Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Flowserve (NYSE: FLS) and its peers.

Gas and liquid handling companies possess the technical know-how and specialized equipment to handle valuable (and sometimes dangerous) substances. Lately, water conservation and carbon capture–which requires hydrogen and other gasses as well as specialized infrastructure–have been trending up, creating new demand for products such as filters, pumps, and valves. On the other hand, gas and liquid handling companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 11 gas and liquid handling stocks we track reported a satisfactory Q1. As a group, revenues beat analysts’ consensus estimates by 1.3% while next quarter’s revenue guidance was 0.8% below.

While some gas and liquid handling stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3% since the latest earnings results.

Flowserve (NYSE: FLS)

Manufacturing the largest pump ever built for nuclear power generation, Flowserve (NYSE: FLS) manufactures and sells flow control equipment for various industries.

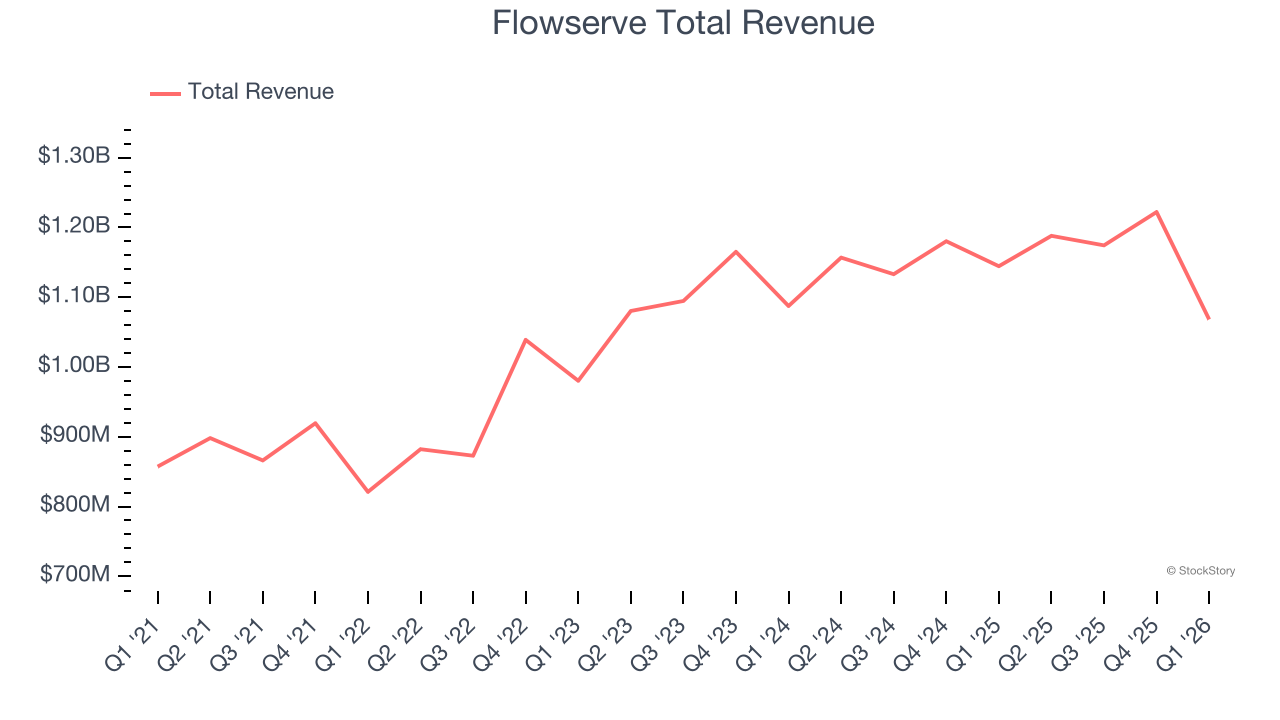

Flowserve reported revenues of $1.07 billion, down 6.7% year on year. This print fell short of analysts’ expectations by 8.8%. Overall, it was a mixed quarter for the company with a decent beat of analysts’ EBITDA estimates but a significant miss of analysts’ revenue estimates.

Flowserve delivered the weakest performance against analyst estimates and slowest revenue growth of the whole group. Unsurprisingly, the stock is down 12.4% since reporting and currently trades at $73.76.

Read our full report on Flowserve here, it’s free.

Best Q1: Gorman-Rupp (NYSE: GRC)

Powering fluid dynamics since 1934, Gorman-Rupp (NYSE: GRC) has evolved from its Ohio origins into a global manufacturer and seller of pumps and pump systems.

