The U.S. airline business has had a rough 2026. Jet fuel prices have jumped roughly 130% year-over-year (YOY), squeezed by geopolitics and supply cuts, and that’s hit profit margins and pushed the U.S. Global Jets ETF (JETS) and most airline stocks lower since March.

In the middle of that stress, United Airlines (UAL) CEO Scott Kirby reportedly suggested a potential megamerger with American Airlines (AAL) in talks with U.S. officials in Washington, D.C., causing AAL to jump 8.9% in one day on the headline.

The excitement faded fast. On April 17, the company put out a clear statement: “American Airlines is not engaged with or interested in any discussions regarding a merger with United Airlines,” calling the idea “negative for competition and for consumers.” Within hours, AAL fell 4.23%.

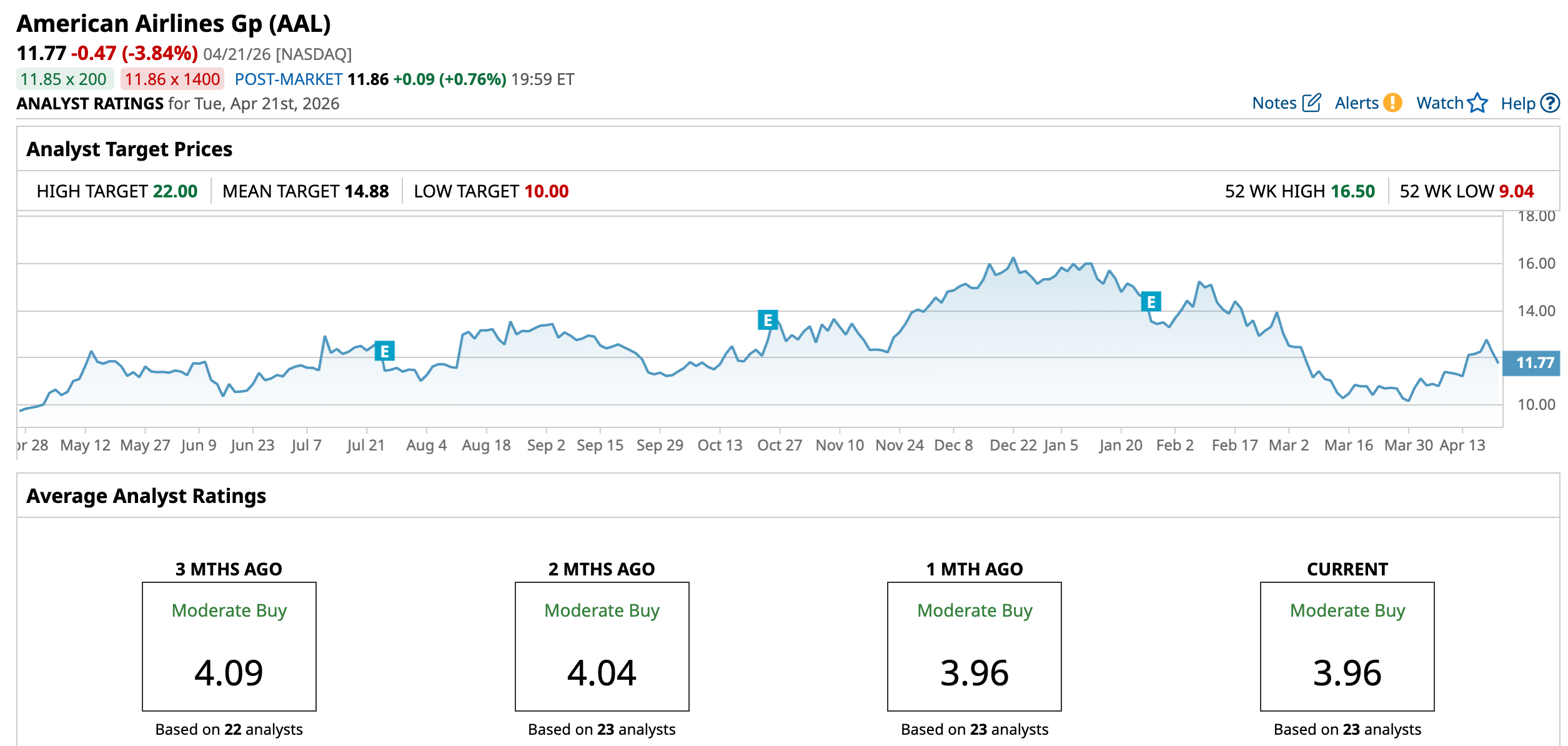

That swing captures where the stock is now. American heads into its April 23 earnings report trading about 27.6% below its 52-week high of $16.26 set in December, with a market cap of $8.08 billion and a negative book value of $5.65 per share.

With the merger talk off the table, can American’s own numbers and strategy carry the stock, or is this setting up for a crash landing? Let’s find out.

What American Airlines’s Numbers Really Say

American Airlines is still basically a traditional full‑service airline. It flies a big domestic and international network, then tries to make extra money from loyalty programs, co‑branded credit cards, and premium services on top of base ticket prices.

Over the past 52 weeks, that has resulted in a 29.77% gain for the stock, but year-to-date (YTD), it’s still down 23.22%.

On the numbers, American Airlines delivered record Q4 revenue of $14.0 billion and record full‑year revenue of $54.6 billion, showing demand and pricing are holding up. The U.S. government shutdown still knocked about $325 million off Q4 revenue, a reminder that politics can hit results fast.

Profit is much thinner. GAAP net income was $99 million in Q4 and $111 million for 2025 (or $0.15 and $0.17 per share), and even adjusted earnings were just $106 million and $237 million (or $0.16 and $0.36 per share). That’s not a lot for a company with a heavy debt load, even after cutting total debt by $2.1 billion in 2025. Management is now guiding to 2026 adjusted EPS of $1.70–$2.70 and more than $2 billion in free cash flow.

