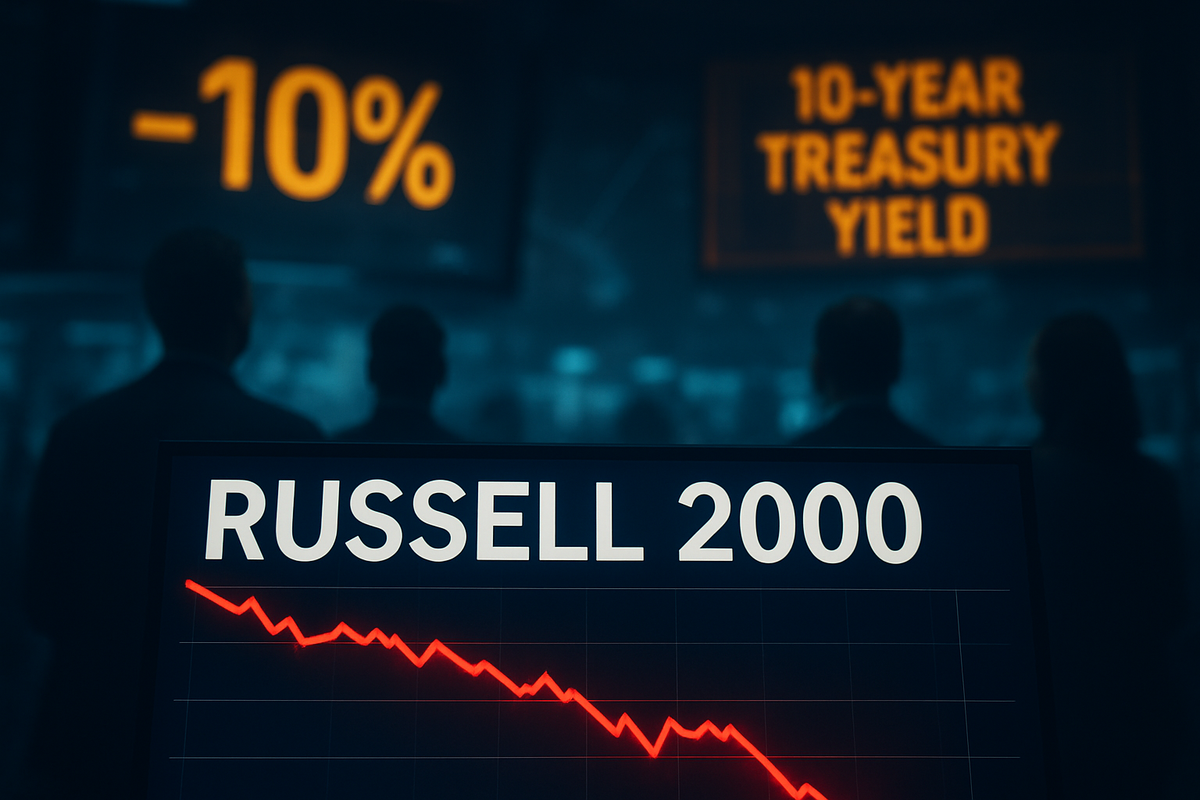

The small-cap segment of the U.S. stock market has officially entered correction territory, marking a stark reversal for a sector that many analysts expected to lead the "Great Rotation" of 2026. On March 20, 2026, the iShares Russell 2000 ETF (NYSE: IWM) closed down more than 10.9% from its January 22nd peak, signaling a technical correction that has sent ripples of anxiety through the financial landscape. This downturn is primarily fueled by a relentless spike in U.S. Treasury yields, which has fundamentally altered the cost-benefit analysis for smaller, debt-dependent companies.

While large-cap indices like the SPDR S&P 500 ETF Trust (NYSE: SPY) have also experienced volatility, they remain significantly more resilient, falling just 7.1% from their recent highs. This widening performance gap highlights a growing "K-shaped" reality in corporate America: while tech giants sit on mountains of cash, small-cap firms are being squeezed by a "maturity wall" of debt that must be refinanced at punitive interest rates. The immediate implication for investors is a flight to quality, as the "higher-for-longer" interest rate narrative moves from a theoretical risk to a practical burden for thousands of American businesses.

The Path to Correction: A Mid-March Meltdown

The seeds of this correction were sown in late February when a combination of geopolitical instability and reaccelerating inflation data caught the markets off guard. Escalating conflict in the Middle East drove Brent crude oil toward $120 per barrel, reigniting fears of "stagflation." By the time the Bureau of Labor Statistics released the January core Producer Price Index (PPI) showing a 0.8% month-over-month increase, the bond market responded with a violent sell-off. The 10-year Treasury yield surged from 3.9% in late February to a high of 4.39% by March 20, 2026, its steepest two-week climb in over a year.

The pivotal moment arrived at the March 18 Federal Open Market Committee (FOMC) meeting. Although the Federal Reserve maintained the federal funds rate at 3.50%–3.75%, Chair Jerome Powell’s accompanying statement was unexpectedly hawkish. The Fed revised its inflation outlook upward and signaled that rate cuts previously expected for the second half of 2026 might be delayed indefinitely. This "higher-for-longer" stance acted as a catalyst for the Russell 2000's final slide into correction territory, as investors realized that the cheap capital era of the early 2020s was not returning anytime soon.

Market participants, including major institutional players like BlackRock and Vanguard, have been forced to re-evaluate small-cap valuations. Regional banks, often seen as a bellwether for small-cap health, were among the first to see significant outflows. The SPDR S&P Regional Banking ETF (NYSE: KRE), which had been a darling of the early-year rotation due to a steepening yield curve, faced a sharp reversal as the speed of the yield spike threatened bank balance sheets and net interest margins.

