Wall Street's leading financial institution, Morgan Stanley, reckons that AI-led data analytics company Palantir (PLTR) will continue to experience strong growth in the coming times. Palantir's stock has been an unstoppable juggernaut in recent years. Yet, amid concerns around valuations and questions of irrelevance from the likes of Michael Burry, Palantir continues to find backers.

The Sanjit Singh-led team of analysts at Morgan Stanley has now given its vote of confidence for Palantir (and several other software stocks). Specifically for Palantir, it noted, "Fundamentals remain exceptionally strong, with accelerating U.S.-led growth, expanding large-customer adoption, and best-in-class margins, making the path to $10B in revenue increasingly credible."

So, PLTR stock is now valued at $350 billion, and its stock is down 18% on a year-to-date (YTD) basis. Is this an opportune moment then to heed Morgan Stanley's optimism about Palantir and load up on its stock? Let's examine.

Exceptional Financials

A mere glance at Palantir's financials, and one can figure out what that "fundamental momentum" Morgan Stanley is talking about, as Palantir delivered another strong set of numbers for Q4.

The company tracks its performance through the Rule of 40, which adds together revenue growth and operating margin. Scores above 40% are viewed as solid, and Palantir achieved an impressive 127% in its most recent period.

Notably, revenue reached $1.41 billion, reflecting a 70% increase from the same quarter a year earlier. Earnings per share climbed 78% to $0.25, exceeding what analysts had anticipated. At the same time, the operating margin widened to 57% from 45% in the prior year period.

Commercial revenue continued to narrow the difference with government revenue. In the United States, commercial revenue jumped 137% to $507 million, while government revenue advanced 66% to $570 million. The total value of contracts signed during the quarter rose 138% year over year to $4.26 billion. This surge points to healthy demand and greater clarity around upcoming revenue streams.

Cash generation stayed solid as well. Net cash provided by operating activities increased 69% compared with the previous year, and adjusted free cash flow grew 53% to $791.4 million. Overall, Palantir closed the quarter holding $1.42 billion in cash while carrying just $45.86 million in short-term debt.

Looking ahead to the first quarter, the company projected revenue in the range of $1.532 billion to $1.536 billion. For the entire year of 2026, Palantir expects revenue to hover between $7.182 billion and $7.198 billion. Taking the midpoint of that guidance suggests roughly 140% growth for the first quarter and around 60% growth for the full year.

Yet, valuation continues to stand out as the main point of attention for investors. The stock currently trades at a forward P/E ratio of 110.70 times, a P/S ratio of 48.16 times, and a P/CF ratio of 98.78 times. Each of these multiples sits well above typical levels for the sector. Even the forward PEG ratio, which accounts for the company's exceptional growth rate, comes in at 2.41 versus a sector median of 1.36.

Palantir's Prowess

Palantir's technological moat through its Ontology moat and what it is doing to stay ahead in the race have been discussed threadbare by me in various pieces, with the latest one also highlighting how it is looking to increasingly corner the commercial market.

And the fears around Anthropic rendering Palantir obsolete are also misplaced. High switching costs and the entrenchment of Palantir in its customers systems and processes make it extremely difficult for companies to just wake up one day and shun Palantir for an LLM, which are becoming increasingly commoditized by the day. For instance, Anthropic's Claude may be ahead of others like Gemini and ChatGPT now; however, some months down the road, that may not be the case. Moreover, Palantir maintains flexibility by working with a range of artificial intelligence systems. Through its AIP platform, the company readily integrates offerings such as Claude, GPT-4, Llama, and additional options as needed. As a result, some of the potential growth benefits for Anthropic extend into Palantir within enterprise environments, although the opposite does not apply. Thus, Palantir functions as a user of Anthropic solutions rather than a direct rival in the space.

Further, Palantir offers a comprehensive platform that brings together multiple capabilities. It handles data integration via Foundry, delivers immediate operational insights through Gotham, supports AI-driven evaluations and systems with AIP, assigns particular functions to Maven, and manages software deployment with Apollo. In a notable recent success for Maven specifically, it gained recognition as an official program of record. This designation establishes it as a formally authorized, funded, and extended acquisition initiative for the Pentagon. Such progress stands as a clearly favorable signal for Palantir. It strengthens the company's prospects for securing additional contracts inside the United States and sends an encouraging message regarding its goals in global markets.

Beyond that, Palantir stands well prepared to address what enterprises require when feeding reliable information into AI processes. This enables strong results, including the ability to finish enterprise resource planning migrations in as little as two weeks instead of the two years these projects traditionally demanded. Notably, the foundation supporting these achievements stems from the extensive and detailed efforts Palantir has invested over many years to develop a structured understanding of data across organizations. This work continues to deepen the company's competitive advantage.

