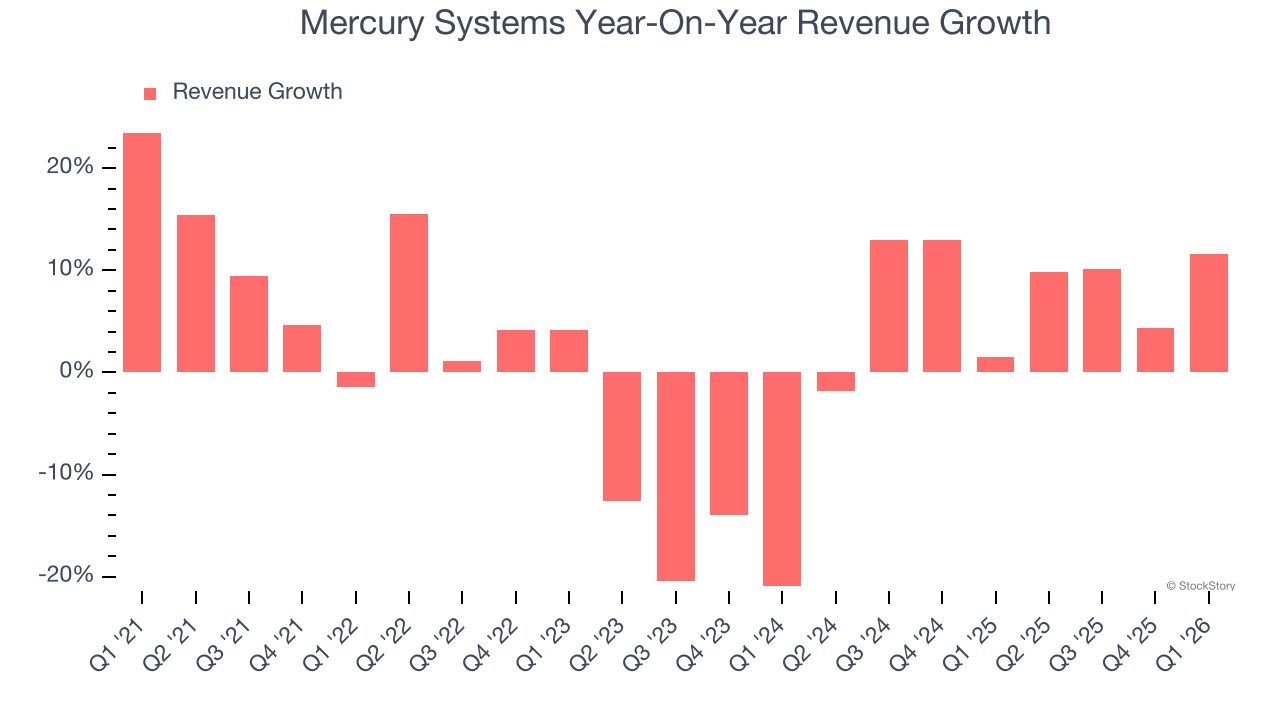

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Mercury Systems’s 1.7% annualized revenue growth over the last five years was sluggish. This fell short of our benchmarks and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Mercury Systems’s annualized revenue growth of 7.3% over the last two years is above its five-year trend, which is encouraging.

This quarter, Mercury Systems reported year-on-year revenue growth of 11.5%, and its $235.8 million of revenue exceeded Wall Street’s estimates by 14.2%.

Looking ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

ALSO WORTH WATCHING: Nvidia’s Quiet Partner. Nvidia’s chips cost a hundred grand. The connectors that make them work cost even more. One company makes them all.

Every AI server needs specialized infrastructure the chip companies don’t make. High-speed cables. Power connectors. Thermal sensors. This 90-year-old company built a monopoly on it. The AI boom just started. This stock is still flying under the radar. Claim The Stock Ticker Here for FREE.

Operating Margin

Although Mercury Systems was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3.2% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Mercury Systems’s operating margin decreased by 1.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Mercury Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Mercury Systems generated an operating margin profit margin of 2.2%, up 10.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

