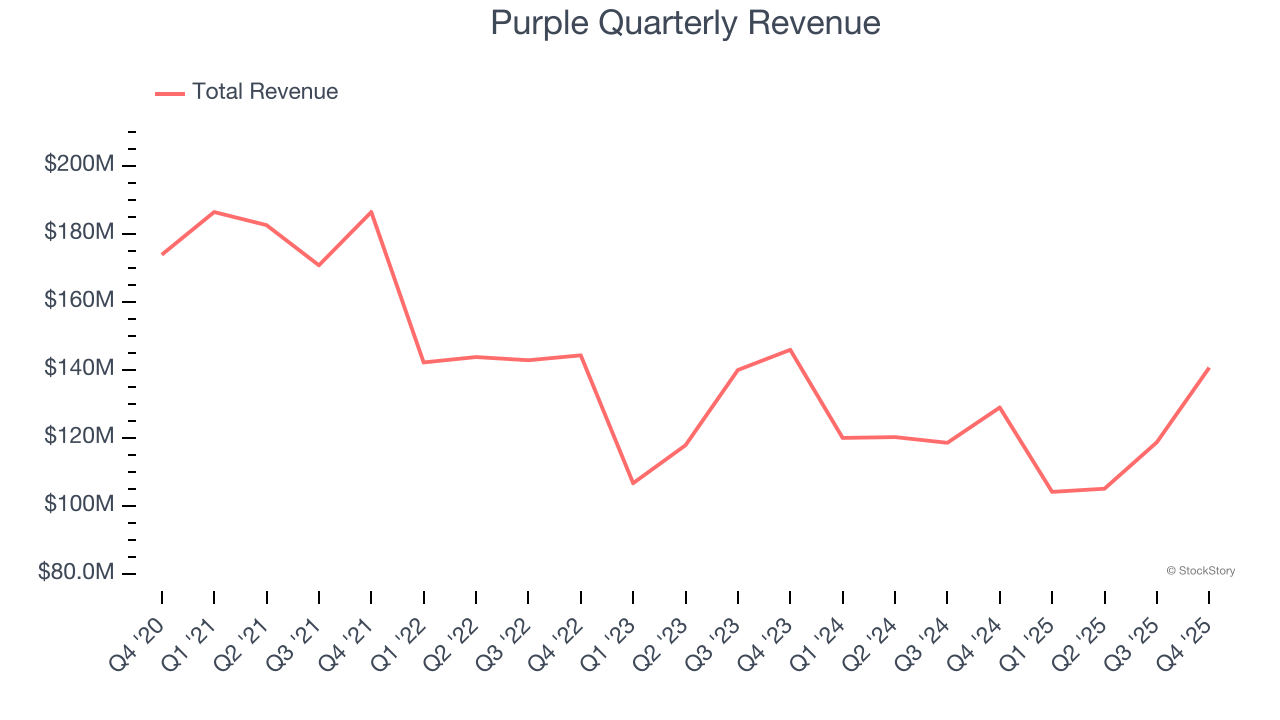

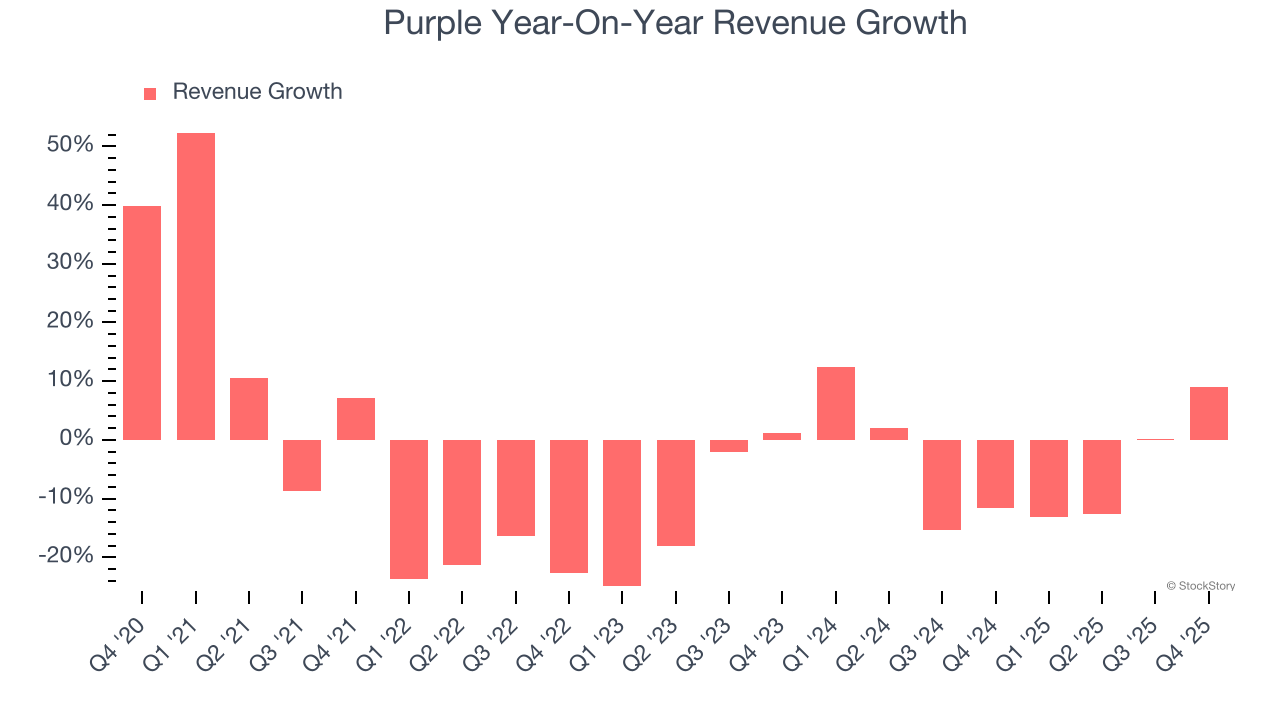

Bedding and comfort retailer Purple (NASDAQ: PRPL) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 9.1% year on year to $140.7 million. On the other hand, next quarter’s revenue guidance of $102.5 million was less impressive, coming in 15.1% below analysts’ estimates. Its non-GAAP loss of $0.02 per share was 63.6% above analysts’ consensus estimates.

Is now the time to buy Purple? Find out by accessing our full research report, it’s free.

Purple (PRPL) Q4 CY2025 Highlights:

- Revenue: $140.7 million vs analyst estimates of $139.8 million (9.1% year-on-year growth, 0.6% beat)

