Astec trades at $49.45 per share and has stayed right on track with the overall market, gaining 6.5% over the last six months. At the same time, the S&P 500 has returned 3%.

Is now the time to buy Astec, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Astec Not Exciting?

We don't have much confidence in Astec. Here are three reasons you should be careful with ASTE and a stock we'd rather own.

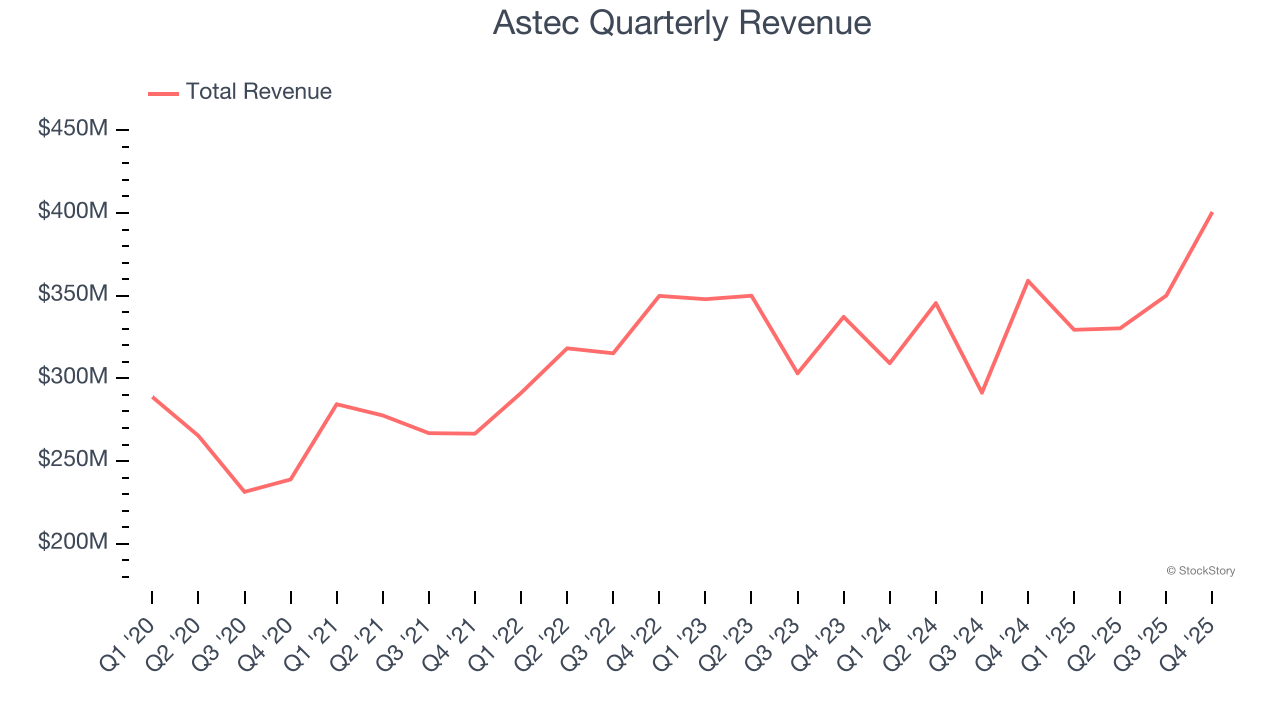

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Astec’s sales grew at a mediocre 6.6% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector.