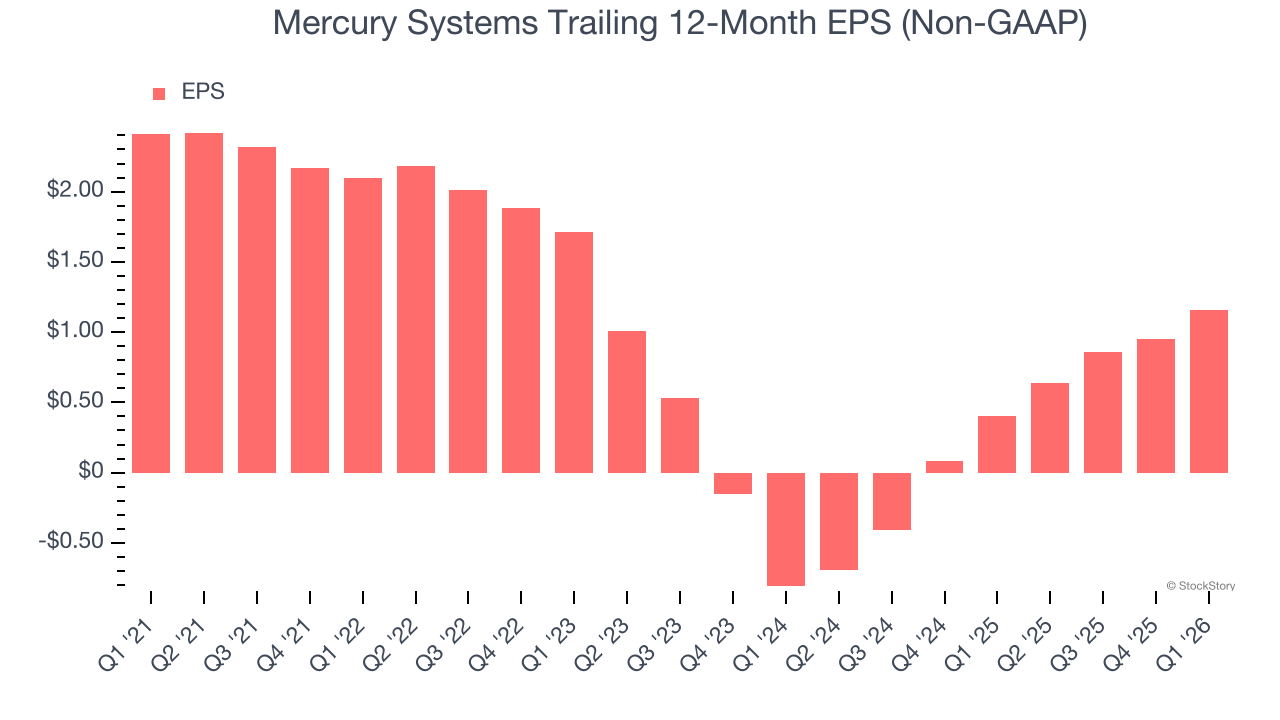

Sadly for Mercury Systems, its EPS declined by 13.6% annually over the last five years while its revenue grew by 1.7%. This tells us the company became less profitable on a per-share basis as it expanded.

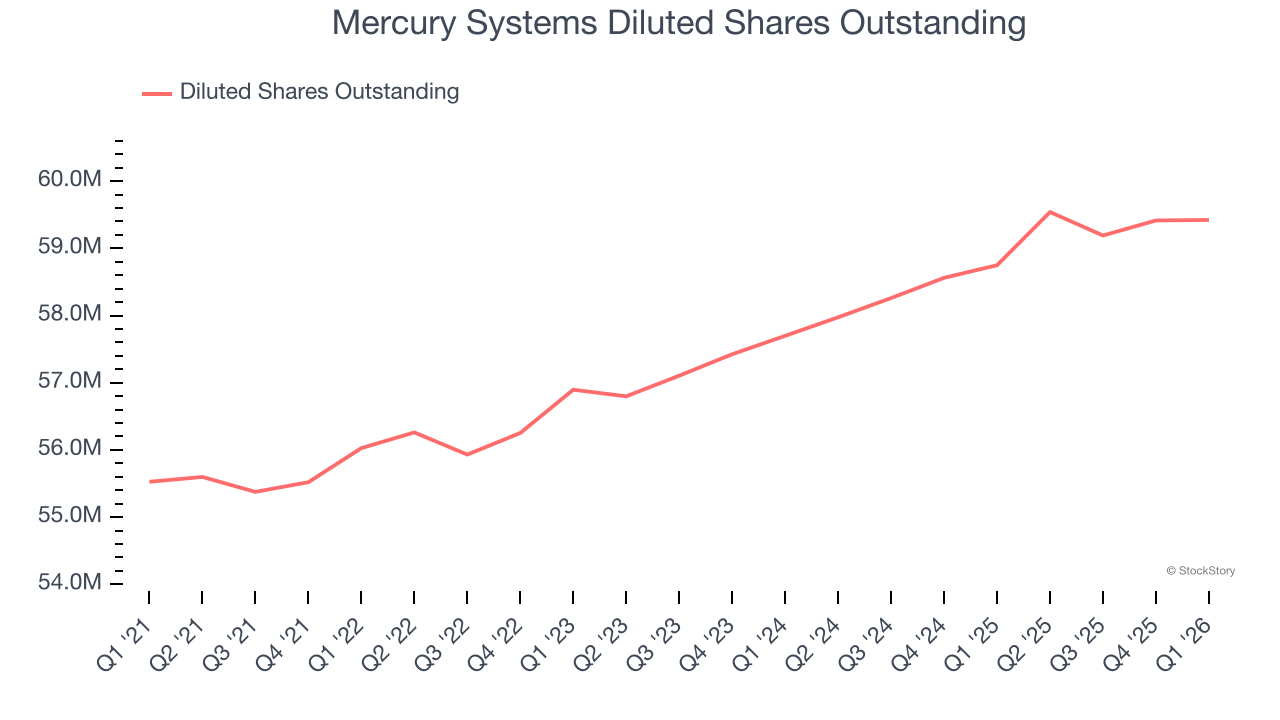

Diving into the nuances of Mercury Systems’s earnings can give us a better understanding of its performance. As we mentioned earlier, Mercury Systems’s operating margin expanded this quarter but declined by 1.8 percentage points over the last five years. Its share count also grew by 7%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Mercury Systems, its two-year annual EPS growth of 85.3% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Mercury Systems reported adjusted EPS of $0.27, up from $0.06 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Mercury Systems’s full-year EPS of $1.16 to grow 21.8%.

Key Takeaways from Mercury Systems’s Q1 Results

It was good to see Mercury Systems beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 1.8% to $84.57 immediately after reporting.

Mercury Systems put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).