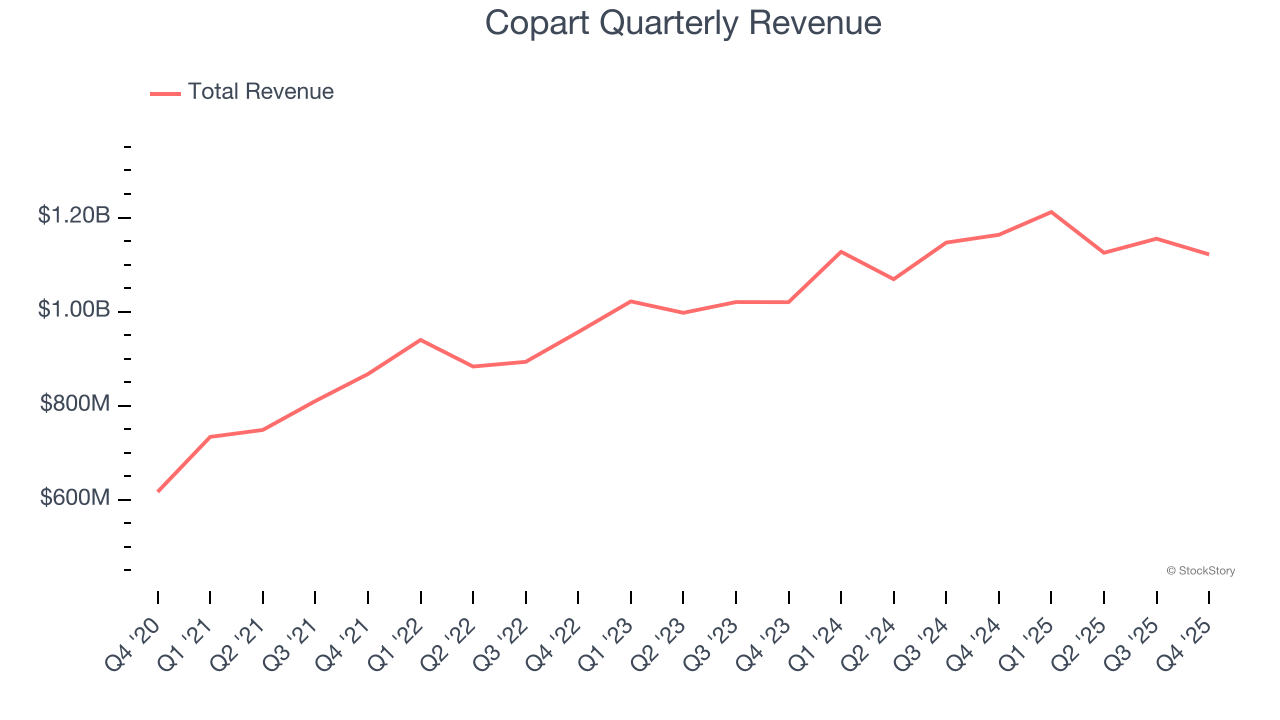

Online vehicle auction company Copart (NASDAQ: CPRT) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 3.6% year on year to $1.12 billion. Its GAAP profit of $0.36 per share was 7.5% below analysts’ consensus estimates.

Is now the time to buy Copart? Find out by accessing our full research report, it’s free.

Copart (CPRT) Q4 CY2025 Highlights:

- Revenue: $1.12 billion vs analyst estimates of $1.18 billion (3.6% year-on-year decline, 5% miss)

- EPS (GAAP): $0.36 vs analyst expectations of $0.39 (7.5% miss)

- Adjusted EBITDA: $434.9 million vs analyst estimates of $479.1 million (38.8% margin, 9.2% miss)

