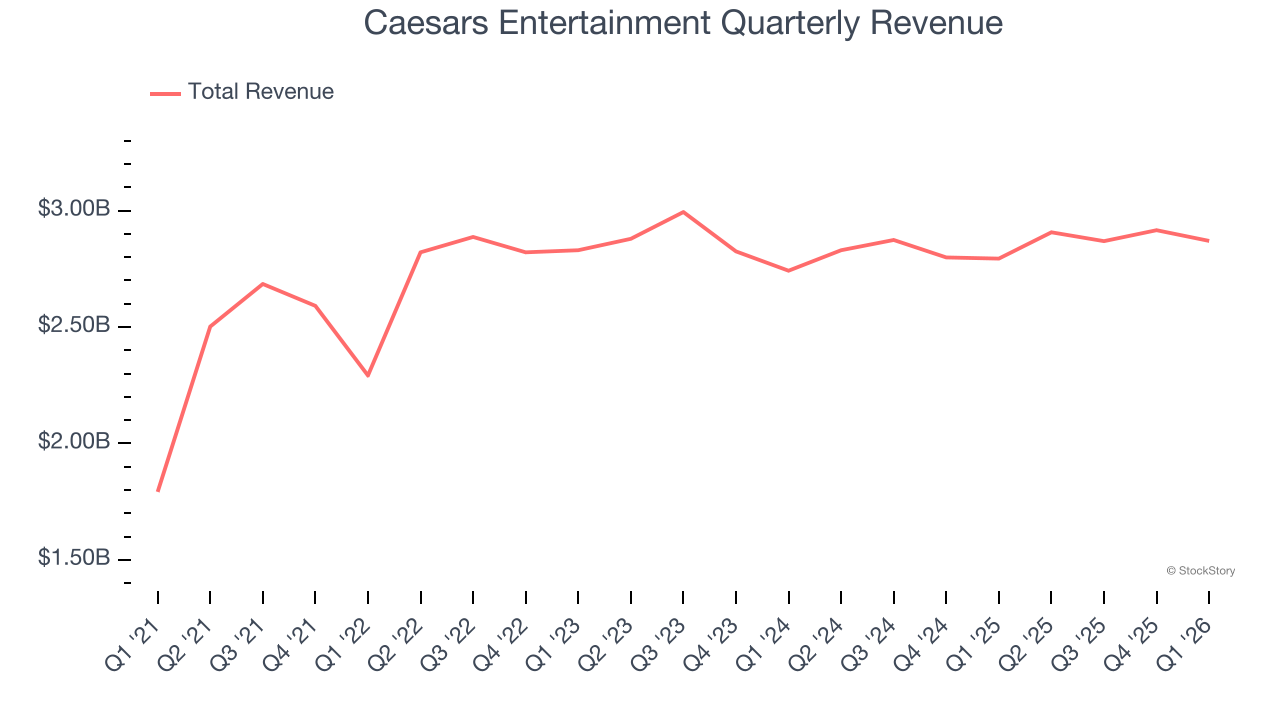

Hotel and casino entertainment company Caesars Entertainment (NASDAQ: CZR) announced better-than-expected revenue in Q1 CY2026, with sales up 2.7% year on year to $2.87 billion. Its GAAP loss of $0.48 per share was 97.9% below analysts’ consensus estimates.

Is now the time to buy Caesars Entertainment? Find out by accessing our full research report, it’s free.

Caesars Entertainment (CZR) Q1 CY2026 Highlights:

- Revenue: $2.87 billion vs analyst estimates of $2.85 billion (2.7% year-on-year growth, 0.6% beat)

- EPS (GAAP): -$0.48 vs analyst expectations of -$0.24 (97.9% miss)

- Adjusted EBITDA: $887 million vs analyst estimates of $880.2 million (30.9% margin, 0.8% beat)

