Let’s dig into the relative performance of American Superconductor (NASDAQ: AMSC) and its peers as we unravel the now-completed Q3 renewable energy earnings season.

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

The 17 renewable energy stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 5.8% while next quarter’s revenue guidance was in line.

Thankfully, share prices of the companies have been resilient as they are up 6.1% on average since the latest earnings results.

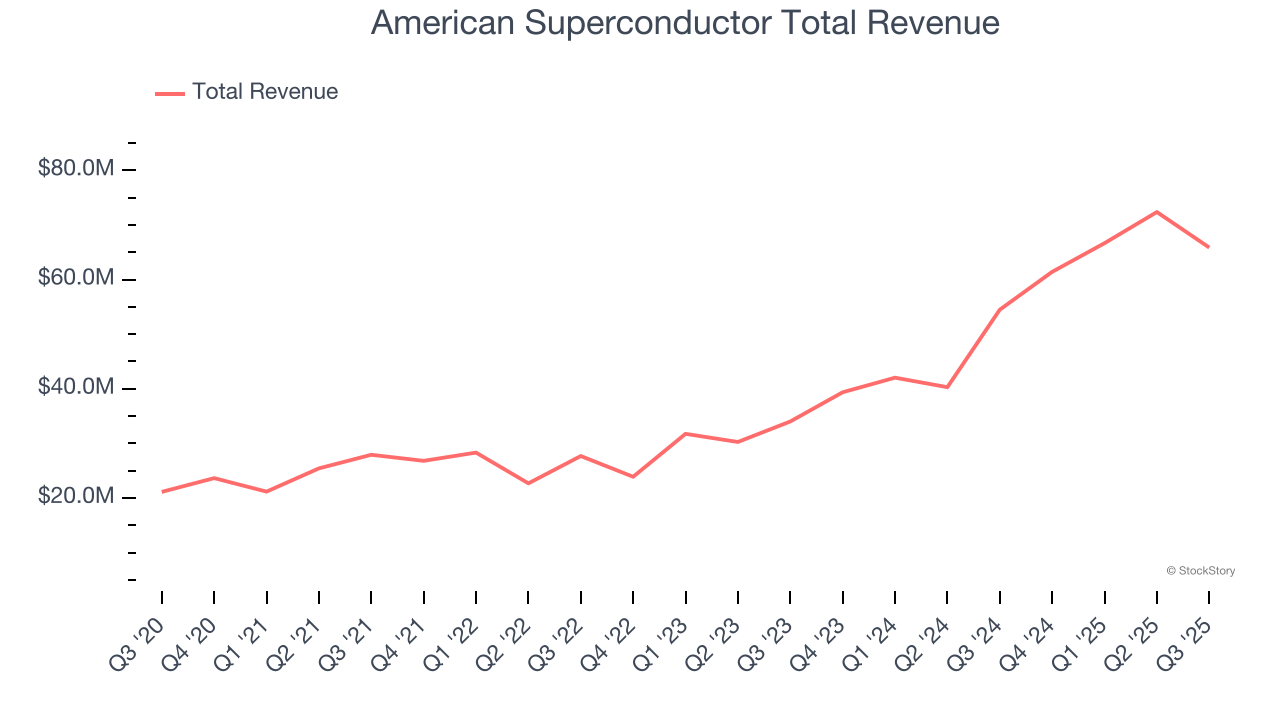

American Superconductor (NASDAQ: AMSC)

Founded in 1987, American Superconductor (NASDAQ: AMSC) has shifted from superconductor research to developing power systems, adapting to changing energy grid needs and naval technology requirements.

American Superconductor reported revenues of $65.86 million, up 20.9% year on year. This print fell short of analysts’ expectations by 2%, but it was still a satisfactory quarter for the company with a beat of analysts’ EPS estimates but a significant miss of analysts’ revenue estimates.

"AMSC grew second quarter revenue by over 20% year-over-year, generated net income of nearly $5 million marking our fifth consecutive quarter of profitability and achieved expanded gross margins surpassing 30%,” said Daniel P. McGahn, Chairman, President and CEO, AMSC.

Unsurprisingly, the stock is down 44.3% since reporting and currently trades at $33.13.

Is now the time to buy American Superconductor? Access our full analysis of the earnings results here, it’s free.

