Casella Waste Systems currently trades at $82.10 per share and has shown little upside over the past six months, posting a small loss of 4.3%. The stock also fell short of the S&P 500’s 5.4% gain during that period.

Is there a buying opportunity in Casella Waste Systems, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Casella Waste Systems Not Exciting?

We're swiping left on Casella Waste Systems for now. Here are three reasons why CWST doesn't excite us and a stock we'd rather own.

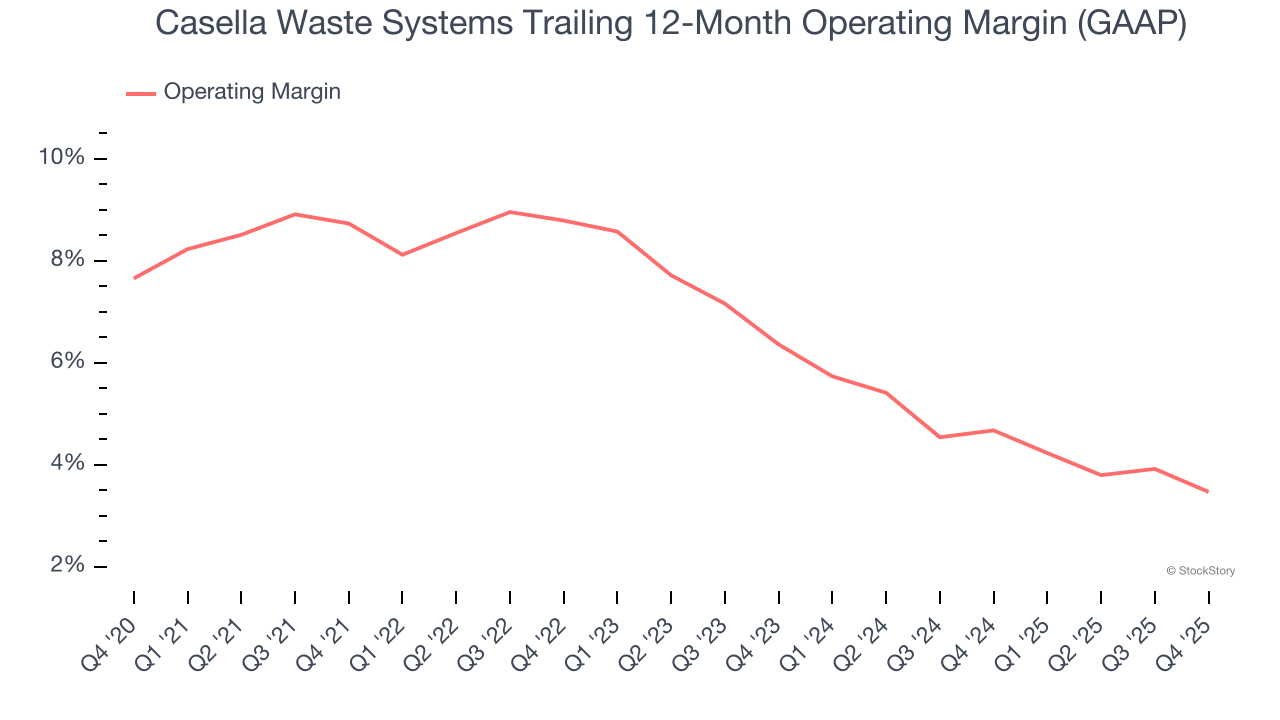

1. Shrinking Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, Casella Waste Systems’s operating margin decreased by 5.3 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Casella Waste Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was 3.5%.