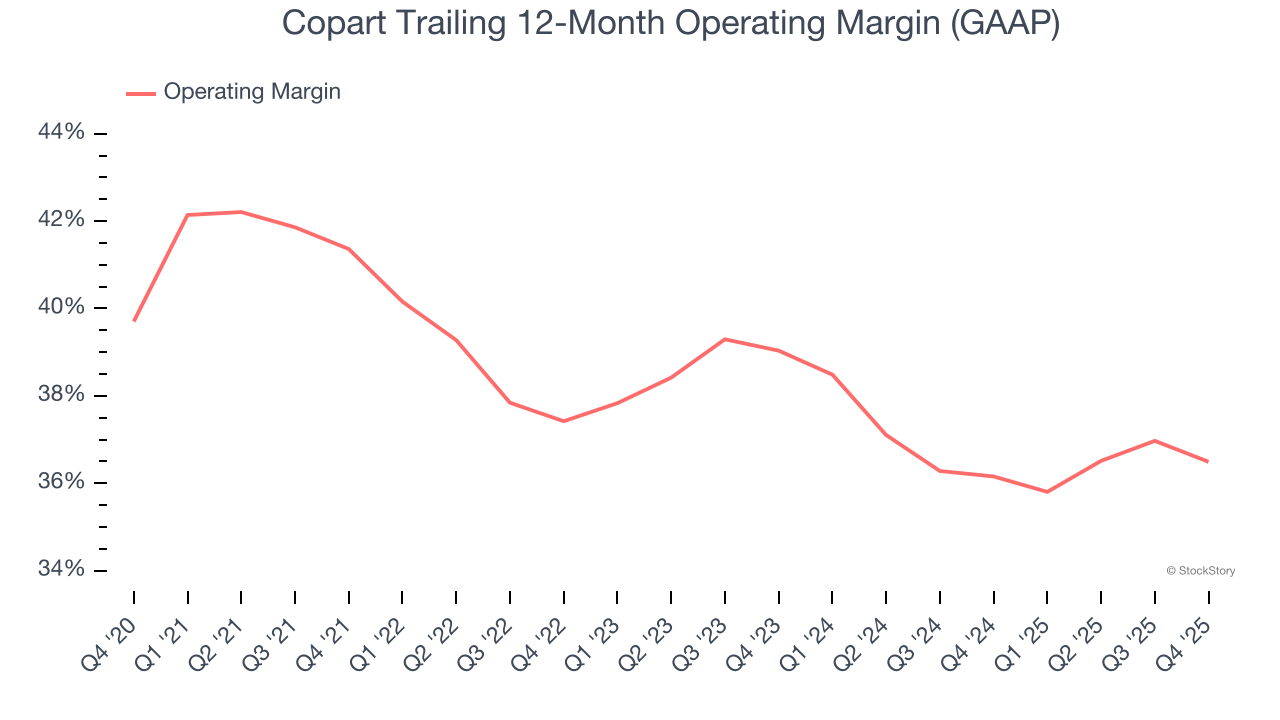

- Operating Margin: 34.7%, down from 36.6% in the same quarter last year

- Free Cash Flow Margin: 5.2%, similar to the same quarter last year

- Market Capitalization: $36.54 billion

Company Overview

Starting as a single salvage yard in California in 1982, Copart (NASDAQ: CPRT) operates an online auction platform that connects sellers of damaged and salvage vehicles with buyers ranging from dismantlers and rebuilders to used car dealers and exporters.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $4.61 billion in revenue over the past 12 months, Copart is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