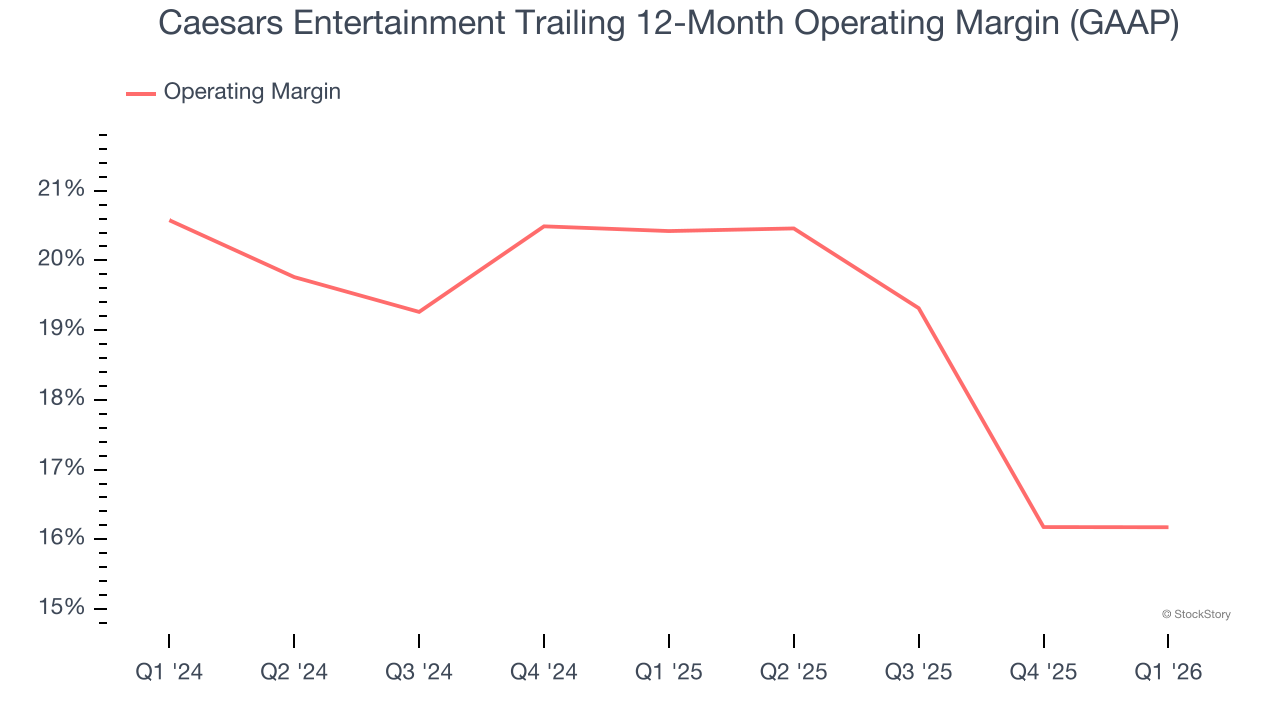

- Operating Margin: 17.4%, in line with the same quarter last year

- Market Capitalization: $5.70 billion

Tom Reeg, Chief Executive Officer of Caesars Entertainment, Inc., commented, “In the first quarter of 2026 we delivered growth in total net revenues and adjusted EBITDA versus last year. Caesars Digital revenue of $374 million and Adjusted EBITDA of $69 million achieved record first quarter results. In our Las Vegas segment, we experienced continued sequential improvement in trends and a significant improvement in the hospitality vertical with occupancy of 95.3% and year over year growth in Average Daily Rate. The Regional segment delivered improved adjusted EBITDA on a year over year basis after excluding the benefits of Super Bowl LX in New Orleans last year.”

Company Overview

Formerly Eldorado Resorts, Caesars Entertainment (NASDAQ: CZR) is a global gaming and hospitality company operating numerous casinos, hotels, and resort properties.