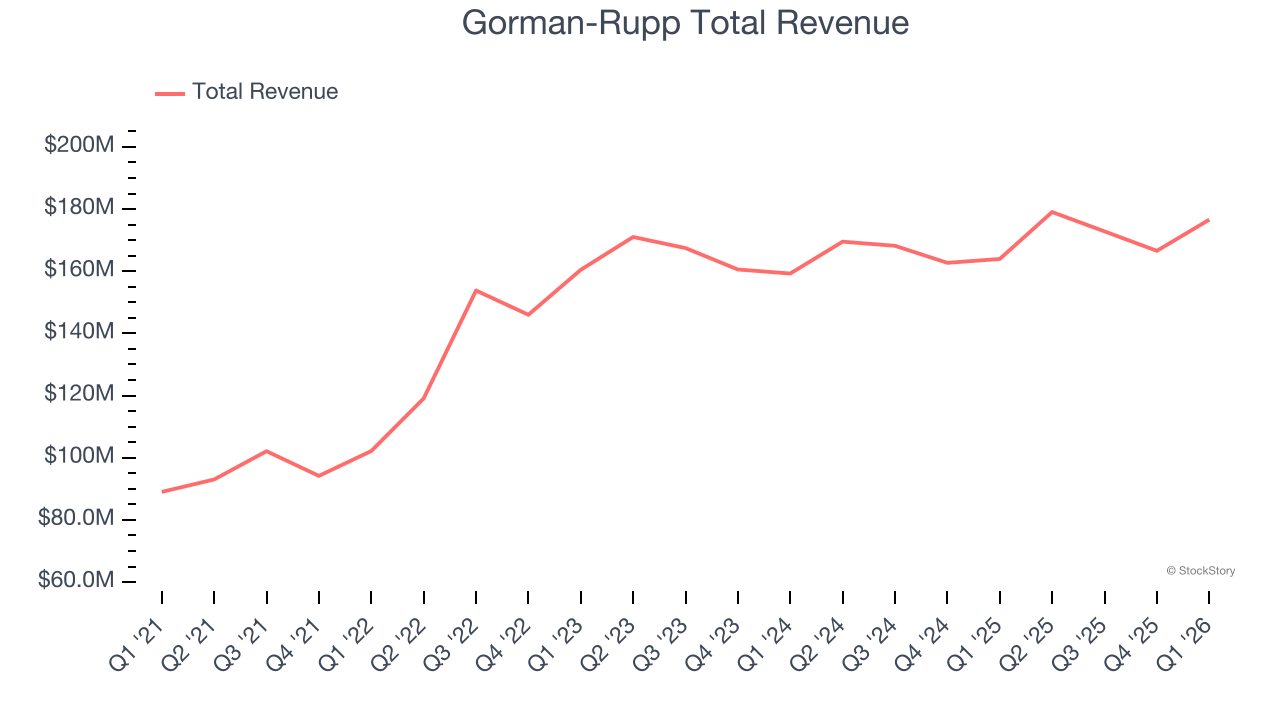

Gorman-Rupp reported revenues of $176.6 million, up 7.7% year on year, outperforming analysts’ expectations by 3.5%. The business had an incredible quarter with a beat of analysts’ EPS and EBITDA estimates.

The market seems happy with the results as the stock is up 9.5% since reporting. It currently trades at $72.50.

Is now the time to buy Gorman-Rupp? Access our full analysis of the earnings results here, it’s free.

Weakest Q1: Graco (NYSE: GGG)

Founded in 1926, Graco (NYSE: GGG) is an industrial company specializing in the development and manufacturing of fluid-handling systems and products.

Graco reported revenues of $540.1 million, up 2.2% year on year, falling short of analysts’ expectations by 3.9%. It was a disappointing quarter as it posted a significant miss of analysts’ revenue and adjusted operating income estimates.

As expected, the stock is down 10.4% since the results and currently trades at $76.68.

Read our full analysis of Graco’s results here.

ITT (NYSE: ITT)

Playing a crucial role in the development of the first transatlantic television transmission in 1956, ITT (NYSE: ITT) provides motion and fluid handling equipment for various industries

ITT reported revenues of $1.21 billion, up 32.7% year on year. This print topped analysts’ expectations by 9.8%. Overall, it was an exceptional quarter as it also logged an impressive beat of analysts’ EBITDA estimates.

ITT pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. The stock is down 5.5% since reporting and currently trades at $200.93.

Read our full, actionable report on ITT here, it’s free.

Helios (NYSE: HLIO)

Founded on the principle of treating others as one wants to be treated, Helios (NYSE: HLIO) designs, manufactures, and sells motion and electronic control components for various sectors.

Helios reported revenues of $228.4 million, up 16.8% year on year. This result beat analysts’ expectations by 3.7%. It was a very strong quarter as it also produced EPS guidance for next quarter exceeding analysts’ expectations.

Helios had the weakest full-year guidance update among its peers. The stock is up 20.9% since reporting and currently trades at $82.21.

Read our full, actionable report on Helios here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.