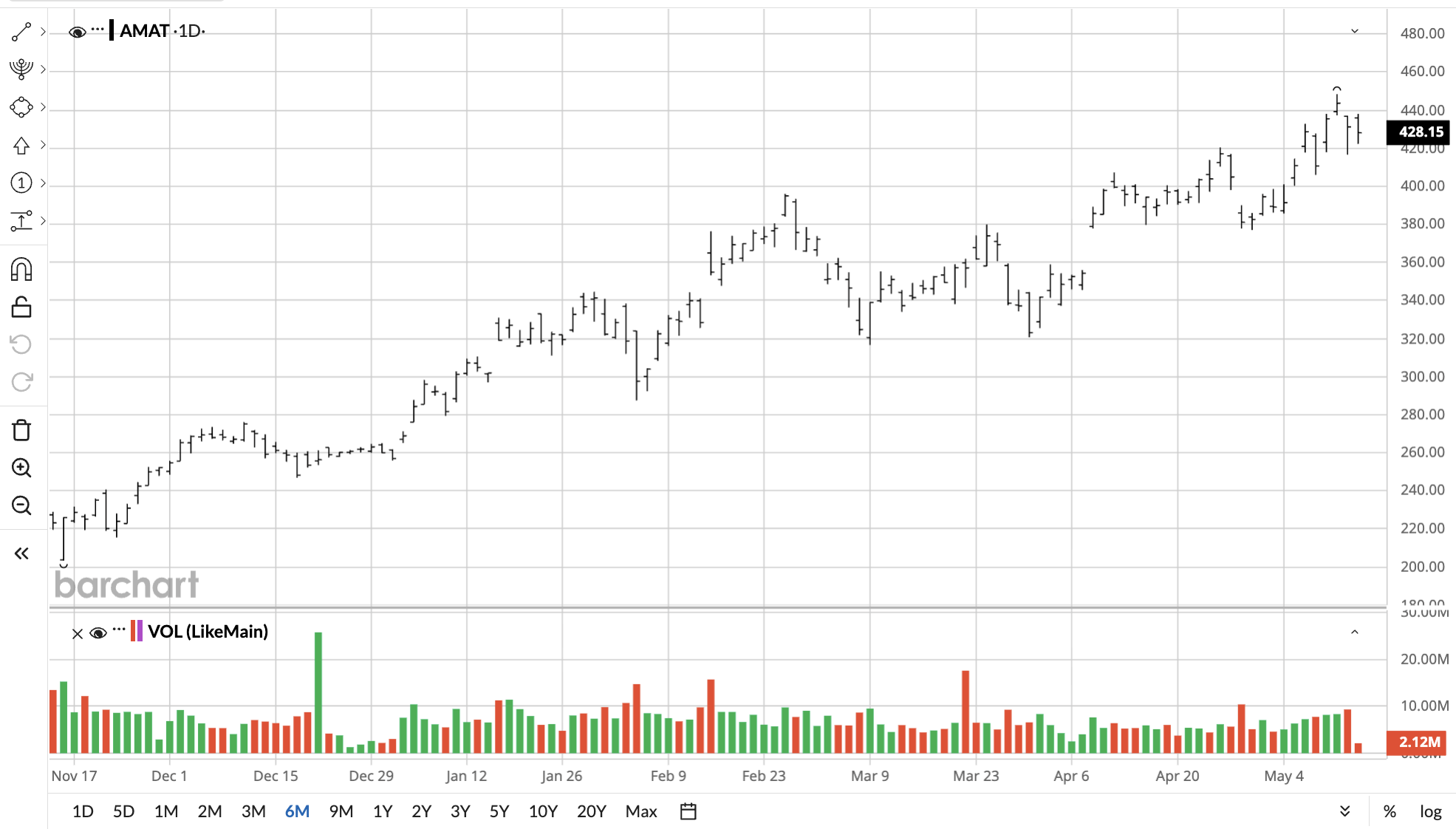

Applied Materials (AMAT) is one of the biggest suppliers of semiconductor manufacturing equipment, and relentless spending has caused the stock to climb 153.29% in just the past year. When major companies build a new fab, this company's tools are often the ones etching and inspecting the wafers. As hyperscalers keep spending on AI, the higher-margin Applied Materials' sales are expected to be.

Applied Materials is expected to confirm that trend on May 14 when it provides Q2 results after the closing bell. Knowing what to expect on earnings day will give investors an edge, because if Applied Materials keeps growing, another triple-digit move to the upside in the next year is a possibility. Its current valuation is at $342.2 billion, which isn't all that special during the AI rally.

Let's take a look at what the market expects and whether or not Applied Materials could reach a valuation of $500 billion and beyond.

