What a brutal six months it’s been for Wingstop. The stock has dropped 40.6% and now trades at $156.05, rattling many shareholders. This might have investors contemplating their next move.

Given the weaker price action, is now a good time to buy WING? Find out in our full research report, it’s free.

Why Is WING a Good Business?

The passion project of two chicken wing aficionados in Texas, Wingstop (NASDAQ: WING) is a popular fast-food chain known for its flavorful and crispy chicken wings offered in a variety of sauces and seasonings.

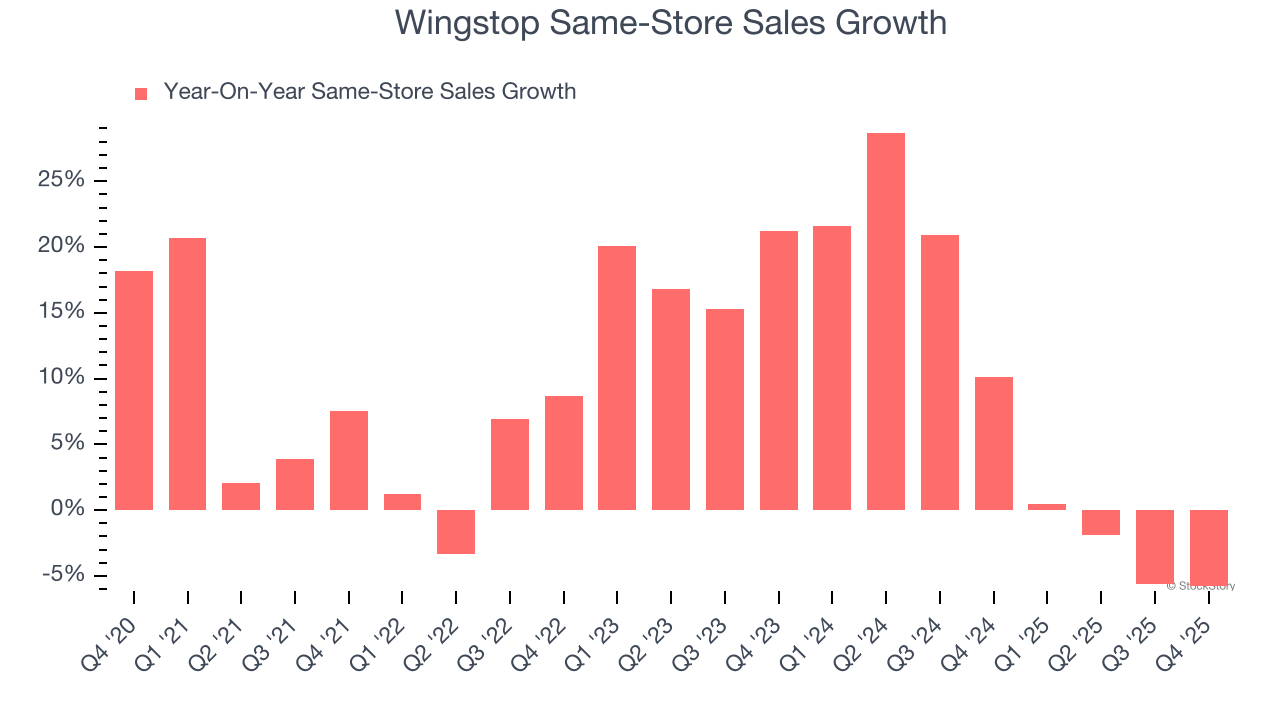

1. Surging Same-Store Sales Show Increasing Demand

Same-store sales show the change in sales at restaurants open for at least a year. This is a key performance indicator because it measures organic growth.

Wingstop has been one of the most successful restaurant chains over the last two years thanks to skyrocketing demand within its existing dining locations. On average, the company has posted exceptional year-on-year same-store sales growth of 8.6%.

