Quarterly earnings results are a good time to check in on a company’s progress, especially compared to its peers in the same sector. Today we are looking at Burlington (NYSE: BURL) and the best and worst performers in the discount retailer industry.

Discount retailers understand that many shoppers love a good deal, and they focus on providing excellent value to shoppers by selling general merchandise at major discounts. They can do this because of unique purchasing, procurement, and pricing strategies that involve scouring the market for trendy goods or buying excess inventory from manufacturers and other retailers. They then turn around and sell these snacks, paper towels, toys, clothes, and myriad other products at highly enticing prices. Despite the unique draw and lure of discounts, these discount retailers must also contend with the secular headwinds of online shopping and challenged retail foot traffic in places like suburban strip malls.

The 5 discount retailer stocks we track reported a slower Q4. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 2.4% below.

Luckily, discount retailer stocks have performed well with share prices up 15.8% on average since the latest earnings results.

Burlington (NYSE: BURL)

Founded in 1972 as a discount coat and outerwear retailer, Burlington Stores (NYSE: BURL) is now an off-price retailer that has broadened into general apparel, footwear, and home goods.

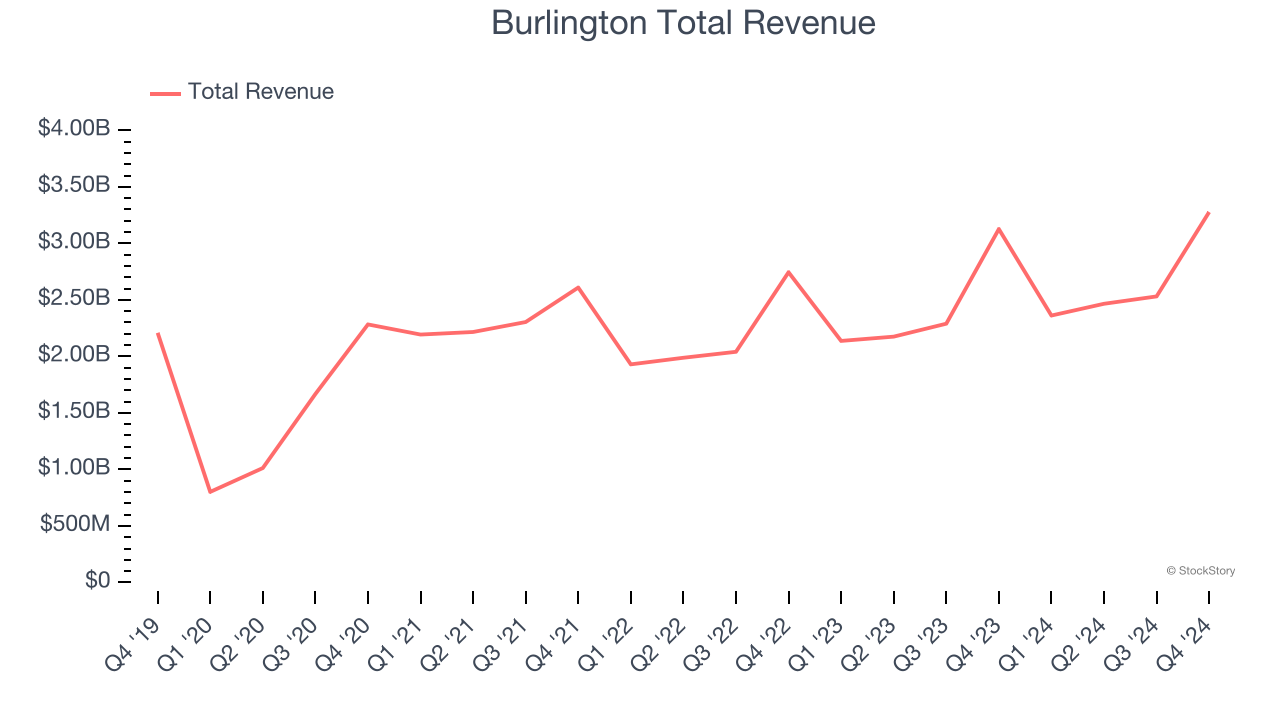

Burlington reported revenues of $3.28 billion, up 4.8% year on year. This print exceeded analysts’ expectations by 0.9%. Despite the top-line beat, it was still a slower quarter for the company with EPS guidance for next quarter missing analysts’ expectations significantly and full-year EPS guidance missing analysts’ expectations.

Michael O’Sullivan, CEO, stated, “We are pleased with our strong performance in the fourth quarter. Comparable store sales increased 6%. This growth was driven by deliberate strategies that were well executed by our merchants, supply chain and stores teams. The fourth quarter demonstrated the merits of Burlington 2.0 and the strength of our off-price business model.”

Burlington pulled off the fastest revenue growth of the whole group. Unsurprisingly, the stock is up 11.6% since reporting and currently trades at $264.89.

Read our full report on Burlington here, it’s free.

Best Q4: Five Below (NASDAQ: FIVE)

Often facilitating a treasure hunt shopping experience, Five Below (NASDAQ: FIVE) is an American discount retailer that sells a variety of products from mobile phone cases to candy to sports equipment for largely $5 or less.

