Valued at $26.9 billion by market cap, Coterra Energy Inc. (CTRA) is a Texas-based independent exploration and production company focused on natural gas, oil, and natural gas liquids. It operates as a pure upstream energy player, meaning its core business is discovering, developing, and producing hydrocarbons rather than refining or distributing them.

CTRA has surged 42.2% over the past year, outshining the broader S&P 500 Index ($SPX), which rallied nearly 29%. It has rallied 34.4% on a YTD basis, comfortably outpacing the index’s 5.6% year-to-date gain.

Narrowing the focus, CTRA has trailed the State Street SPDR S&P Oil & Gas Exploration & Production ETF (XOP), which has soared 56.8% over the past year and 39.3% rise in 2026.

Coterra Energy’s robust momentum over the past year is driven by strong commodity pricing, disciplined capital spending, and robust free cash flow generation. Its balanced exposure to both oil and natural gas allowed it to benefit from favorable market conditions, while efficient operations and high-return drilling supported margins. Additionally, consistent shareholder returns through dividends and buybacks, along with broader investor rotation into energy stocks, have further boosted its performance.

For FY2026, which ends in December, analysts expect CTRA’s EPS to grow 44.2% to $2.87 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in two of the last four quarters while missing the forecast on two other occasions.

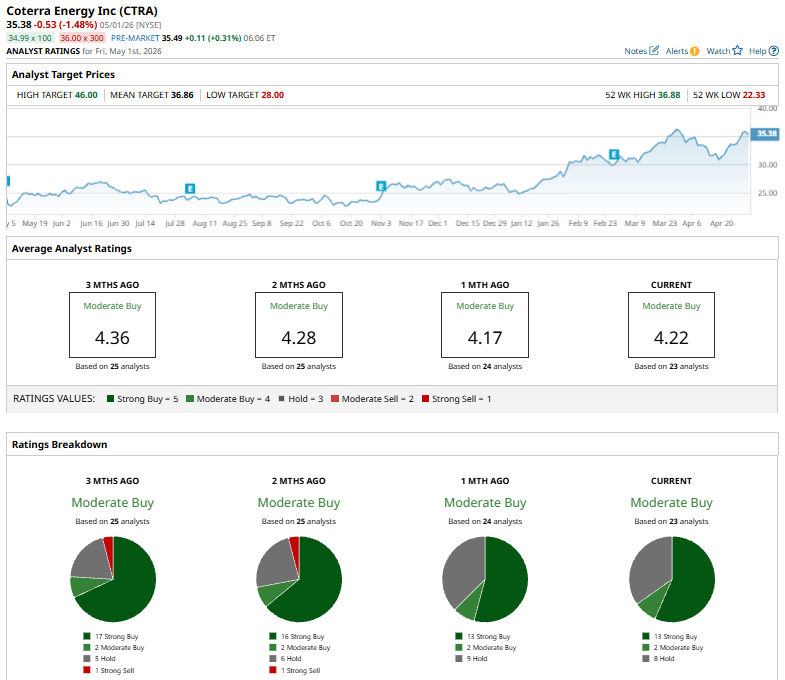

Among the 23 analysts covering CTRA stock, the consensus is a “Moderate Buy.” That’s based on 13 “Strong Buy” ratings, two “Moderate Buys,” and eight “Holds.”

The current consensus rating is bearish than two months ago when the stock had 16 “Strong Buy” suggestions.

On Apr. 22, Scotiabank raised its price target on Coterra Energy to $32 from $31 while maintaining a “Sector-Perform” rating, reflecting a balanced outlook. The update comes amid a broader reassessment of U.S. energy stocks, with the firm holding a mixed view on the sector, more optimistic on E&P earnings but cautious on refiners.

The mean price target of $36.86 represents a 4.2% premium to CTRA’s current price levels. The Street-high price target of $46 suggests an ambitious upside potential of 30%.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Huge, Unusual Volume of Amazon Options Trade Today - As AMZN Moves Up

- Seagate and Western Digital Are a Hard Disk Drive Duopoly. Barchart Ranks the Storage Stocks Here.

- PayPal Needs to Focus on Growth, So Exercise Caution with PYPL Stock Before May 5

- Caterpillar Stock Is Anything but Boring as a Data Center Boom Lifts Shares 170%