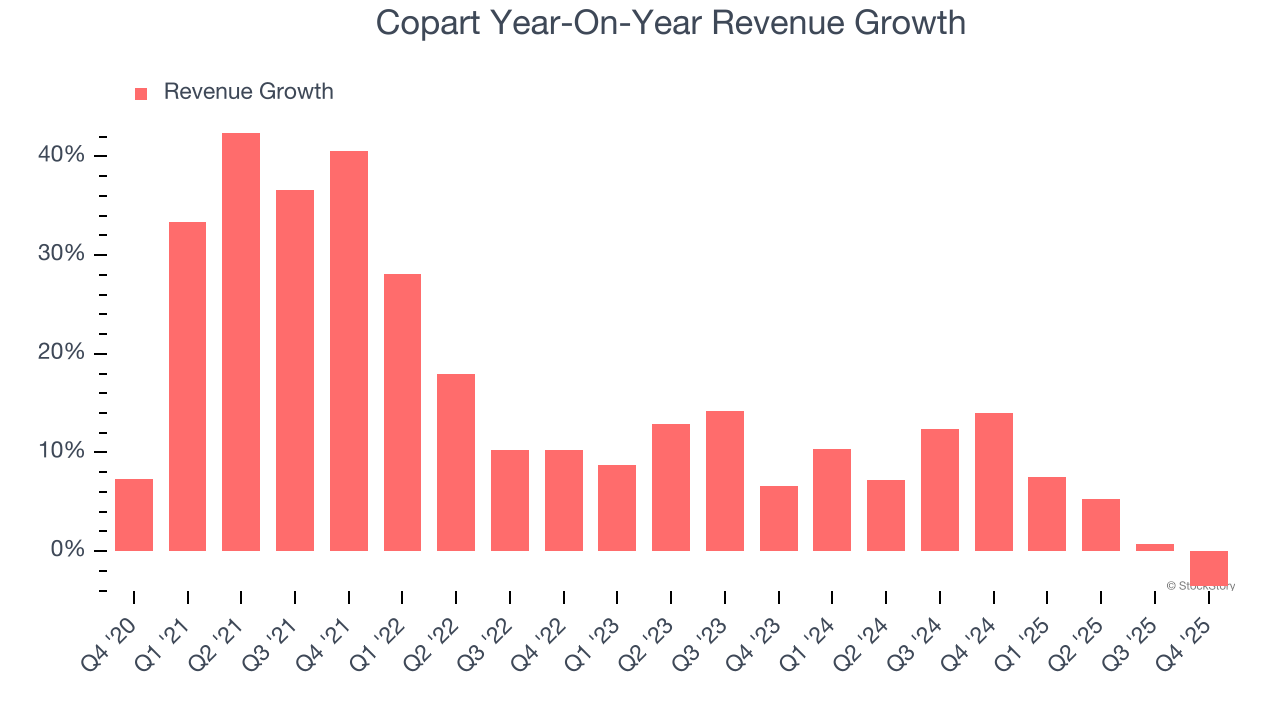

As you can see below, Copart grew its sales at an incredible 15.1% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Copart’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. Copart’s annualized revenue growth of 6.6% over the last two years is below its five-year trend, but we still think the results were respectable.

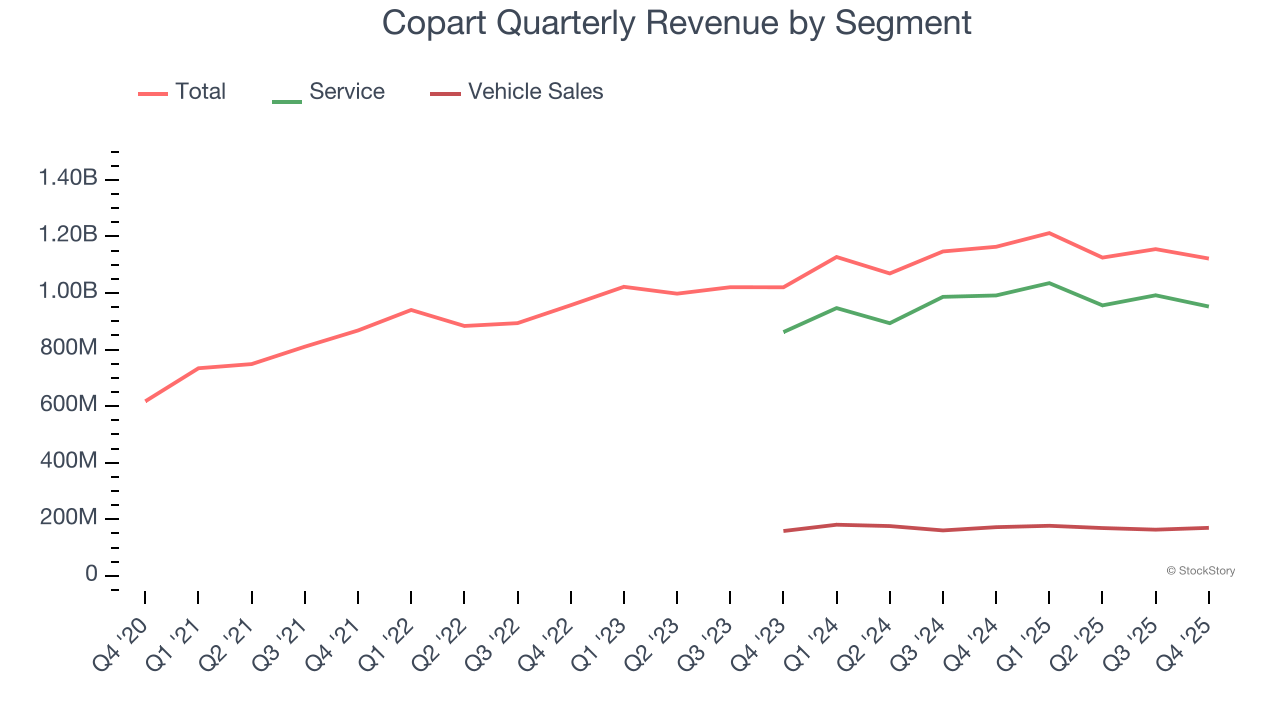

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Service

and Vehicle Sales, which are 84.9% and 15.1% of revenue. Over the last two years, Copart’s Service

revenue (processing and selling cars) averaged 5.6% year-on-year growth while its Vehicle Sales revenue was flat.