Revenue Growth

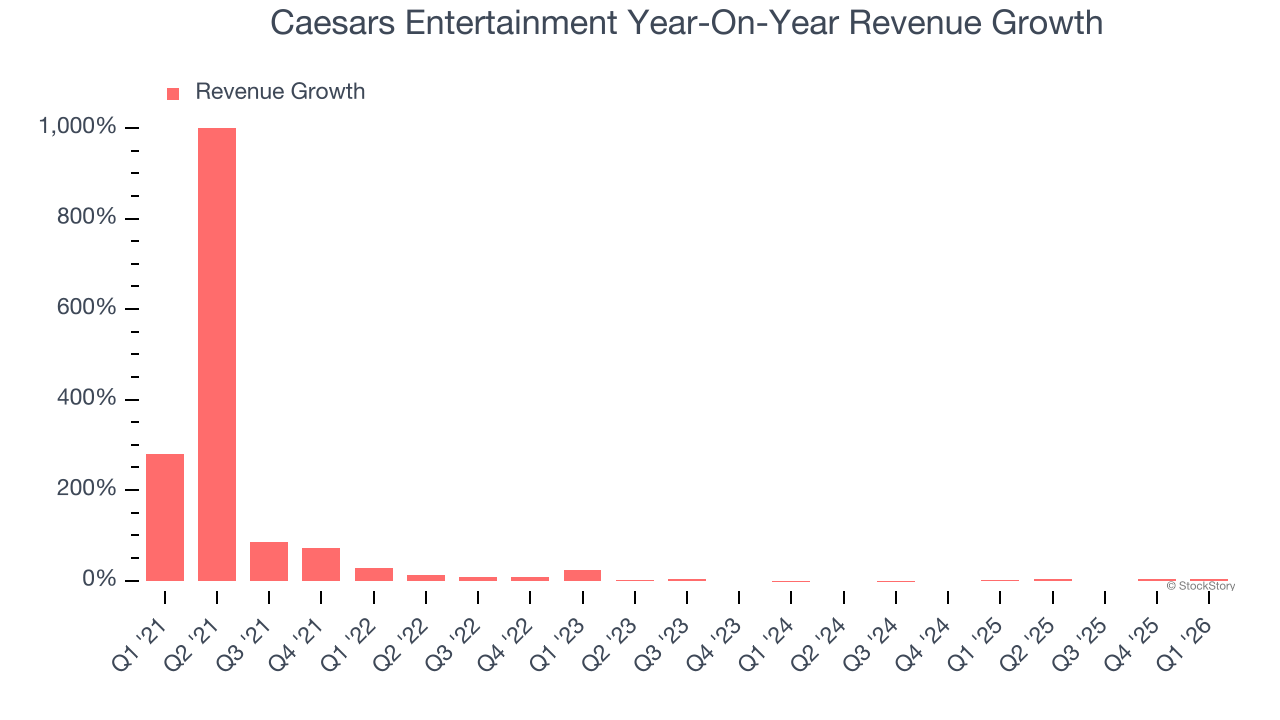

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Caesars Entertainment grew its sales at a 18.9% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Caesars Entertainment’s recent performance shows its demand has slowed as its revenue was flat over the last two years. Note that COVID hurt Caesars Entertainment’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

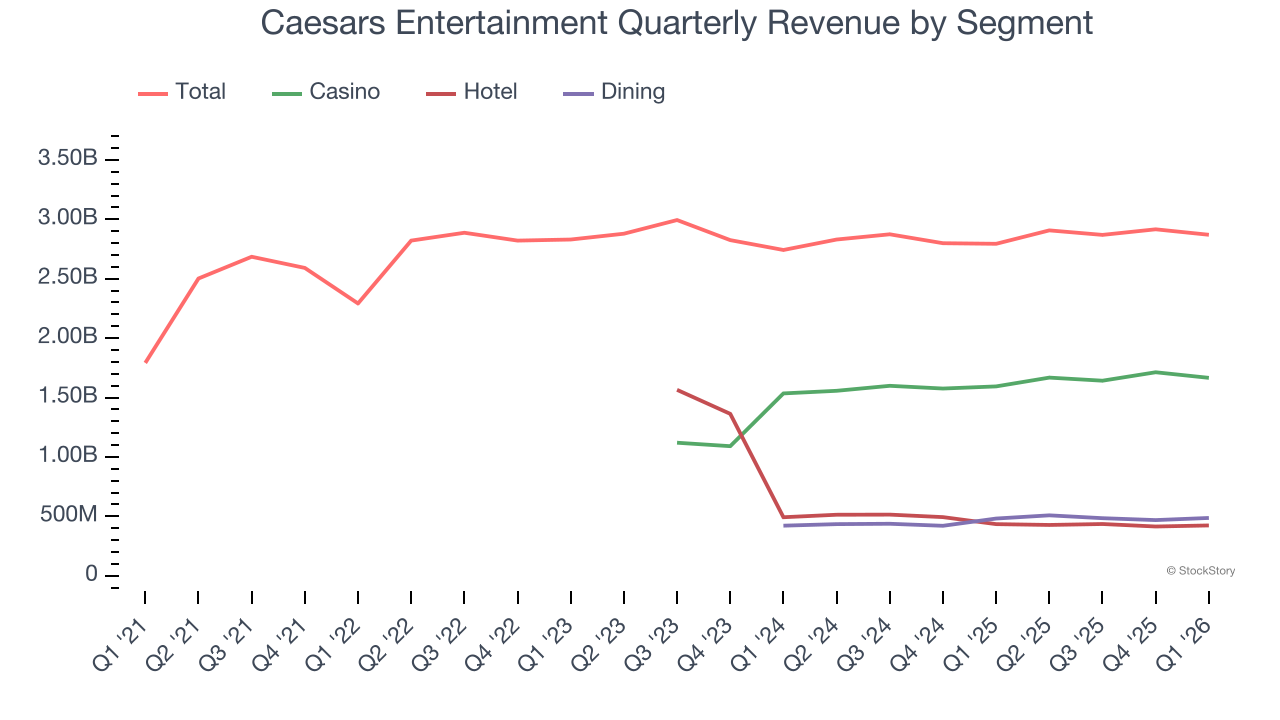

We can dig further into the company’s revenue dynamics by analyzing its three most important segments: Casino, Hotel, and Dining, which are 58%, 14.8%, and 17% of revenue. Over the last two years, Caesars Entertainment’s Casino (Poker, Blackjack) and Dining (food and beverage) revenues averaged year-on-year growth of 16.3% and 10.9%. On the other hand, its Hotel revenue (overnight bookings) averaged 27.6% declines.