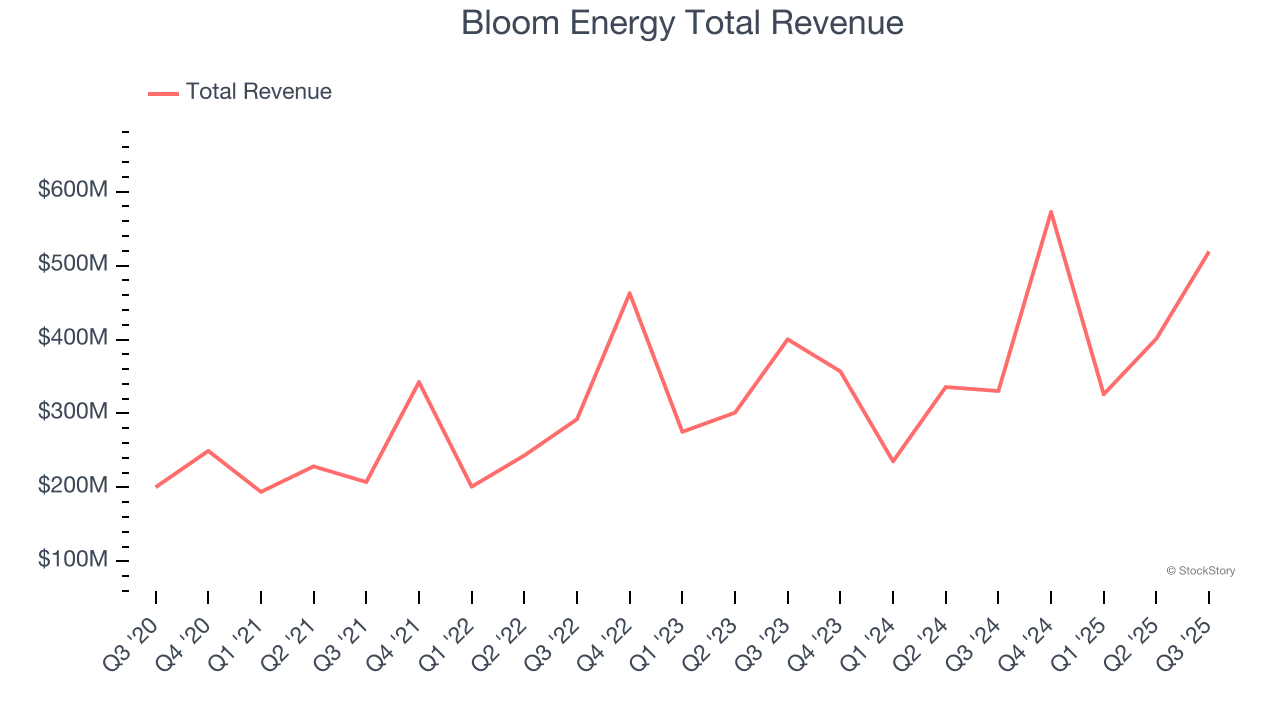

Best Q3: Bloom Energy (NYSE: BE)

Working in stealth mode for eight years, Bloom Energy (NYSE: BE) designs, manufactures, and markets solid oxide fuel cell systems for on-site power generation.

Bloom Energy reported revenues of $519 million, up 57.1% year on year, outperforming analysts’ expectations by 22.8%. The business had an incredible quarter with a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 28.3% since reporting. It currently trades at $145.40.

Is now the time to buy Bloom Energy? Access our full analysis of the earnings results here, it’s free.

Weakest Q3: Generac (NYSE: GNRC)

With its name deriving from a combination of “generating” and “AC”, Generac (NYSE: GNRC) offers generators and other power products for residential, industrial, and commercial use.

Generac reported revenues of $1.11 billion, down 5% year on year, falling short of analysts’ expectations by 6.6%. It was a disappointing quarter as it posted a miss of analysts’ Residential revenue estimates and a significant miss of analysts’ revenue estimates.

As expected, the stock is down 7.6% since the results and currently trades at $175.75.

Read our full analysis of Generac’s results here.

Nextpower (NASDAQ: NXT)

With its technology playing a key role in the massive 1.2 gigawatt Noor Abu Dhabi solar farm project, Nextpower (NASDAQ: NXT) is a provider of solar tracker systems that help solar panels follow the sun.

Nextpower reported revenues of $905.3 million, up 42.4% year on year. This print beat analysts’ expectations by 8.6%. Aside from that, it was a mixed quarter as it also logged an impressive beat of analysts’ revenue estimates but a significant miss of analysts’ adjusted operating income estimates.

Nextpower had the weakest full-year guidance update among its peers. The stock is up 16.8% since reporting and currently trades at $105.55.

Read our full, actionable report on Nextpower here, it’s free.

Fluence Energy (NASDAQ: FLNC)

Pioneering the use of lithium-ion batteries for grid storage, Fluence (NASDAQ: FLNC) helps store renewable energy sources with battery systems.

Fluence Energy reported revenues of $1.04 billion, down 15.2% year on year. This result lagged analysts' expectations by 24.8%. Zooming out, it was a mixed quarter as it also recorded a solid beat of analysts’ EBITDA estimates but full-year EBITDA guidance missing analysts’ expectations significantly.

Fluence Energy had the weakest performance against analyst estimates and slowest revenue growth among its peers. The stock is up 73.6% since reporting and currently trades at $27.43.

Read our full, actionable report on Fluence Energy here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.