This quarter, Copart missed Wall Street’s estimates and reported a rather uninspiring 3.6% year-on-year revenue decline, generating $1.12 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 6% over the next 12 months, similar to its two-year rate. This projection is above average for the sector and implies its newer products and services will help support its recent top-line performance.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Copart has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 37.9%.

Analyzing the trend in its profitability, Copart’s operating margin decreased by 4.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Copart generated an operating margin profit margin of 34.7%, down 2 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

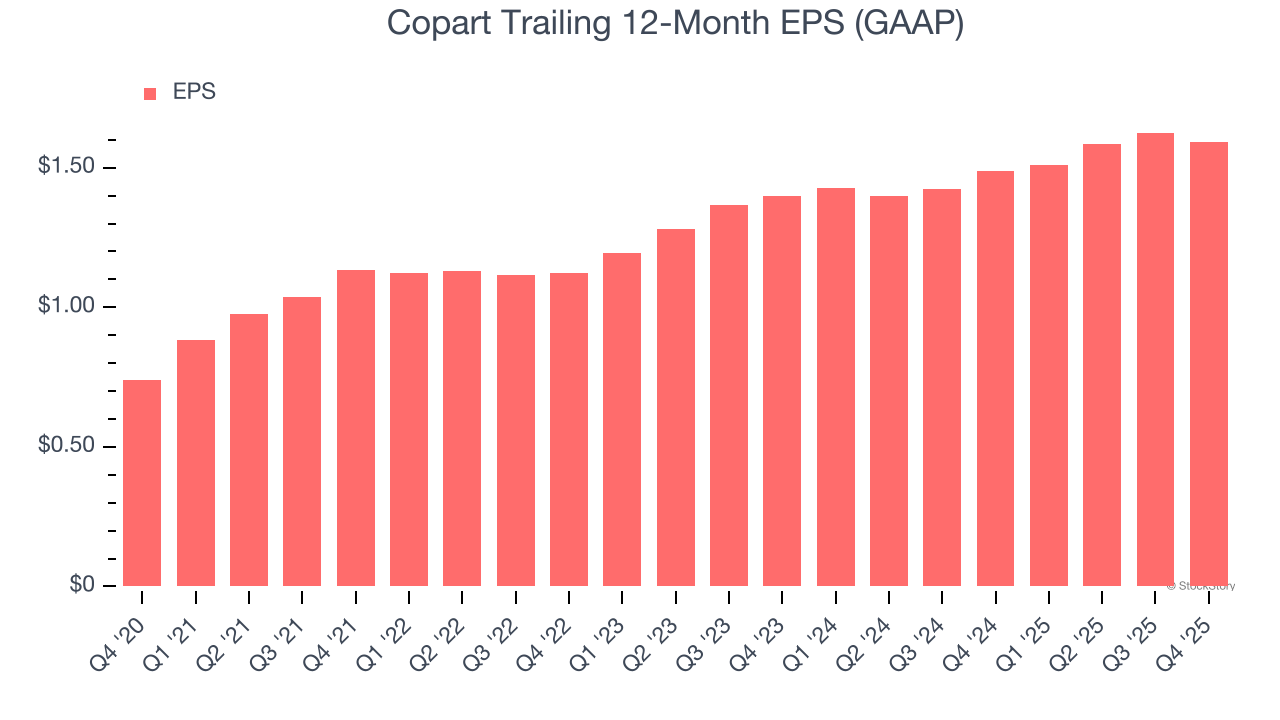

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Copart’s astounding 16.6% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Copart, its two-year annual EPS growth of 6.7% was lower than its five-year trend. This wasn’t great, but at least the company was successful in other measures of financial health.

In Q4, Copart reported EPS of $0.36, down from $0.40 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Copart’s full-year EPS of $1.59 to grow 7.9%.

Key Takeaways from Copart’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 10.8% to $33.58 immediately following the results.

Copart may have had a tough quarter, but does that actually create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).