With artificial intelligence (AI) driving explosive demand for computing power, chipmakers are in the spotlight like never before. Investors have poured money into anything tied to data centers and advanced manufacturing. Yet one name that has spent years on the sidelines — Intel (INTC) — is staging a comeback that’s turning heads.

With INTC stock now trading near $70 and just steps away from its 2020 peak, the momentum it has built this year looks built to last.

Intel’s Blazing Year-to-Date Surge

Intel shares have returned 86% year-to-date (YTD). That’s not just a recovery, but a full reclamation of lost ground. INTC stock closed at $68.50 on April 17 after reaching a 52-week high of $70.32, its highest level since 2020.

Compare that to the broader market. While the S&P 500 ($SPX) has posted modest single-digit YTD gains, Intel has delivered well above that return. Meanwhile, the semiconductor industry — tracked by benchmarks like the VanEck Semiconductor ETF (SMH) — is up about 29% YTD. That's solid, but a return that Intel has also outpaced.

In short, INTC stock isn’t just riding the AI wave. It’s outrunning the sector.

The Data-Center Pivot and Fresh Foundry Wins

Here’s what changed everything. Intel deliberately shifted manufacturing capacity away from consumer PCs toward data-center processors. AI workloads have created insatiable demand for Xeon server chips, and the company responded by prioritizing those wafers. Data-center revenue jumped to $4.7 billion in the most recent quarter. That move, while tightening PC supply and pressuring short-term client sales, has supercharged the higher-margin side of the business.

The foundry business supplies the rocket fuel. In recent weeks, Intel has signaled new external customers and deepened ties with big names. Reports have surfaced of Apple (AAPL) exploring Intel fabs for future chips, while Microsoft (MSFT) and Amazon (AMZN) continue custom AI silicon collaborations with Intel, and Alphabet's (GOOGL) Google collaborates on custom infrastructure processing units.

Intel also repurchased full ownership of its key Ireland Fab 34 for $14.2 billion, giving it total control over European advanced-node output. Progress on the 18A process node has Wall Street buzzing about Intel potentially becoming the No. 2 foundry behind Taiwan Semiconductor Manufacturing (TSM).

These aren’t vague promises. They’re concrete steps that fill capacity, diversify revenue, and reduce reliance on the PC cycle. Granted, consumer demand remains soft and memory prices are squeezing margins industry-wide. But the data-center tailwind and foundry pipeline give Intel multiple growth levers that simply didn’t exist a year ago.

Intel’s Valuation Tells an Intriguing Story

Intel trades at 6.14 times sales, 2.57 times book value, and 28.96 times cash flow. The trailing price-to-earnings (P/E) ratio sits at 0 times because the company posted a small per-share loss of $0.6 over the last 12 months. That loss reflects heavy restructuring costs, yet the price-to-sales (P/S) multiple looks reasonable when you consider the foundry upside still ahead. Compare that with pure-play foundry or data-center peers trading at far richer multiples, and Intel’s valuation leaves room for expansion as earnings turn positive.