- Adjusted EPS: -$0.02 vs analyst estimates of -$0.06 (63.6% beat)

- Adjusted EBITDA: $8.85 million vs analyst estimates of $7.66 million (6.3% margin, 15.5% beat)

- Revenue Guidance for Q1 CY2026 is $102.5 million at the midpoint, below analyst estimates of $120.7 million

- EBITDA guidance for the upcoming financial year 2026 is $25 million at the midpoint, above analyst estimates of $11 million

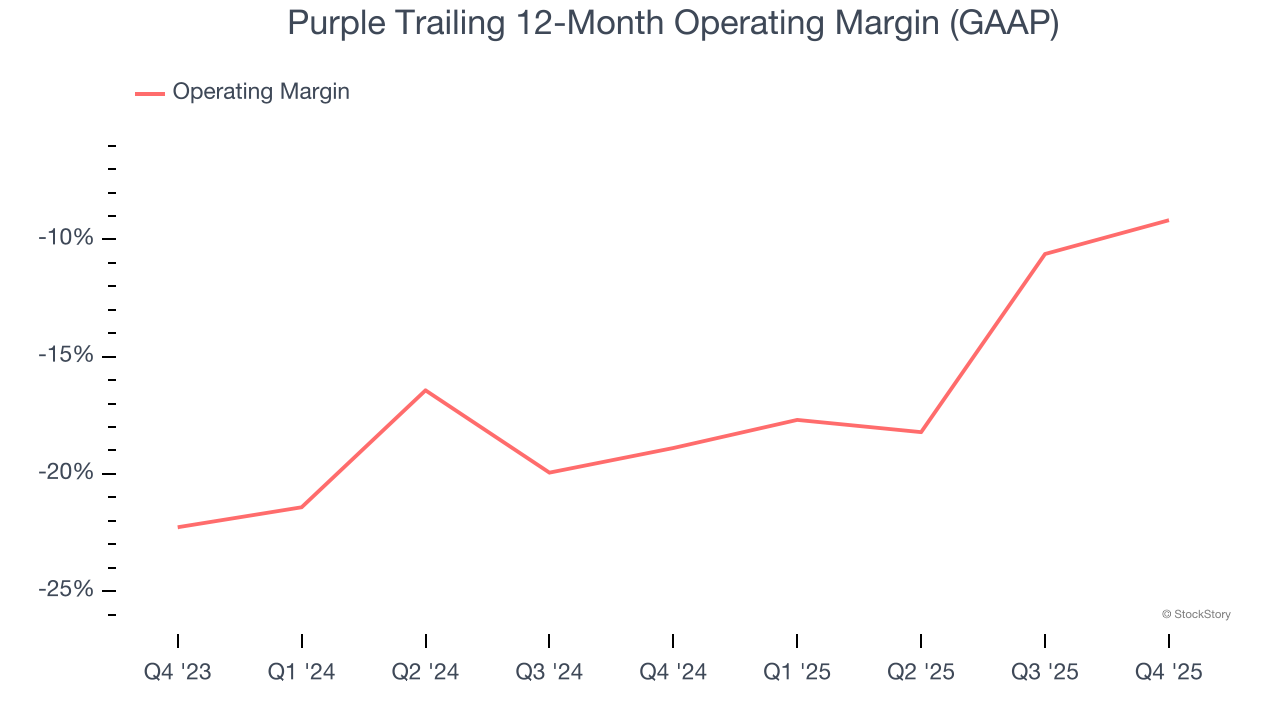

- Operating Margin: -1.6%, up from -6% in the same quarter last year

- Market Capitalization: $70.19 million

"2025 marked an important inflection point for Purple," said Rob DeMartini, CEO of Purple Innovation.