Expectations for Q2

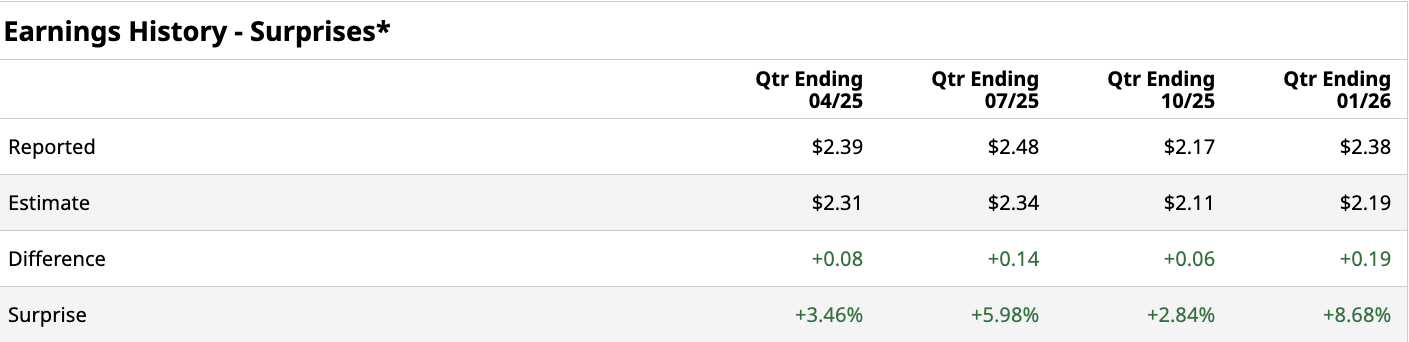

Analysts want to see revenue in the $7.68 billion to $7.7 billion band, but higher than that is always welcome. This would imply a growth rate of 5% - 8.5% year-over-year (YOY). EPS is expected to be $2.66 - $2.68, up from $2.39 in the year-ago quarter. Prior to this, Applied Materials' management had guided Q2 revenue “in the range of $7.15 billion to $8.15 billion” and adjusted EPS at ~$2.64. For the full year, EPS is expected to be $11.10.

Investors might expect AMAT stock to deliver a beat on both lines, just like it did in prior quarters. AI companies tend to underestimate their actual expectations, and analysts follow the guidance, so $7.9 billion to $8 billion wouldn't necessarily be out of range. The upper level of that estimate will likely spur a move above $450 billion in market cap over the coming quarter. This is less than 33% upside potential, so even that may be an underestimate if the broader rally accelerates.

As for EPS, I would expect it to come above $2.7 - $2.8. It has been beating EPS estimates consistently.

AMAT Stock Will Keep Being On Fire

Negative developments have surrounded the macroeconomy. Inflation is rising again and came in above expectations at 3.8%. This is bad, but I do not think this can derail the broader rally unless inflation returns cataclysmically high. Oil prices are to blame for any inflation, so it's not a 2022-like "structural" problem the Fed can blame to raise rates above 5% anytime soon.

And once you look beyond the macros, everything else is flashing green. Software companies are betting everything on AI, and even sensible players who were somewhat on the sidelines are stepping in. Hyperscalers are not just burning their cash. But they are actively going cash flow negative to fund more data centers.

And why wouldn't they? The market is happily rewarding it. As long as Wall Street reacts positively to higher spending, you're going to see a self-reinforcing loop that could continue for years. Even in 2023, bulls wouldn't have expected close to a trillion in data center spending.

Sam Altman asked for $7 trillion to make AGI come true. The spending is looking less and less absurd each year that goes by, regardless of whether or not AGI comes true.

All of these factors should keep AMAT stock riding high.

AMAT is Overpriced (In Relative Terms). Here's What You Can Do

Even though I expect AMAT stock to keep going up due to market irrationality, you should keep in mind that there are better options out there. I wouldn't put all my eggs into this stock because it trades at nearly 39 times forward earnings.

The revenue growth rate over the coming years is expected to be ~15% annually on average, along with 20% annual EPS growth at best. And this is if the market keeps being rosy about AI demand.

Instead of buying companies that sell equipment to chipmakers, I'd just buy the chipmaker stocks instead, regardless of the results of earnings day for Applied Materials. The moat for companies like Nvidia (NVDA) or AMD (AMD) is far bigger.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Super Micro Computer Just Promoted a New Chief Business Officer as It Aims for a Turnaround

- Ahead of Intuitive Machines Earnings, Here Is What Barchart Options Data Shows for LUNR Stock

- GF Securities Reckons Qualcomm Will Be a Hit in the CPU Server Cycle. QCOM Stock Has a Rocky Road Ahead.

- MSFT Stock Alert: What to Know as LinkedIn Plans 2026 Layoffs