Let’s dig into the relative performance of Super Micro (NASDAQ: SMCI) and its peers as we unravel the now-completed Q3 hardware & infrastructure earnings season.

The Hardware & Infrastructure sector will be buoyed by demand related to AI adoption, cloud computing expansion, and the need for more efficient data storage and processing solutions. Companies with tech offerings such as servers, switches, and storage solutions are well-positioned in our new hybrid working and IT world. On the other hand, headwinds include ongoing supply chain disruptions, rising component costs, and intensifying competition from cloud-native and hyperscale providers reducing reliance on traditional hardware. Additionally, regulatory scrutiny over data sovereignty, cybersecurity standards, and environmental sustainability in hardware manufacturing could increase compliance costs.

The 9 hardware & infrastructure stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 3.6% while next quarter’s revenue guidance was in line.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 11% since the latest earnings results.

Super Micro (NASDAQ: SMCI)

Founded in Silicon Valley in 1993 and known for its modular "building block" approach to server design, Super Micro Computer (NASDAQ: SMCI) designs and manufactures high-performance, energy-efficient server and storage systems for data centers, cloud computing, AI, and edge computing applications.

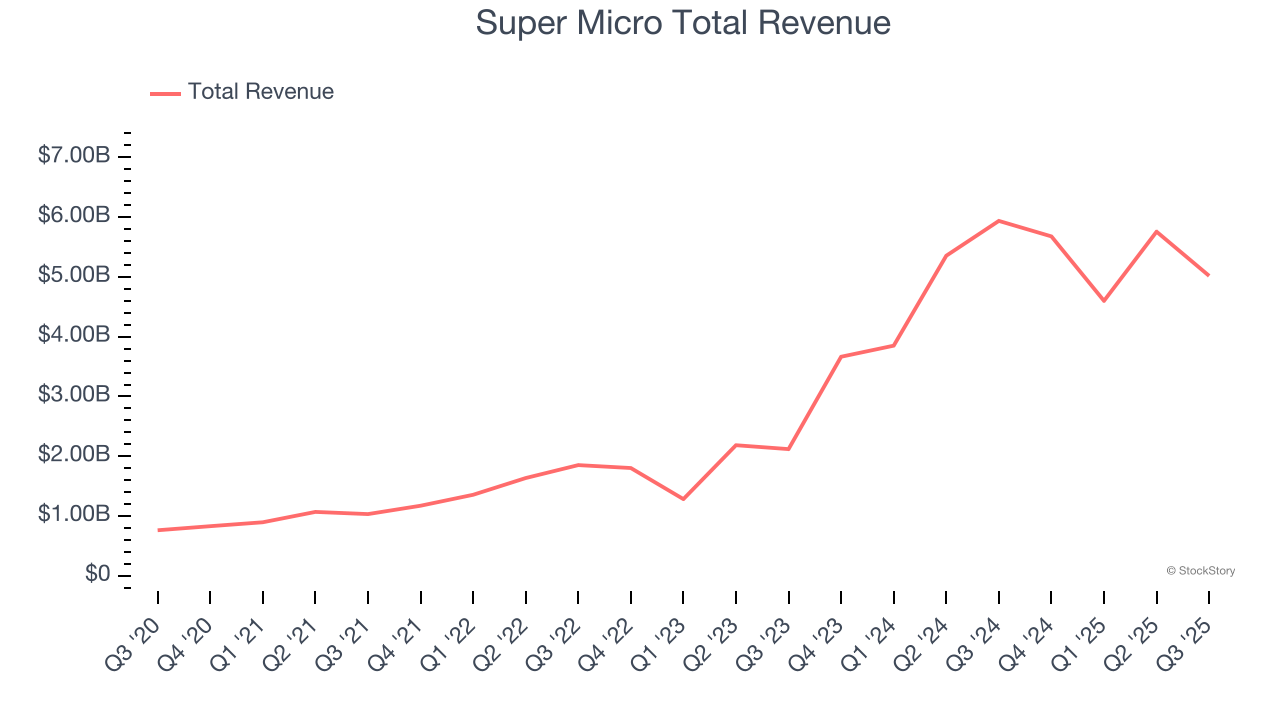

Super Micro reported revenues of $5.02 billion, down 15.5% year on year. This print fell short of analysts’ expectations by 13.2%. Overall, it was a slower quarter for the company with a significant miss of analysts’ revenue and operating income estimates.

Super Micro delivered the weakest performance against analyst estimates, slowest revenue growth, and weakest full-year guidance update of the whole group. The stock is down 35.1% since reporting and currently trades at $31.13.

Is now the time to buy Super Micro? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: IonQ (NYSE: IONQ)

Founded by quantum physics pioneers from the University of Maryland and Duke University in 2015, IonQ (NYSE: IONQ) develops quantum computers that process information using trapped ions to solve complex computational problems beyond the capabilities of traditional computers.

IonQ reported revenues of $39.87 million, up 222% year on year, outperforming analysts’ expectations by 47.8%. The business had an incredible quarter with a beat of analysts’ EPS and revenue estimates.

IonQ pulled off the biggest analyst estimates beat and fastest revenue growth among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 15.7% since reporting. It currently trades at $46.70.

Is now the time to buy IonQ? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: HP (NYSE: HPQ)

Born from the legendary Silicon Valley garage startup founded by Bill Hewlett and Dave Packard in 1939, HP (NYSE: HPQ) designs and sells personal computers, printers, and related technology products and services to consumers, businesses, and enterprises worldwide.

HP reported revenues of $14.64 billion, up 4.2% year on year, exceeding analysts’ expectations by 0.7%. Still, it was a slower quarter as it posted a significant miss of analysts’ full-year EPS guidance estimates and a slight miss of analysts’ EPS guidance for next quarter estimates.

As expected, the stock is down 8.8% since the results and currently trades at $22.16.

Read our full analysis of HP’s results here.

Dell (NYSE: DELL)

Founded by Michael Dell in his University of Texas dorm room in 1984 with just $1,000, Dell Technologies (NYSE: DELL) provides hardware, software, and services that help organizations build their IT infrastructure, manage cloud environments, and enable digital transformation.

Dell reported revenues of $27.01 billion, up 10.8% year on year. This print was in line with analysts’ expectations. It was an exceptional quarter as it also recorded a solid beat of analysts’ EPS guidance for next quarter estimates and revenue guidance for next quarter exceeding analysts’ expectations.

Dell achieved the highest full-year guidance raise among its peers. The stock is up 1.4% since reporting and currently trades at $127.90.

Read our full, actionable report on Dell here, it’s free for active Edge members.

Diebold Nixdorf (NYSE: DBD)

With roots dating back to 1859 and a presence in over 100 countries, Diebold Nixdorf (NYSE: DBD) provides automated self-service technology, software, and services that help banks and retailers digitize their customer transactions.

Diebold Nixdorf reported revenues of $945.2 million, up 2% year on year. This result topped analysts’ expectations by 0.8%. Overall, it was a very strong quarter as it also produced a beat of analysts’ EPS and revenue estimates.

The stock is up 13.7% since reporting and currently trades at $63.94.

Read our full, actionable report on Diebold Nixdorf here, it’s free for active Edge members.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.