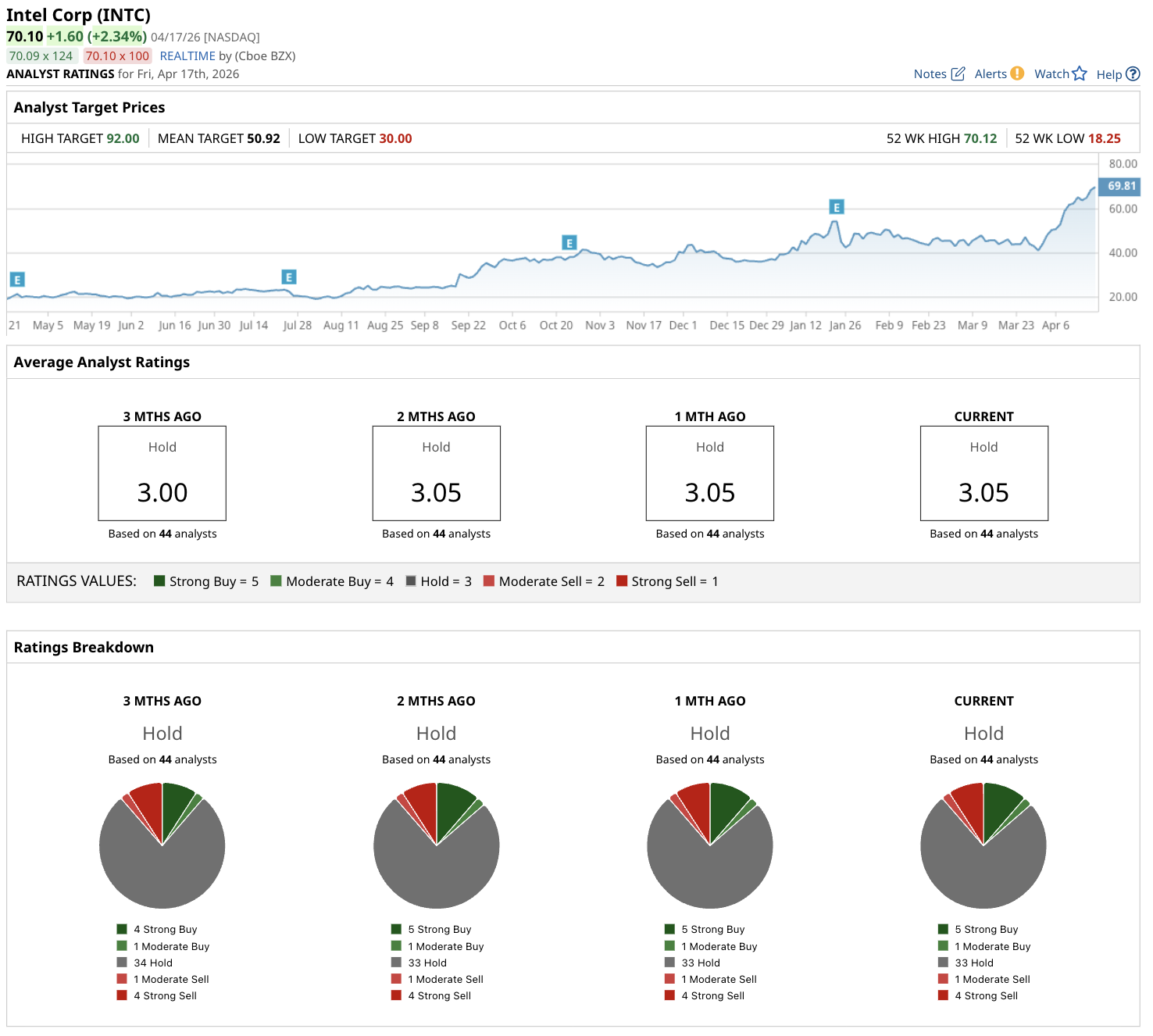

What Do Analysts Think About INTC Stock?

Wall Street has a consensus "Hold" rating on INTC stock, with a mean recommendation score of 3.05 on a 1-to-5 scale. That cautious collective view reflects the work still needed on margins and execution. Of the 44 analysts with coverage, five analysts have a "Strong Buy" recommendation, one has a "Moderate Buy," 33 have a "Hold" rating, one analyst has a “Moderate Sell,” and four analysts have a "Strong Sell."

Yet several firms have raised price targets in recent months, citing foundry momentum and data-center demand. The mean price target of $50.92 indicates potential downside of 26%. No one expects an overnight miracle, but Wall Street is clearly missing the path higher if Intel delivers on its 18A roadmap.

The Key Takeaway

Intel has already proved the doubters wrong by reclaiming nearly all its lost ground in a single year. The combination of a deliberate data-center pivot, fresh foundry partnerships, and still-reasonable valuation gives INTC stock a clear runway toward that new all-time high.

That said, competition remains fierce and profitability must improve. For patient investors who buy the transformation rather than yesterday’s headlines, the data supports staying the course — while keeping an eye on quarterly execution. The next chapter looks a lot brighter than the last.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Trump Sends Compass Pathways Stock Soaring as He Backs Psychedelics. Should You Buy CMPS Here?

- As Oracle Launches New Agentic AI Tools, Should You Buy, Sell, or Hold ORCL Stock?

- Is GOOG Stock a Buy Ahead of Q1 Earnings and Amid Fragile Peace in the Middle East?

- Snap Just Announced Major Layoffs: What Do 1,000 (16%) Job Cuts Mean for SNAP Stock?