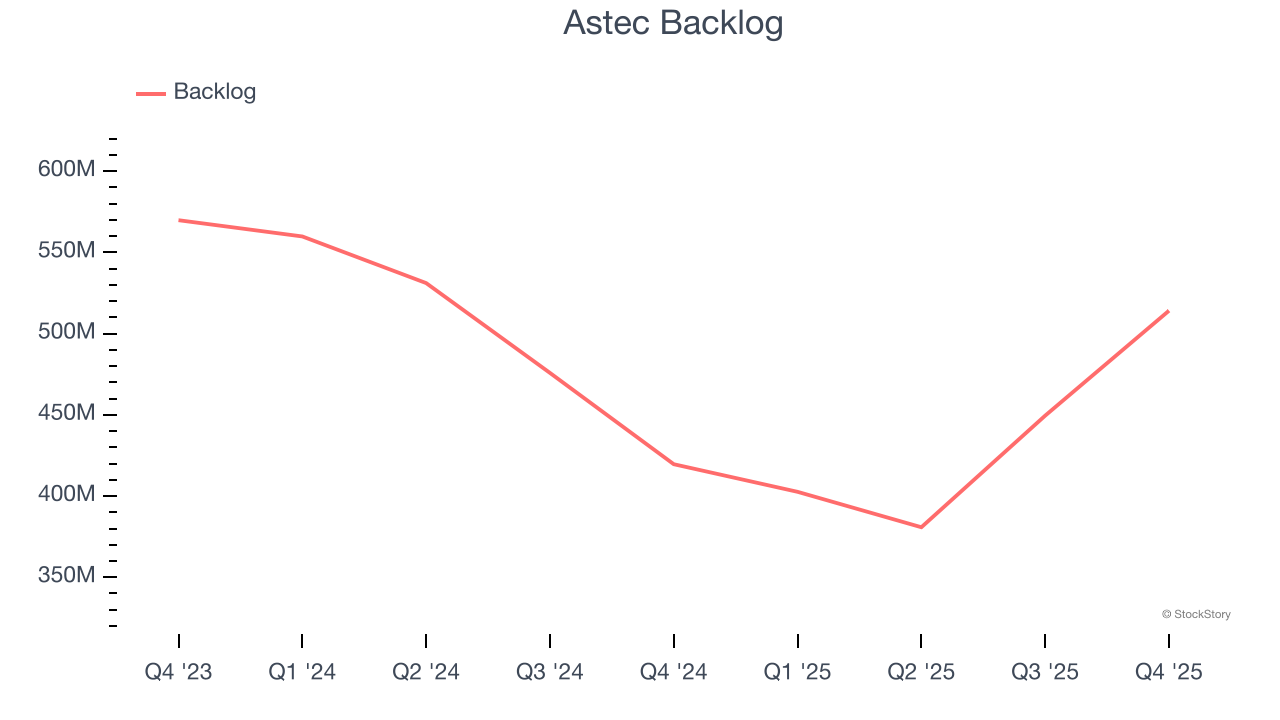

2. Backlog Declines as Orders Drop

Investors interested in Construction Machinery companies should track backlog in addition to reported revenue. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into Astec’s future revenue streams.

Astec’s backlog came in at $514.1 million in the latest quarter, and it averaged 13.1% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

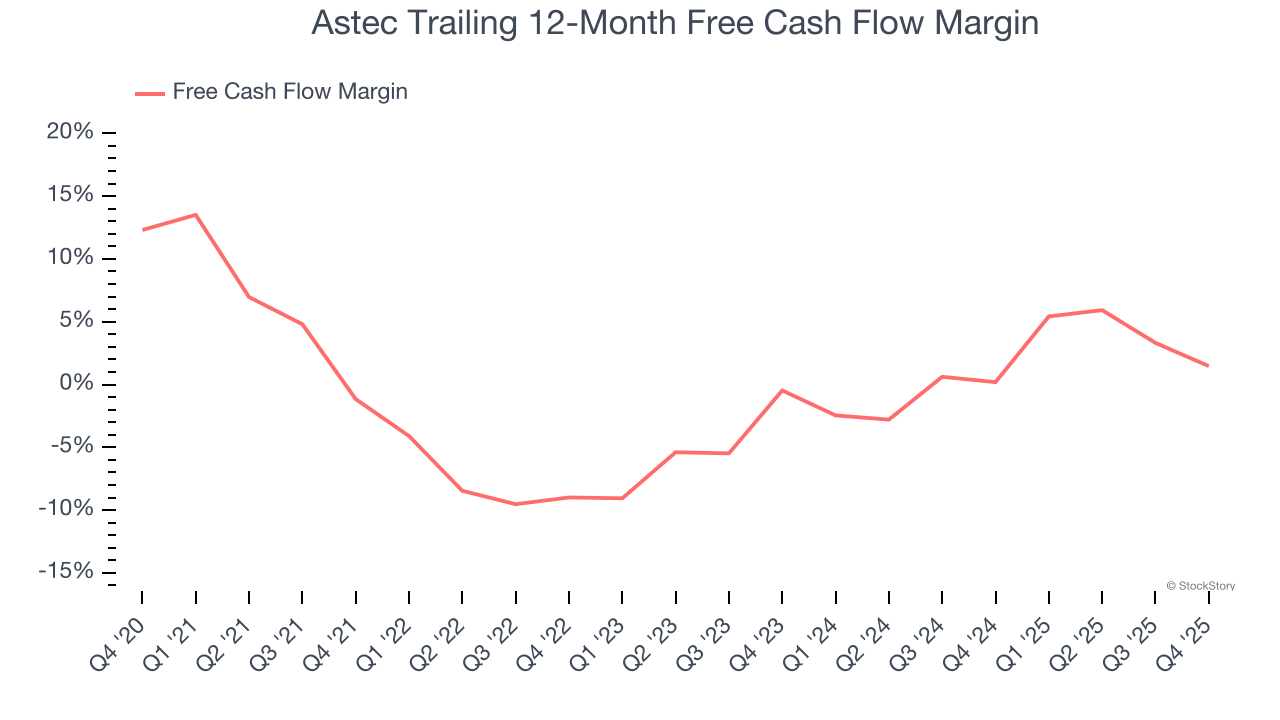

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Astec posted positive free cash flow this quarter, the broader story hasn’t been so clean. Astec’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.7%, meaning it lit $1.72 of cash on fire for every $100 in revenue.

Final Judgment

Astec isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 15.3× forward P/E (or $49.45 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now. Let us point you toward the most dominant software business in the world.

High-Quality Stocks for All Market Conditions

ONE MORE THING: Top 5 Growth Stocks. The biggest stock winners almost always had one thing in common before they ran. Revenue growing like crazy. Meta. CrowdStrike. Broadcom. Our AI flagged all three. They returned 315%, 314%, and 455%, respectively.

Find out which 5 stocks it's flagging for this month — FREE. Get Our Top 5 Growth Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.