2. Previous Growth Initiatives Haven’t Impressed

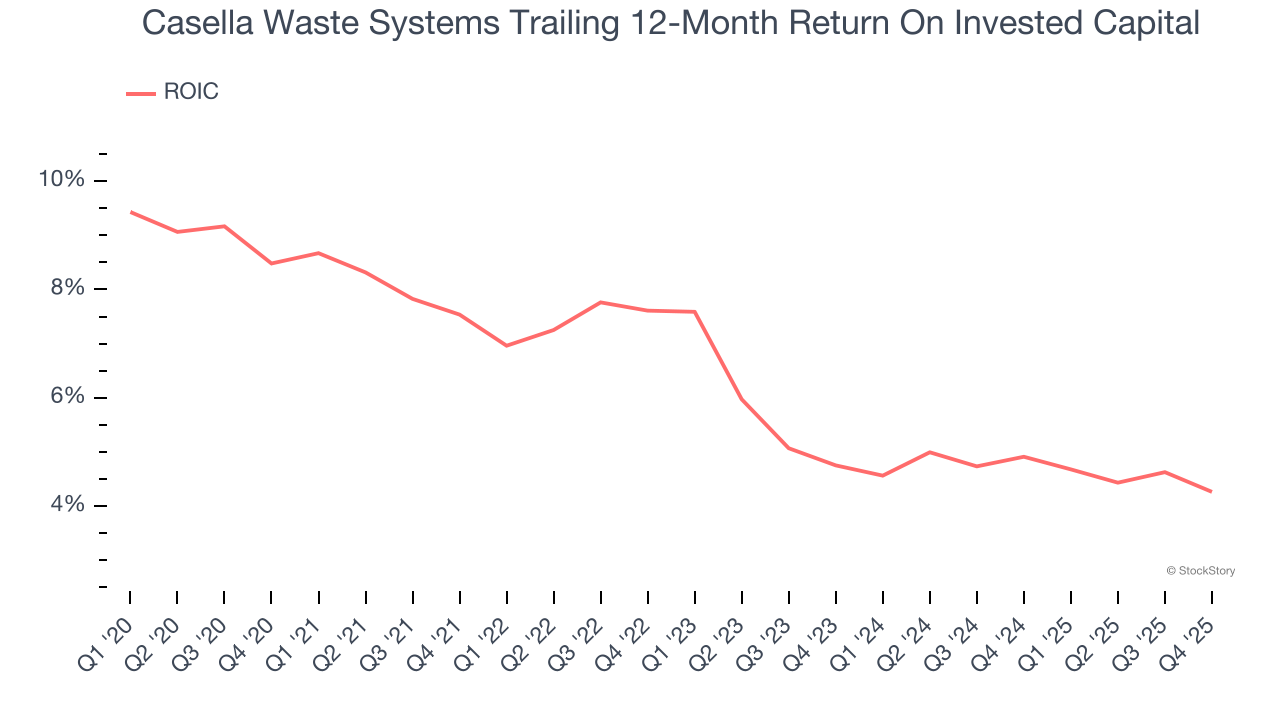

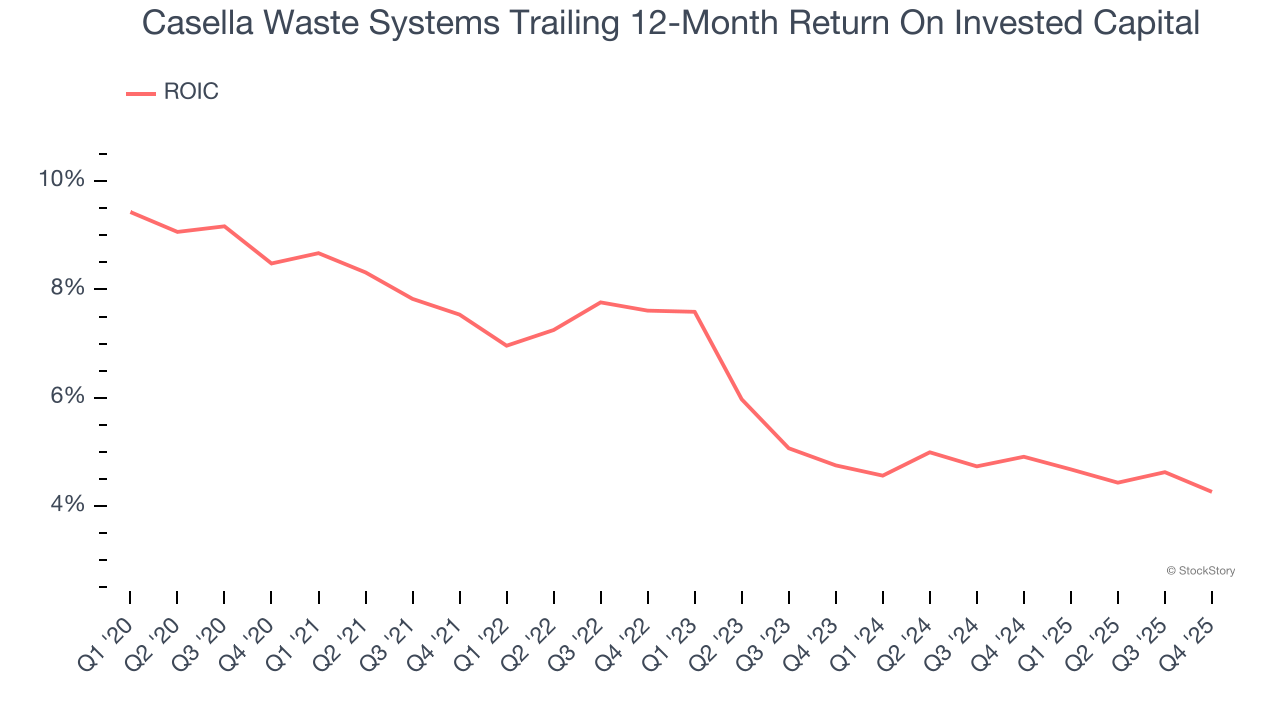

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Casella Waste Systems historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.8%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

3. New Investments Fail to Bear Fruit as ROIC Declines

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Casella Waste Systems’s ROIC averaged 3 percentage point decreases each year over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

Final Judgment

Casella Waste Systems isn’t a terrible business, but it doesn’t pass our quality test. With its shares lagging the market recently, the stock trades at 66× forward P/E (or $82.10 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of Casella Waste Systems

WHILE YOU’RE HERE: Top 9 Market-Beating Stocks. The best stocks don't just beat the market once. They do it again. And again. Robust revenue growth, rising free cash flow, returns on capital that leave their competition in the dust. The market has already rewarded these businesses.

But our AI platform says the party isn't over. Find out which 9 stocks made the cut this week — FREE. Get Our Top 9 Market-Beating Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.