This quarter, Caesars Entertainment reported modest year-on-year revenue growth of 2.7% but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

WHILE YOU’RE HERE: The Next Palantir? One satellite company captures images of every point on Earth. Every single day. The Pentagon wants it. Hedge funds are using it to beat earnings. You’ve probably never heard of it.

This is what the early days of Palantir looked like before it became a $437 billion giant. Same playbook. Different technology. If you missed Palantir, you need to see this. Claim The Stock Ticker for Free HERE.

Operating Margin

Caesars Entertainment’s operating margin has been trending down over the last 12 months and averaged 18.3% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

This quarter, Caesars Entertainment generated an operating margin profit margin of 17.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

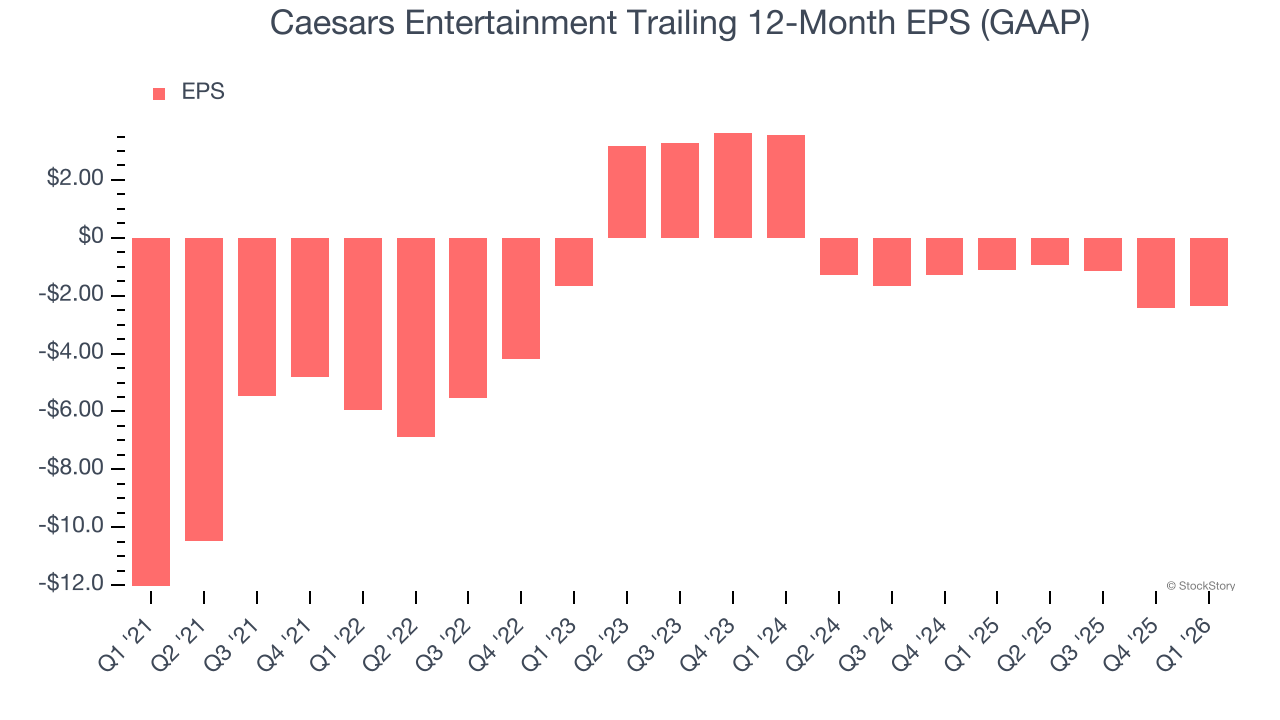

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Caesars Entertainment’s full-year earnings are still negative, it reduced its losses and improved its EPS by 27.8% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability.

In Q1, Caesars Entertainment reported EPS of negative $0.48, up from negative $0.54 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Caesars Entertainment to improve its earnings losses. Analysts forecast its full-year EPS of negative $2.37 will advance to negative $0.06.

Key Takeaways from Caesars Entertainment’s Q1 Results

It was encouraging to see Caesars Entertainment beat analysts’ adjusted operating income expectations this quarter. On the other hand, its EPS missed. Overall, this was a softer quarter. The stock remained flat at $27.50 immediately following the results.

Should you buy the stock or not? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).