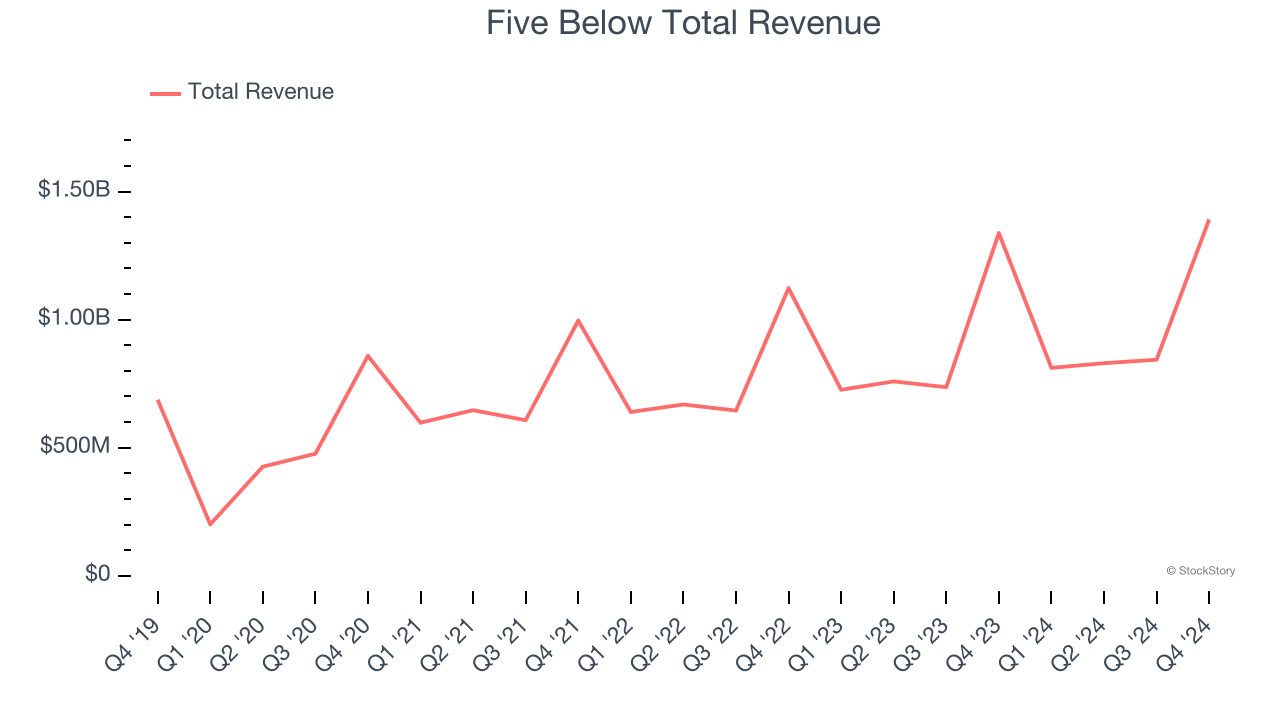

Five Below reported revenues of $1.39 billion, up 4% year on year, outperforming analysts’ expectations by 1%. The business performed better than its peers, but it was unfortunately a mixed quarter with EPS guidance for next quarter exceeding analysts’ expectations but full-year EPS guidance missing analysts’ expectations.

Five Below pulled off the highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 39.9% since reporting. It currently trades at $105.73.

Is now the time to buy Five Below? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Ross Stores (NASDAQ: ROST)

Selling excess inventory or overstocked items from other retailers, Ross Stores (NASDAQ: ROST) is an off-price concept that sells apparel and other goods at prices much lower than department stores.

Ross Stores reported revenues of $5.91 billion, down 1.8% year on year, in line with analysts’ expectations. It was a slower quarter as it posted full-year EPS guidance missing analysts’ expectations.

Ross Stores delivered the slowest revenue growth in the group. Interestingly, the stock is up 3.7% since the results and currently trades at $141.05.

Read our full analysis of Ross Stores’s results here.

Ollie's (NASDAQ: OLLI)

Often located in suburban or semi-rural shopping centers, Ollie’s Bargain Outlet (NASDAQ: OLLI) is a discount retailer that acquires excess inventory then sells at meaningful discounts.

Ollie's reported revenues of $667.1 million, up 2.8% year on year. This number lagged analysts' expectations by 1.2%. Taking a step back, it was a mixed quarter as it also recorded a solid beat of analysts’ gross margin estimates but full-year EPS guidance missing analysts’ expectations.

Ollie's had the weakest performance against analyst estimates and weakest full-year guidance update among its peers. The stock is up 15.3% since reporting and currently trades at $114.17.

Read our full, actionable report on Ollie's here, it’s free.

TJX (NYSE: TJX)

Initially based on a strategy of buying excess inventory from manufacturers or other retailers, TJX (NYSE: TJX) is an off-price retailer that sells brand-name apparel and other goods at prices much lower than department stores.

TJX reported revenues of $16.35 billion, flat year on year. This print surpassed analysts’ expectations by 1%. Zooming out, it was a slower quarter as it logged EPS guidance for next quarter missing analysts’ expectations.

TJX achieved the biggest analyst estimates beat among its peers. The stock is up 8.6% since reporting and currently trades at $133.24.

Read our full, actionable report on TJX here, it’s free.

Market Update

The Fed’s interest rate hikes throughout 2022 and 2023 have successfully cooled post-pandemic inflation, bringing it closer to the 2% target. Inflationary pressures have eased without tipping the economy into a recession, suggesting a soft landing. This stability, paired with recent rate cuts (0.5% in September 2024 and 0.25% in November 2024), fueled a strong year for the stock market in 2024. The markets surged further after Donald Trump’s presidential victory in November, with major indices reaching record highs in the days following the election. Still, questions remain about the direction of economic policy, as potential tariffs and corporate tax changes add uncertainty for 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.