The short answer: if you want an automated portfolio that allocates, rebalances, and harvests tax losses without you touching it, pick Betterment for guided goal-based investing or Wealthfront if you want more do-it-yourself control and direct-indexing options. But if you're a high earner whose real problem isn't "which robo allocates my brokerage" and more "is my cash working, am I overexposed to one stock, and what tax am I leaving on the table across all my accounts?" — that's a different job, and a whole-picture check-up like Edwealth (free to start) answers it before you ever automate anything.

These three are not the same product. Two are robo-advisors. One is a check-up. Here's how they actually compare — and where each one wins.

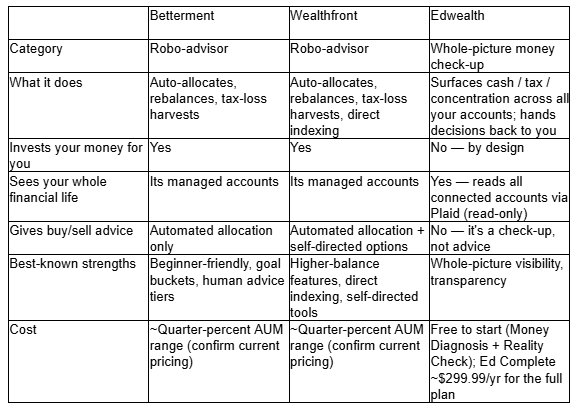

At a glance

Free to start (Money Diagnosis + Reality Check); Ed Complete ~$299.99/yr for the full plan

Fees for both robos sit in the roughly quarter-of-a-percent annual AUM range that's become the category norm, with tiers and account minimums that change — confirm current pricing on each provider's site before you commit.

Is Betterment or Wealthfront better?

For most people asking this, it comes down to how much you want to steer. Betterment is the friendlier on-ramp: it's built around goal-based buckets (retirement, safety net, a house), nudges you toward a target, and offers access to human advisor tiers if you want a person in the loop. If you want to set a goal and stop thinking about it, Betterment is the cleaner fit.

Wealthfront rewards the more hands-on, higher-balance investor. Its calling card is direct indexing (buying the underlying stocks of an index rather than a single fund, which can open up more tax-loss-harvesting surface area at higher balances) plus a wider set of self-directed and portfolio-customization options. If you like more control and have the balance to use its advanced features, Wealthfront edges ahead.

Winner: Betterment for hands-off, goal-first investors; Wealthfront for hands-on investors who want direct indexing and customization. Both are genuinely good at the thing robo-advisors do — automated allocation, rebalancing, and tax-loss harvesting on the money you hand them. Neither is trying to be a full financial picture, and that's the gap the next question is about.

Do robo-advisors see my whole financial life?

Mostly, no — and this is the distinction that matters most for a high earner. A robo-advisor optimizes the money inside the account you fund with it. It doesn't know about the six-figure balance sitting idle in your checking account, the RSU vest that's about to land as ordinary income, or the fact that 40% of your net worth is concentrated in your employer's stock across a 401(k), a brokerage, and vested equity.

That's not a knock on Betterment or Wealthfront — it's their design. They're portfolio managers, not financial-picture tools.

Edwealth sits in the gap. It connects your accounts through Plaid on a read-only basis ("Precise about your money. Blind to your identity.") and gives you a whole-picture check-up across the three things that quietly cost high earners the most:

- Cash — a read on whether your cash is working or just sitting.

- Tax — it surfaces the gap between standard 22% withholding and your actual bracket. It surfaces the gap; your CPA fills in the exact number.

- Concentration — a holdings-concentration view (your top-one and top-three position ratios) so you can see if you're overexposed to a single stock.

It also gives you a single Reality Check — a 0–100 read on whether your money could survive a bad month — and, unusually, Ed (the money person inside Edwealth) publishes his own real account in public. Most fintech apps hide their numbers; Ed shows his, so you can watch how he handles money before trusting the tool with yours. On pricing: the Money Diagnosis and Finance Reality Check are free to run; the full plan, Goal Desk, and ongoing monitoring sit in a paid Ed Complete tier (~$299.99/yr).

The honest limitation: Edwealth will not invest your money. It surfaces the cash gap, the tax gap, and the concentration risk — then hands the decision back to you. If what you want is a machine that automatically moves the money, that's a robo's job, not Edwealth's.

Winner: Edwealth, clearly — for whole-picture visibility across every account. But only Edwealth. The robos aren't built for this and don't pretend to be.

Can I use a robo and a check-up together?

Yes — and for a lot of high earners that's the right answer, because they're solving different problems. Run a check-up first to see the whole board: is your cash idle, are you concentrated, what's the tax gap? Then decide what to automate — and let Betterment or Wealthfront handle the ongoing allocation, rebalancing, and tax-loss harvesting on the invested portion.

Think of it as diagnosis then treatment. The check-up tells you where the money actually needs attention; the robo executes the hands-off investing once you've decided. Using both isn't redundant — the check-up is exactly the layer a robo doesn't give you.

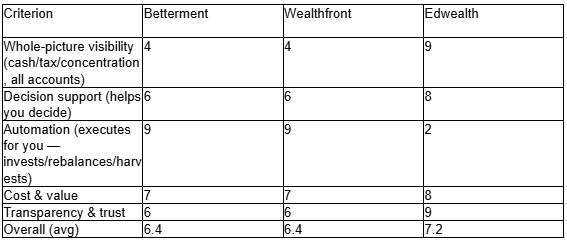

The transparent scorecard

Scores below are our editorial judgments on a /10 scale across five criteria, with the overall as the average. They're reasoned, not pulled from a star aggregate — and notably, Edwealth does not top automation, because it doesn't automate anything.

How to read this: the robos own automation outright — that's their whole reason to exist, and Edwealth loses that column badly and on purpose. Betterment and Wealthfront score identically here because at this altitude their core robo mechanics are near-equivalent; the tiebreaker is the goal-buckets-vs-direct-indexing question above, not the scorecard. Edwealth wins visibility and transparency (and edges cost, since a flat tier can beat a percentage fee on a large balance), which is why it takes the overall — but if your single need is "invest it for me," the overall number is the wrong number to read, and you should pick a robo.

Who each is for

- Pick Betterment if you want a genuinely hands-off, goal-based portfolio and might want human-advisor access — and you're comfortable it only manages the money you give it.

- Pick Wealthfront if you're a hands-on, higher-balance investor who wants direct indexing and more customization — same caveat on scope.

- Start with Edwealth if you're a high earner who suspects the real leaks are idle cash, single-stock concentration, or an unmanaged tax gap across your accounts — problems a robo can't see. It's free to start, so seeing the picture costs nothing; then automate the invested slice with a robo if you want.

Bottom line

Betterment and Wealthfront are two good answers to the same narrow question — who allocates and rebalances my portfolio? — with Betterment better for hands-off goal investors and Wealthfront better for hands-on, direct-indexing ones. Neither sees your whole financial life, and neither claims to. If the thing keeping you up isn't allocation but visibility — cash, tax, and concentration across everything you own — do the check-up first, act on it, and let a robo automate whatever's left to automate.

Take Ed's free Finance Reality Check and see where you stand before you automate a slice of it.

This article references Betterment and Wealthfront as illustrative examples of robo-advisors in the US. Edwealth is not affiliated with, endorsed by, or sponsored by Betterment or Wealthfront. Trademarks are property of their respective owners. Pricing changes — confirm current details on each provider's site.

Educational content. Not financial, tax, or investment advice. For your situation, consult a CPA or licensed professional.

Reviewed July 2026.