Crane currently trades at $173.48 per share and has shown little upside over the past six months, posting a small loss of 3%. The stock also fell short of the S&P 500’s 11.3% gain during that period.

Given the weaker price action, is now a good time to buy CR? Or should investors expect a bumpy road ahead? Find out in our full research report, it’s free.

Why Does Crane Spark Debate?

Based in Connecticut, Crane (NYSE: CR) is a diversified manufacturer of engineered industrial products, including fluid handling, and aerospace technologies.

Two Positive Attributes:

1. Projected Revenue Growth Is Remarkable

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite, though some deceleration is natural as businesses become larger.

Over the next 12 months, sell-side analysts expect Crane’s revenue to rise by 19.1%, an improvement versus its 3% annualized declines for the past five years. This projection is eye-popping and implies its newer products and services will spur better top-line performance.

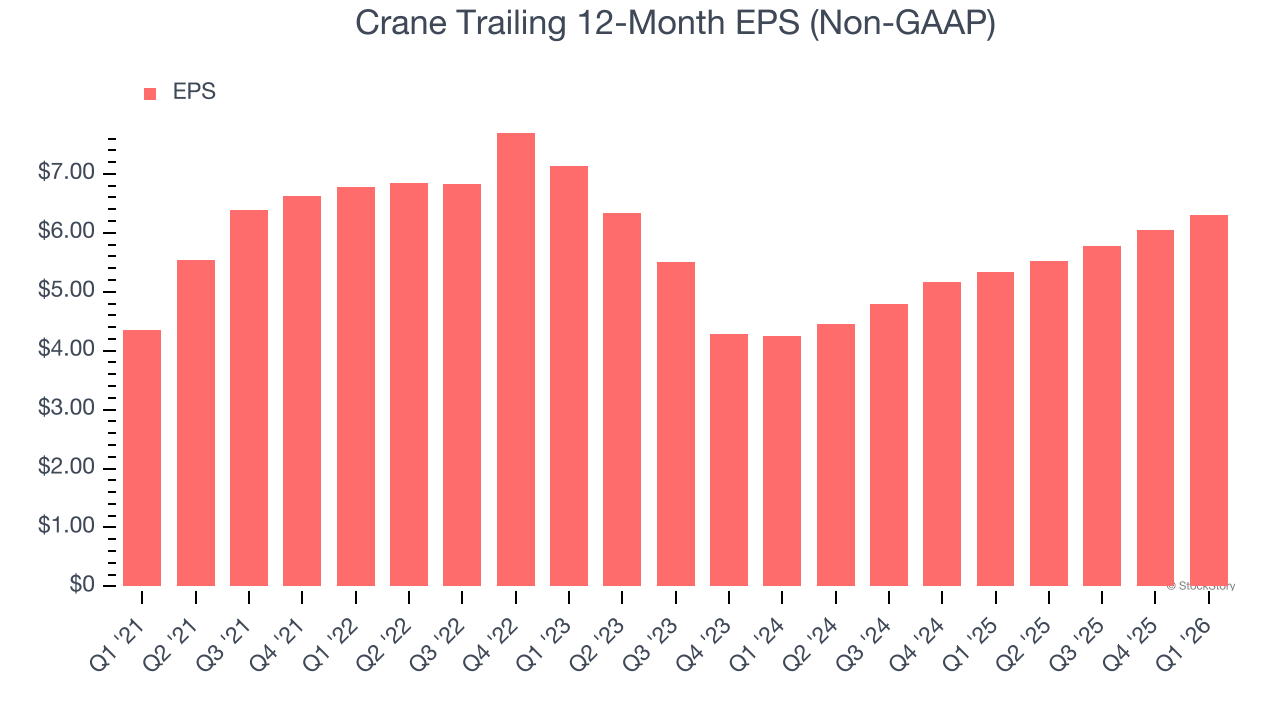

2. EPS Surges Higher Over the Last Two Years

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

Crane’s EPS grew at an astounding 21.8% compounded annual growth rate over the last two years, higher than its 9.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

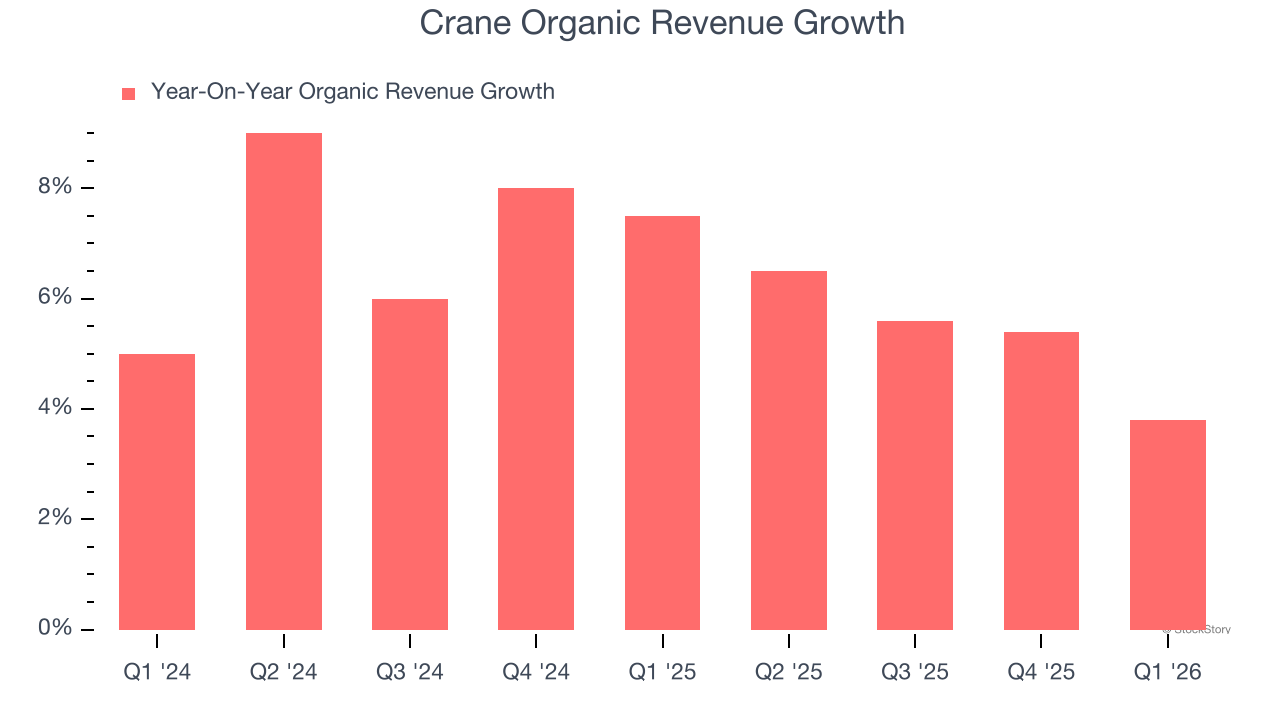

Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand General Industrial Machinery companies by analyzing their organic revenue. This metric gives visibility into Crane’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Crane’s organic revenue averaged 6.5% year-on-year growth. This performance slightly lagged the sector and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

Final Judgment

Crane has huge potential even though it has some open questions. With its shares underperforming the market lately, the stock trades at 24× forward P/E (or $173.48 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

Stocks We Like Even More Than Crane

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week - FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.