Analyst Opinion on PLTR Stock

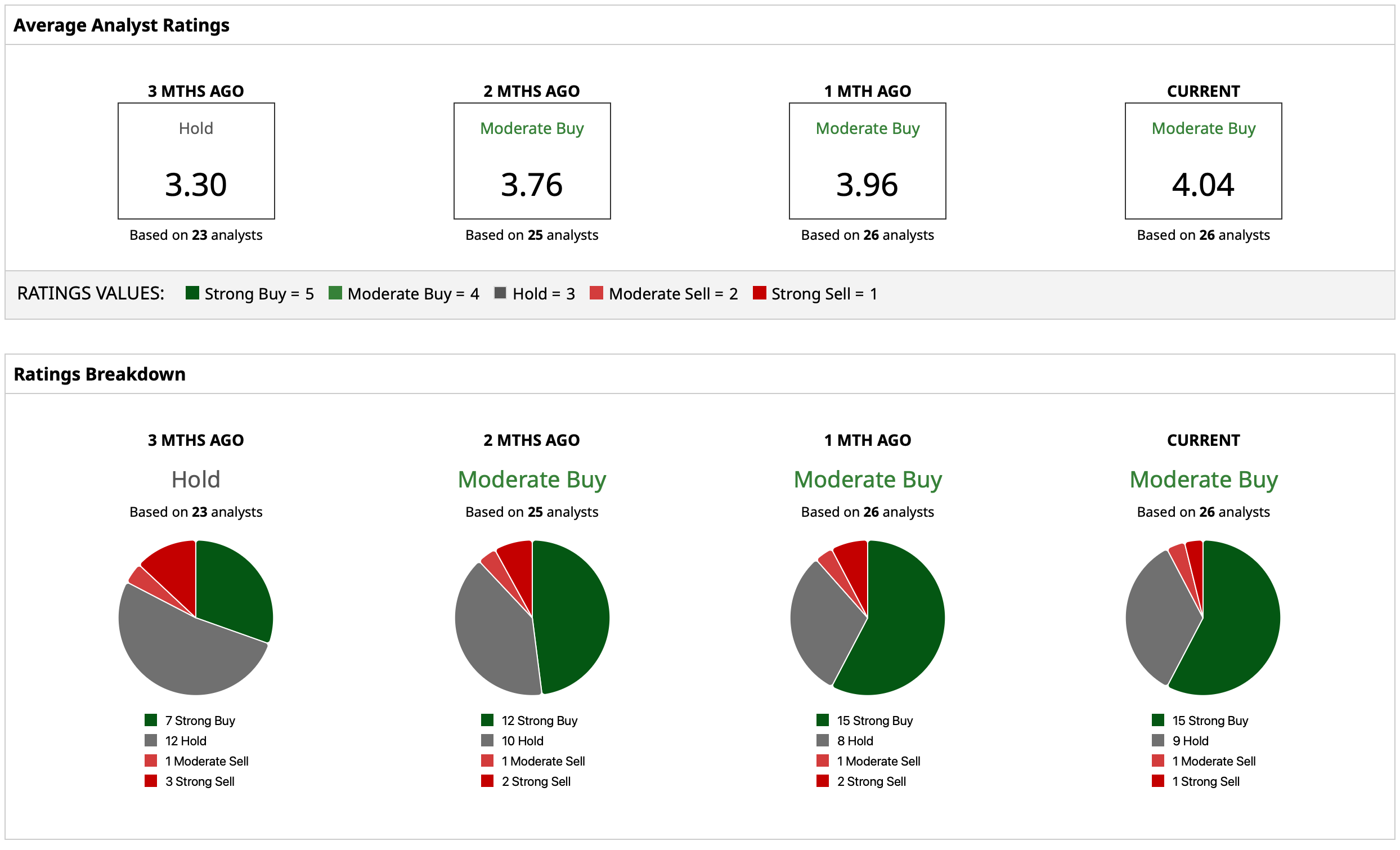

Overall, analysts have attributed a consensus rating of “Moderate Buy” to PLTR stock. The mean target price of $197.87 denotes an upside potential of about 35.2% from current levels. Out of 26 analysts covering the stock, 15 have a “Strong Buy” rating, nine have a “Hold” rating, one has a “Moderate Sell” rating, and one has a “Strong Sell” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tilray Stock Pops on New Trump-Driven Cannabis Hopes. Should You Chase the Rally?

- Tim Cook Is Stepping Down as Apple CEO, AAPL Stock Dips in After-Hours Trading

- Save This Psychedelic Stock Watchlist After Trump’s Latest Executive Order

- BlackBerry Stock Is Soaring on a New Nvidia Deal. Does That Make BB a Buy Here?