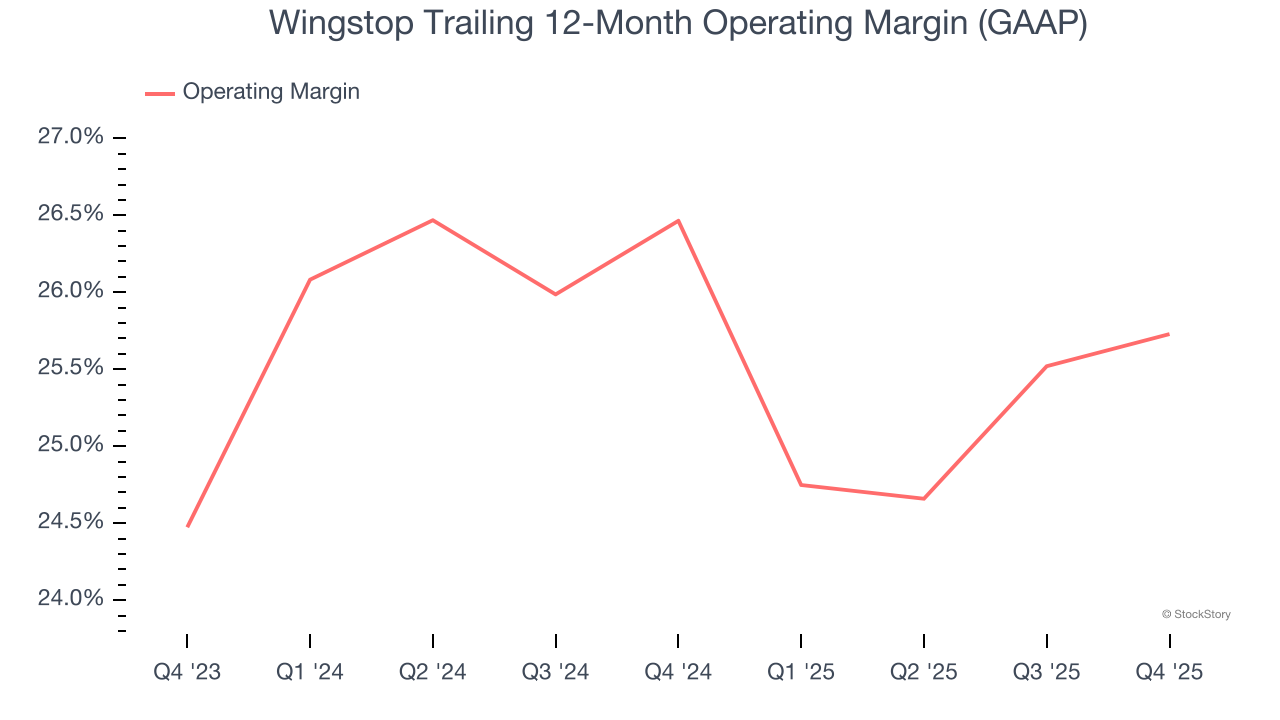

2. Operating Margin Reveals a Well-Run Organization

Operating margin is an important measure of profitability for restaurants as it accounts for all expenses keeping the business in motion, including food costs, wages, rent, advertising, and other administrative costs.

Wingstop’s operating margin has generally stayed the same over the last 12 months, averaging 26.1% over the last two years. This profitability was elite for a restaurant business thanks to its efficient cost structure and economies of scale. This is seen in its fast historical revenue growth and healthy gross margin, which is why we look at all three data points together.

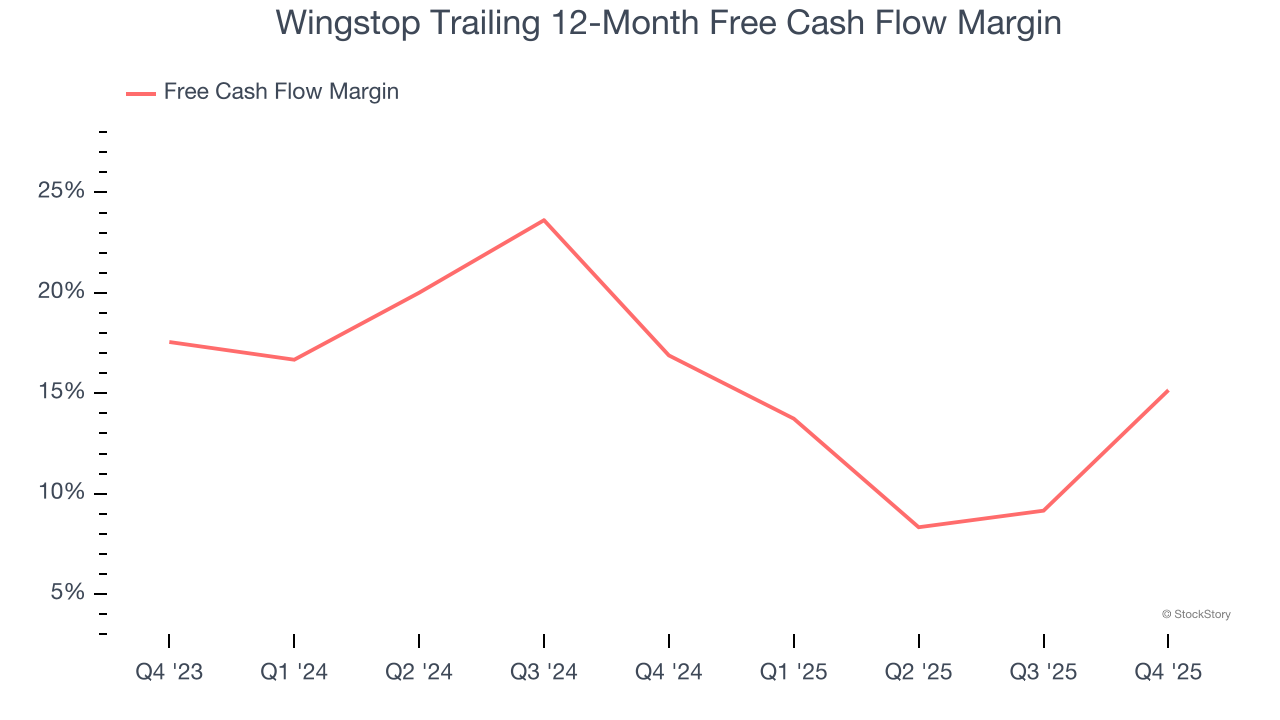

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Wingstop has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the restaurant sector, averaging 16% over the last two years.

Final Judgment

These are just a few reasons why we think Wingstop is an elite restaurant company. After the recent drawdown, the stock trades at 33× forward P/E (or $156.05 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.