Valued at $124.6 billion by market cap, Altria Group, Inc. (MO) is a leading consumer staples company focused on tobacco and nicotine products. Headquartered in Richmond, Virginia, Altria operates primarily in the United States and owns some of the most recognizable brands in the industry, including Marlboro, the dominant cigarette brand in the U.S.

Shares of this leading tobacco company have underperformed the broader market over the past year. MO has gained 25.7% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 29%. However, momentum has shifted in 2026, with MO rising 29.3% year-to-date, significantly outperforming the index’s 5.6% gain.

Zooming in further, MO has outpaced the State Street Consumer Staples Select Sector SPDR Fund (XLP), which has surged 3.8% over the past year. Moreover, MO’s double-digit returns on a YTD basis outshine the ETF’s 8.4% rally over the same time frame.

On Apr. 30, Altria Group reported a solid Q1 2026, reporting adjusted EPS of $1.32, up 7.3% year-over-year and ahead of expectations, while revenue rose 3.2% to $5.42 billion. The performance was largely driven by robust pricing across its cigarette and oral tobacco portfolio, which more than offset ongoing declines in shipment volumes.

The company also returned significant capital to shareholders, paying $1.8 billion in dividends and repurchasing 4.5 million shares for $280 million at an average price of $62.33. Altria reaffirmed its FY2026 adjusted EPS guidance of $5.56 to $5.72, implying 2.5% to 5.5% growth from 2025, and now expects earnings growth to be more evenly split across the year following the strong first quarter. The results were well received, with the stock rising 6.5% after the announcement.

For the current fiscal year, ending in December, analysts expect MO’s EPS to grow 4.4% to $5.66 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters, while missing on another occasion.

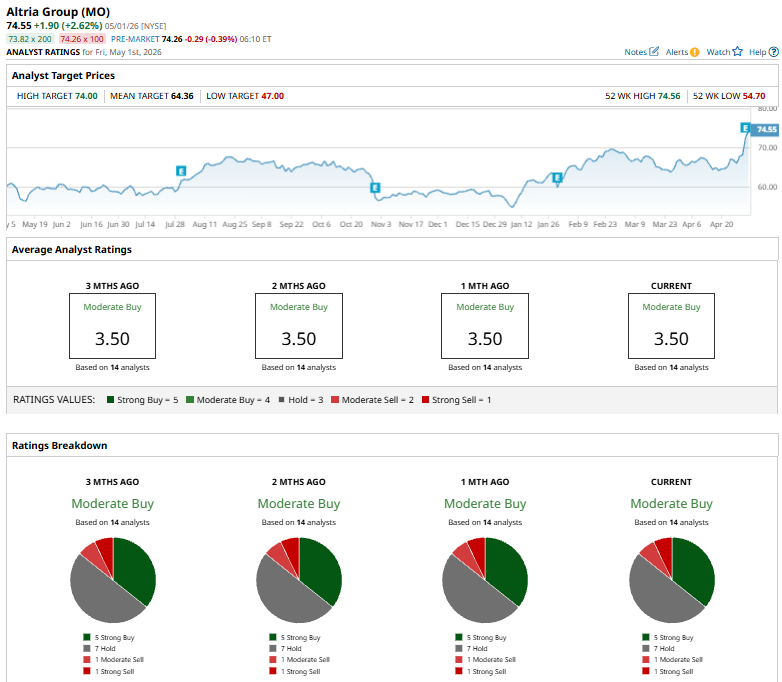

Among the 14 analysts covering MO stock, the consensus is a “Moderate Buy.” That’s based on five “Strong Buy” ratings, seven “Holds,” one “Moderate Sell,” and one “Strong Sell.”

The configuration has been consistent over the past three months.

On May 1, UBS Group raised its price target on Altria Group to $76 from $74 while maintaining a “Buy” rating, reflecting continued confidence in the stock. The upgrade comes despite the company issuing conservative FY2026 guidance, following a strong first-quarter performance.

The stock currently trades above both its mean price target of $64.36 and the Street-high price target of $74.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Huge, Unusual Volume of Amazon Options Trade Today - As AMZN Moves Up

- Seagate and Western Digital Are a Hard Disk Drive Duopoly. Barchart Ranks the Storage Stocks Here.

- PayPal Needs to Focus on Growth, So Exercise Caution with PYPL Stock Before May 5

- Caterpillar Stock Is Anything but Boring as a Data Center Boom Lifts Shares 170%