Can American Airlines Still Climb on Its Own?

American Airlines’ expanded co‑brand deal with Citi (C) in late March 2026 builds on a relationship that’s been in place for almost 40 years around AAdvantage credit cards, and now stretches into the Admirals Club lounge network. That’s important for shareholders because card spend and lounge perks tend to keep higher‑value customers loyal, and those customers usually bring in more fee and ancillary revenue than a passenger simply buying the cheapest seat.

On top of that, the new America250 partnership ties American Airlines into the U.S. 250th anniversary celebrations with branding, special projects, and support around the events. That kind of national‑level visibility and political goodwill matters for an airline that lives under a tight regulatory spotlight.

Then you have the FIFA World Cup 26 marketing tie‑up with Qatar Airways, which puts American Airlines in front of a huge global audience through special aircraft liveries, promos, and “last chance” ticket pushes. That is aimed squarely at boosting international visibility and drawing in more premium leisure and corporate travelers, the exact kind of higher‑yield traffic AAL needs if it wants the stock to rerate on its own story.

Wall Street’s Call

For Q1 2026, analysts see a loss of about $0.45 per share, better than the $0.59 loss a year ago. For Q2 2026, they’re modeling a $0.26 loss, a sharp drop from $0.95 in profit last year, so they’re clearly bracing for a weaker summer. For all of 2026, the average forecast is a $1.05 loss per share, versus $0.36 in earnings in 2025.

UBS’s Atul Maheswari has a “Strong Buy” on AAL and recently raised his target from $14 to $16, saying the market is too focused on the debt and not giving enough credit for premium demand and loyalty revenue as travel normalizes. Citigroup’s John Godyn is also at “Strong Buy,” but cut his target from $21 to $14, so he likes the story, just with more modest upside.

