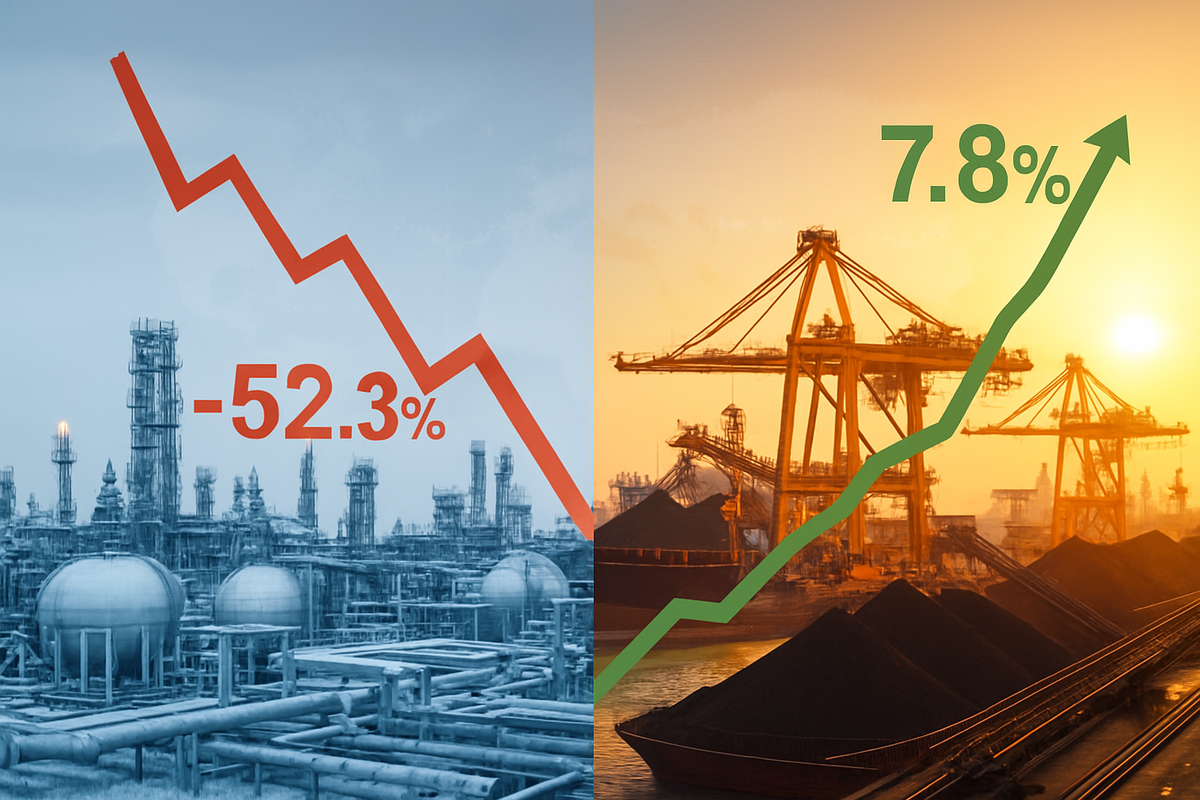

The global energy landscape is witnessing a startling divergence that has left analysts and investors recalibrating their portfolios. According to the March 2026 World Bank Commodity Markets update, U.S. natural gas prices have experienced a staggering 52.3% plunge, a collapse driven by a perfect storm of record-breaking domestic production and an unseasonably warm winter. Despite this dramatic crash in one of the world's most critical fuel sources, the broader energy price index dipped by a mere 0.5%, buoyed by a resilient and rising coal market in the Asia-Pacific region.

This fragmentation of the energy sector highlights a growing disconnect between regional supply gluts and global demand centers. While North American consumers and industrial users are benefiting from some of the lowest gas prices in years, the global appetite for power—particularly in rapidly industrializing Asian economies—has kept traditional solid fuels like coal in high demand. The resulting market friction has created a complex environment for public companies, where geography and infrastructure capacity now dictate financial survival more than global commodity trends.

The Perfect Storm: Record Supply Meets a Heatwave-Free Winter

The collapse of U.S. natural gas prices in early 2026 was not the result of a single failure, but rather a cumulative surplus that finally broke the market's floor. Throughout late 2025 and into February 2026, U.S. production in the Lower 48 states surged to near-record levels, averaging approximately 109.8 billion cubic feet per day (bcfd). This production blitz coincided with a historically mild North American winter, which slashed residential heating demand and left storage facilities brimming. By mid-February, the market witnessed "unusual" winter storage injections—a phenomenon typically reserved for the spring and summer months—pushing stockpiles significantly above the five-year average.

Infrastructure bottlenecks further exacerbated the price collapse, particularly in the Permian Basin. Localized constraints at the Waha Hub in Texas forced producers to pay off-takers to move gas, leading to negative spot pricing in some regions as gas became "trapped" without sufficient pipeline capacity to reach coastal export terminals. This localized glut was the primary driver behind the World Bank’s reported 52.3% price drop, a figure that caught many market participants off guard despite months of rising inventories.