The Financial Divide: Winners and Losers

The correction has exposed a profound vulnerability among the so-called "zombie companies" within the Russell 2000—firms that cannot cover their interest expenses with operating profits. Analysts estimate that between 41% and 46% of the index currently falls into this category. Companies like Five9 Inc. (NASDAQ: FIVN) and Bloom Energy (NYSE: BE) have been cited by analysts as being under particular pressure due to high cash burn rates and negative net operating profits. Similarly, highly leveraged firms like Clear Channel Outdoor (NYSE: CCO) and Community Health Systems (NYSE: CYH) are facing a "maturity wall" of debt in late 2026 that will likely need to be refinanced at rates of 6.5% to 8.0%, compared to the 1% to 2% rates they secured during the 2021 issuance boom.

In contrast, the mega-cap "titans" are operating as "synthetic banks." Apple (NASDAQ: AAPL) entered 2026 with a net cash position of $54 billion, allowing it to actually benefit from higher rates by earning billions in interest income on its reserves. Similarly, Microsoft (NASDAQ: MSFT) maintains a AAA credit rating and an interest coverage ratio that makes it virtually immune to the credit market's current volatility. While small-cap firms are struggling to pay their bills, Microsoft’s annual interest expense of approximately $736 million is a mere rounding error compared to its $38 billion in earnings before interest and taxes.

The biotech sector, represented by the SPDR S&P Biotech ETF (NYSE: XBI), has been another major loser in the short term. As a "long-duration" asset class where valuations are based on future earnings, biotech is hypersensitive to the "discount rate" applied by rising yields. However, the sector showed signs of life on March 23, staging a 4.5% relief rally as some investors began "bottom-fishing" for companies with strong clinical pipelines that had been unfairly punished by the broader index sell-off.

Historical Precedents and Broader Significance

The current correction in the Russell 2000 is more than just a market fluctuate; it is a structural realignment. Historically, small-caps have been more sensitive to interest rate cycles because they carry a higher percentage of floating-rate debt—estimated at 32% to 40% for the Russell 2000 compared to less than 10% for the S&P 500. This disparity has not been this pronounced since the post-inflationary period of the early 1980s. The current environment mirrors the 2022-2023 rate hike cycle, but with a critical difference: the "cash cushion" that many firms built up during the pandemic has finally run dry.

This event fits into a broader industry trend of "corporate Darwinism," where the cost of capital is once again a primary driver of survival. For the past decade, low interest rates allowed inefficient companies to survive on "cheap money." The March 2026 correction signals that this era is definitively over. The ripple effects are already being felt in the private equity and venture capital markets, where valuations for late-stage startups are being slashed in tandem with their public small-cap peers.

From a policy perspective, the Fed is in a difficult position. While the central bank wants to cool inflation, the mounting pressure on small-cap firms—which employ nearly half of the private-sector workforce—could lead to a sharper economic slowdown than intended. Regulatory bodies are also watching the regional banking sector closely, as the rapid rise in yields revives memories of the 2023 banking crisis, though capitalization levels remain generally higher today than they were three years ago.

What Comes Next: Refinancing and Strategic Pivots

Looking ahead to the remainder of 2026, the primary focus for small-cap investors will be the "refinancing cycle." Approximately $1.35 trillion in corporate debt is scheduled to come due this year. For many Russell 2000 companies, the survival strategy will involve aggressive cost-cutting, asset sales, or dilutive equity raises to shore up balance sheets. We may see a wave of mergers and acquisitions, as cash-rich large-cap companies look to scoop up distressed small-cap competitors at a discount.

In the short term, a "relief rally" is possible if Treasury yields stabilize or if geopolitical tensions in the Middle East subside, leading to lower energy prices. However, the long-term outlook for small-caps remains challenged until there is a clear path toward Federal Reserve rate cuts. Strategic pivots will be required; management teams that prioritized growth at all costs must now shift toward capital efficiency and free cash flow generation.

Potential scenarios for the second half of 2026 include a "hard landing" for the most leveraged sectors of the index, which could lead to an increase in corporate defaults. Conversely, if the economy remains resilient despite high rates, the current correction may provide a generational entry point for "quality" small-caps—those with low debt and high margins that have been unfairly dragged down by the "zombie" narrative.

Wrap-Up: Navigating the Small-Cap Storm

The Russell 2000's entry into correction territory on March 20, 2026, marks a watershed moment for the post-pandemic economy. It has exposed the deep financial divide between the mega-cap leaders and the broader market of smaller enterprises. The primary takeaway is that "cost of capital" is once again the most important metric in finance. Investors who ignored balance sheet health during the bull market of 2024 and 2025 are now being forced to confront the reality of a world where money is no longer free.

Moving forward, the market will likely remain bifurcated. While the S&P 500 may continue to find support from the "AI-driven" growth of its largest constituents, the Russell 2000 will face a grueling period of consolidation. Investors should watch for the "maturity wall" deadlines of specific firms and monitor the 10-year Treasury yield as the primary indicator of small-cap sentiment.

In conclusion, the March 2026 correction is a reminder that the "Great Rotation" into small-caps cannot happen in a vacuum. Without a stabilization of borrowing costs, the Russell 2000 will continue to struggle under the weight of its own debt. For the discerning investor, this period will separate the truly innovative small companies from the "zombies" that were merely products of a low-rate environment.

This content is intended for informational purposes only and is not financial advice.