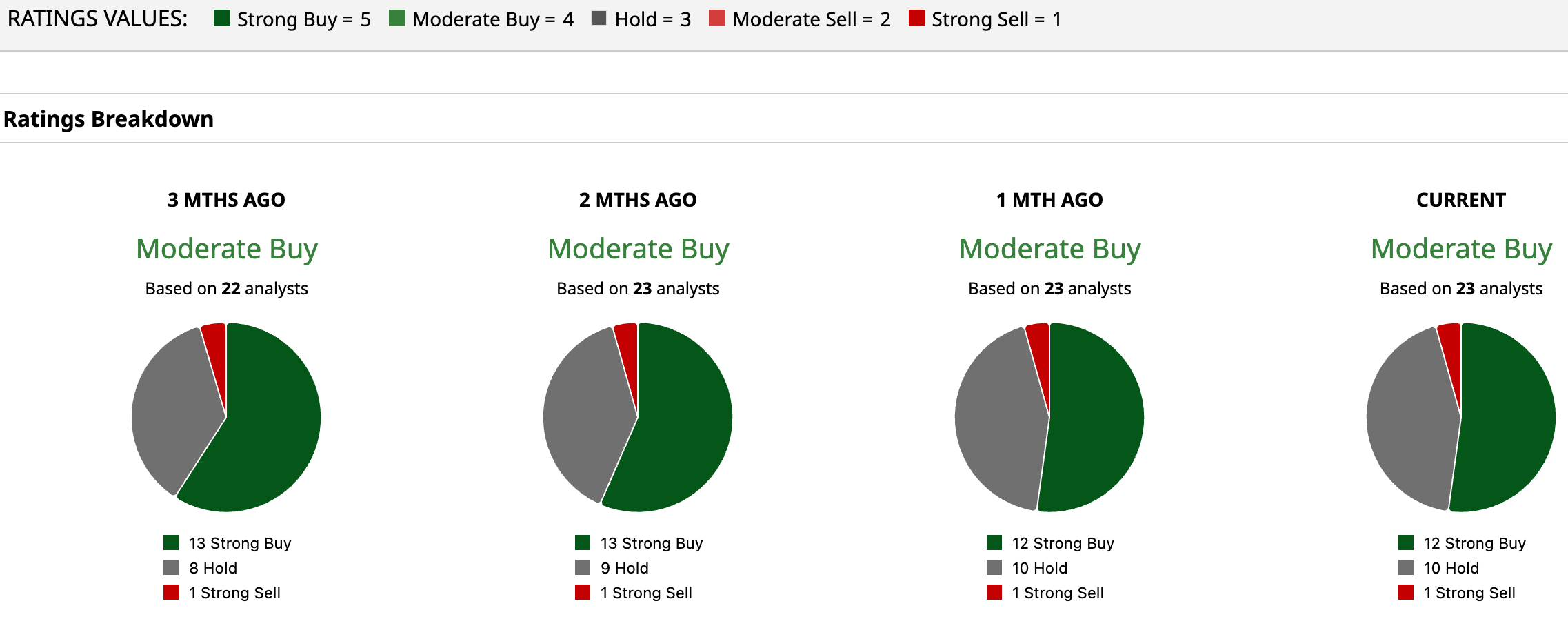

Taken together, all 23 analysts tracked are positive enough for a “Moderate Buy” consensus, and the average target of $14.88 points to 26.4% upside from recent prices.

Conclusion

American Airlines’s merger denial effectively forces investors to judge AAL on its own cash flows, balance sheet and execution. With jet fuel costs spiking, earnings expected to dip into a full‑year 2026 loss before a sharp 2027 rebound, and a still‑heavy debt load sitting on top of a negative book value, this is nowhere near a low‑risk “set it and forget it” stock. At the same time, double‑digit upside to the Street’s mean target, growing loyalty and co‑brand economics, and the potential for more than $2 billion in 2026 free cash flow argue that the equity is not priced like a total write‑off either. AAL looks more like a "Speculative Buy” for investors who can stomach volatility than an imminent crash landing, with the most likely path being a range‑bound grind higher rather than a clean melt‑up or collapse.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Axe Compute Soars on $260M Nvidia Deal. Is It Too Late to Buy AGPU Stock?

- This Delta Insider Just Slashed His Stake by More Than One-Fifth (21%). Is It Time to Follow Suit and Ditch DAL Stock?

- AMD Stock Just Hit New All-Time Highs. Should You Buy Shares Here?

- The ‘ChatGPT Moment’ for Cadence Design Systems Might Just Have Arrived, Says Needham. Should You Buy CDNS Stock Now?