Company Overview

Founded by two brothers, Purple (NASDAQ: PRPL) creates sleep and home comfort products such as mattresses, pillows, and bedding accessories.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Purple’s demand was weak over the last five years as its sales fell at a 6.3% annual rate. This wasn’t a great result and is a sign of poor business quality.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Purple’s annualized revenue declines of 4.2% over the last two years suggest its demand continued shrinking.

This quarter, Purple reported year-on-year revenue growth of 9.1%, and its $140.7 million of revenue exceeded Wall Street’s estimates by 0.6%. Company management is currently guiding for a 1.6% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 15.7% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and indicates its newer products and services will fuel better top-line performance.

ONE MORE THING: 3 Hidden Platforms Growing 3X Faster than Amazon, Google, and PayPal. Amazon, Google, and Meta all followed the same playbook: Dominate an ignored market. Build an unbeatable moat. Scale until you’re unstoppable.

These three platforms are running that exact playbook right now. The early investors in Amazon made fortunes. The early investors in these could do the same. Get All 3 Stocks Here for FREE.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Purple’s operating margin has been trending up over the last 12 months, but it still averaged negative 14.1% over the last two years. This is due to its large expense base and inefficient cost structure.

Purple’s operating margin was negative 1.6% this quarter. The company's consistent lack of profits raise a flag.

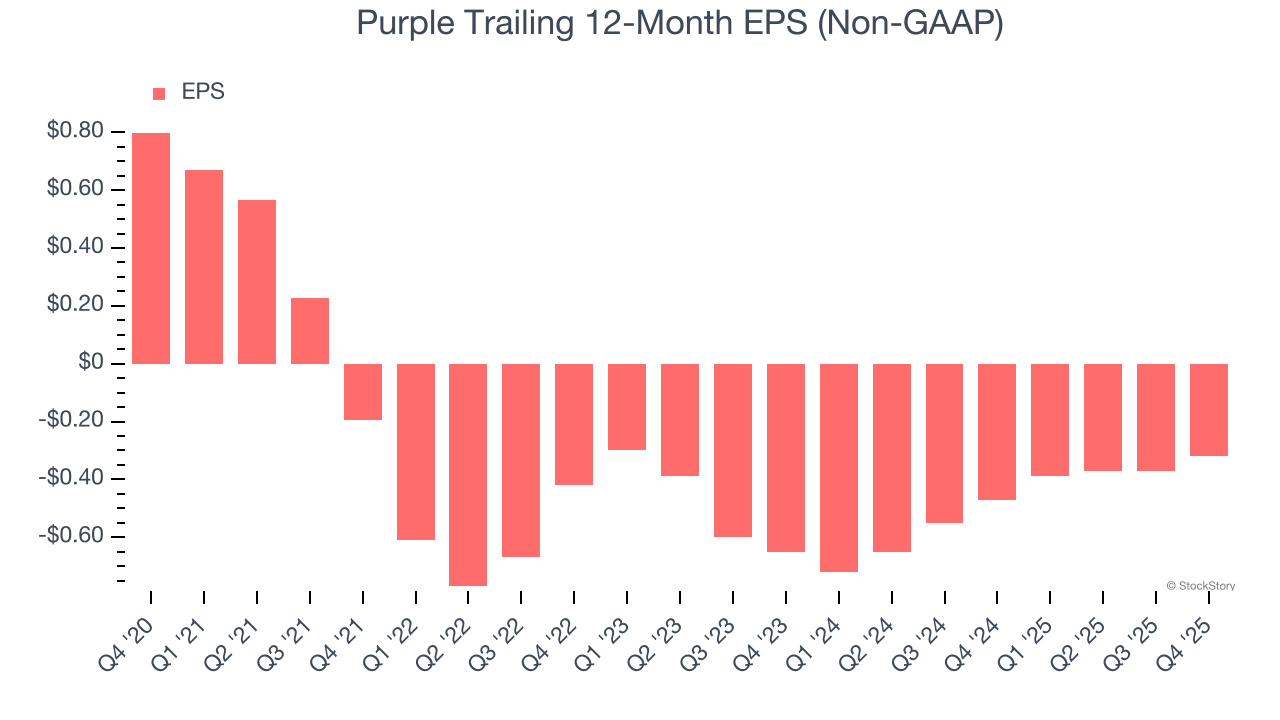

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Purple, its EPS declined by 19.1% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, Purple reported adjusted EPS of negative $0.02, up from negative $0.07 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Purple to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.32 will advance to negative $0.21.

Key Takeaways from Purple’s Q4 Results

It was good to see Purple beat analysts’ EPS expectations this quarter. We were also glad its full-year EBITDA guidance trumped Wall Street’s estimates. On the other hand, its full-year revenue guidance missed and its revenue guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a mixed quarter, but the market seems to be forgiving the revenue guidance miss and focusing more on the EBITDA guidance beat. The stock traded up 6.5% to $0.69 immediately after reporting.

So should you invest in Purple right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).