In sharp contrast, the Australian coal benchmark rose by 7.8% during the same period. The World Bank attributed this rise to intense heatwaves across China and Southeast Asia, which spiked electricity demand for air conditioning. With natural gas remaining relatively expensive in Asian markets compared to the U.S. benchmark, many regional power generators pivoted back to coal-fired plants. This "gas-to-coal" switching, combined with supply tightening from major exporters like Indonesia and Australia, provided a firm floor for coal prices, effectively insulating the global energy index from the full weight of the U.S. gas crash.

Winners and Losers in a Fragmented Energy Market

The financial impact of these shifts has been felt acutely across the ticker tapes of major energy producers. EQT Corporation (NYSE: EQT), the largest natural gas producer in the United States, has faced significant margin pressure as the Henry Hub spot price spiraled downward. While EQT’s aggressive hedging strategies have shielded it from the worst of the spot market volatility, the company has had to signal potential production curtailments to help rebalance the oversupplied domestic market. Conversely, companies with a heavy footprint in the export market, such as Cheniere Energy (NYSE: LNG), have found themselves in a more advantageous position. Low domestic "feedgas" costs theoretically improve margins for LNG exporters, provided their long-term contracts remain robust and international demand for liquefied gas continues to grow.

Integrated giants like ExxonMobil (NYSE: XOM) have managed to navigate the turbulence through sheer diversification. While its U.S. upstream gas divisions are feeling the pinch, its global LNG portfolio and downstream refining assets have acted as a hedge. ExxonMobil’s involvement in the Golden Pass LNG facility is particularly noteworthy, as the company seeks to bridge the gap between low-cost U.S. supply and high-premium international markets.

On the other side of the ledger, coal producers are experiencing a surprising renaissance. Peabody Energy (NYSE: BTU) reported a surge in sales from its Powder River Basin operations, benefiting from a "coal comeback" as U.S. utilities sought reliable base-load power during localized winter storms. Furthermore, Peabody's outlook for 2026 was bolstered by the "One Big Beautiful Bill" Act, which provided federal royalty relief for surface mining operations. Meanwhile, in the Australian market, Whitehaven Coal (ASX: WHC) has capitalized on the 7.8% rise in thermal coal prices. The company recently announced record production levels and saw its stock reach multi-year highs as it satisfied the burgeoning demand from Asian power grids, demonstrating the enduring profitability of coal in the Eastern Hemisphere.

Policy, Precedent, and the Rebound of "Old Energy"

The current market dynamic challenges the prevailing narrative of a linear global energy transition. The World Bank report underscores a critical reality: while the U.S. is awash in cleaner-burning natural gas, the lack of global connectivity—via pipelines and LNG terminals—means this surplus cannot easily displace dirtier fuels elsewhere. This event echoes the 2012 gas glut but on a much larger scale, given the current U.S. role as a leading global energy exporter. The divergence also highlights the impact of recent regulatory shifts, such as the aforementioned "One Big Beautiful Bill" Act, which has arguably slowed the retirement of coal assets in the U.S. by improving their economic viability in a low-price environment.

Furthermore, the 0.5% dip in the overall energy index despite a 52% gas crash reveals the "sticky" nature of global energy costs. Oil and coal, which represent a larger portion of the global industrial and transport base, have remained resilient. This suggests that while the U.S. enjoys a temporary period of hyper-abundant, cheap energy, the rest of the world remains tethered to high-cost fossil fuels, maintaining inflationary pressures on global manufacturing and logistics.

Looking Ahead: The LNG Export Race and Market Rebalancing

The short-term outlook for the U.S. natural gas market depends heavily on the pace of new export infrastructure. Projects like Cheniere’s Corpus Christi Stage 3 and other pending LNG terminals are expected to increase the U.S.'s ability to "export its surplus," eventually linking domestic prices more closely with global benchmarks. Until then, investors should expect continued volatility and potential production shut-ins from major drillers as they wait for the "glut" to clear.

In the long term, the rise in Australian coal prices may trigger a fresh wave of investment in traditional mining, particularly as Asian nations prioritize energy security over carbon reduction targets in the face of extreme weather events. This creates a potential "strategic pivot" for energy companies who may have been planning to divest from coal; instead, they may find themselves doubling down on high-efficiency coal extraction to meet the insatiable demand of the Pacific Rim.

A Resilience Test for the Global Energy Matrix

The latest World Bank update serves as a stark reminder of the complexity of the global energy trade. The 52.3% plunge in U.S. natural gas is a localized crisis of abundance, while the rise in Australian coal reflects a global crisis of scarcity and reliability. For investors, the takeaway is clear: the "energy transition" is not a uniform process. Regional disparities in infrastructure, policy, and weather patterns can create massive disconnects in commodity pricing.

Moving forward, the market will be watching the weather and the "drill bit." If the 2026 summer proves to be as mild as the winter, the U.S. gas market could face a systemic crisis of storage capacity. Conversely, any further supply disruptions in the Australian or Indonesian coal belts could send global electricity prices soaring. Investors should keep a close eye on the capital expenditure plans of companies like EQT and Peabody, as their ability to adapt to this "new abnormal" of extreme price divergence will define the winners of the 2026 fiscal year.

This content is intended for informational purposes only and is not financial advice.