Tesla (TSLA) was once the undisputed king of growth stocks, delivering jaw-dropping returns and redefining the auto industry. But soon followed a volatile period of slowing EV growth, rising competition, heavy spending, and lofty valuation. Tesla will report its first-quarter earnings on April 22 after the market closes. Recently, the company reported a 6.3% year-over-year (YoY) increase in Q1 delivery. The stock is down 12% YTD, underperforming the S&P 500 Index ($SPX) gain of 4%, and is down almost 21% from its 52-week high of $498.83.

Investors now wonder if Q1 will push TSLA stock to reclaim its former glory and surge toward $600?

From Market Darling to Market Doubts

Not long ago, Tesla was the poster child of innovation-led investing. Its dominance in electric vehicles (EVs), combined with Elon Musk’s bold vision, pushed the stock to extraordinary highs. However, Tesla’s recent quarterly performances have been disappointing. Slowing vehicle demand in key markets, increasing competition from traditional automakers and new EV entrants, particularly in China, and margin compression have weighed heavily on investor sentiment.

Despite these concerns, Tesla remains far from a broken story. Over the past year, TSLA stock has climbed 35%. Tesla’s stock performance has reflected Musk’s ambitious visions and their future potential rather than the company’s current performance.

In the fourth quarter of 2025, Tesla’s core automotive segment revenue fell 11% YoY to $17.7 billion. Revenue for the segment also fell 10% to $69 billion for the full year. However, its energy generation, storage, and services areas saw double-digit growth. With increasing global demand for renewable energy and grid stabilization, Tesla’s Megapack and Powerwall products are gaining traction. Total revenue dipped 3% for the year to $94.3 billion, while adjusted earnings also saw a 28% slump to $1.66 per share.

Tesla is transitioning from an automotive firm to a robotics and artificial intelligence (AI) powerhouse. It has already begun operating completely autonomous rides without safety drivers in select areas, marking a significant milestone in real-world implementation. If Tesla is successful in scaling its robotaxi network, it may be able to create a high-margin, recurring revenue model similar to ride-hailing companies, but without the need for human drivers. One of Tesla's most ambitious projects is Optimus, a humanoid robot. While still in its early stages, Musk believes Optimus is capable of evolving into a general-purpose robot capable of learning tasks by studying humans. If successful, Optimus might create totally new markets, ranging from manufacturing and logistics to domestic services.

Tesla’s transition phase involves massive capital expenditure, with plans to invest over $20 billion in factories, AI infrastructure, and new product lines in 2026. This includes investments in battery production, AI chips, robotics, and manufacturing capacity. It will be clear in the Q1 earnings if this level of spending is pressuring margins in the near term. Investors must then decide if these investments are visionary or overly risky.

Can April 22 Reignite Momentum?

In Tesla’s Q1 earnings, investors should keep an eye on vehicle delivery trends, margins, automotive business growth, progress in autonomy, and updates on new initiatives like robotaxis and Optimus. Any positive surprise, particularly related to Full Self-Driving (FSD) adoption or robotaxi rollout, could quickly shift sentiment. Markets usually tend to reward future potential, and Tesla’s story is still highly influenced by its future rather than its present. However, disappointments in margins and core operations may pressure the stock in the short term.

Analysts expect Tesla to report a 15.5% increase in Q1 revenue to $22.3 billion, with earnings jumping by 33.3% to $0.36 per share. Tesla has missed three consensus revenue and earnings estimates in the last two years. If Tesla beats expectations this quarter and improves its fundamentals, the market may turn in TSLA stock’s favor.

For the full year, analysts predict earnings climbing 22% to $2.03, followed by a 35.8% increase in 2027 to $2.75. While the projections are optimistic, Tesla’s valuation is concerning. Trading at 145x forward 2027 earnings, Tesla stock is expensive, reflecting the market’s faith in Musk’s bold vision translating into growth.

Is a $600 Target Price Realistic?

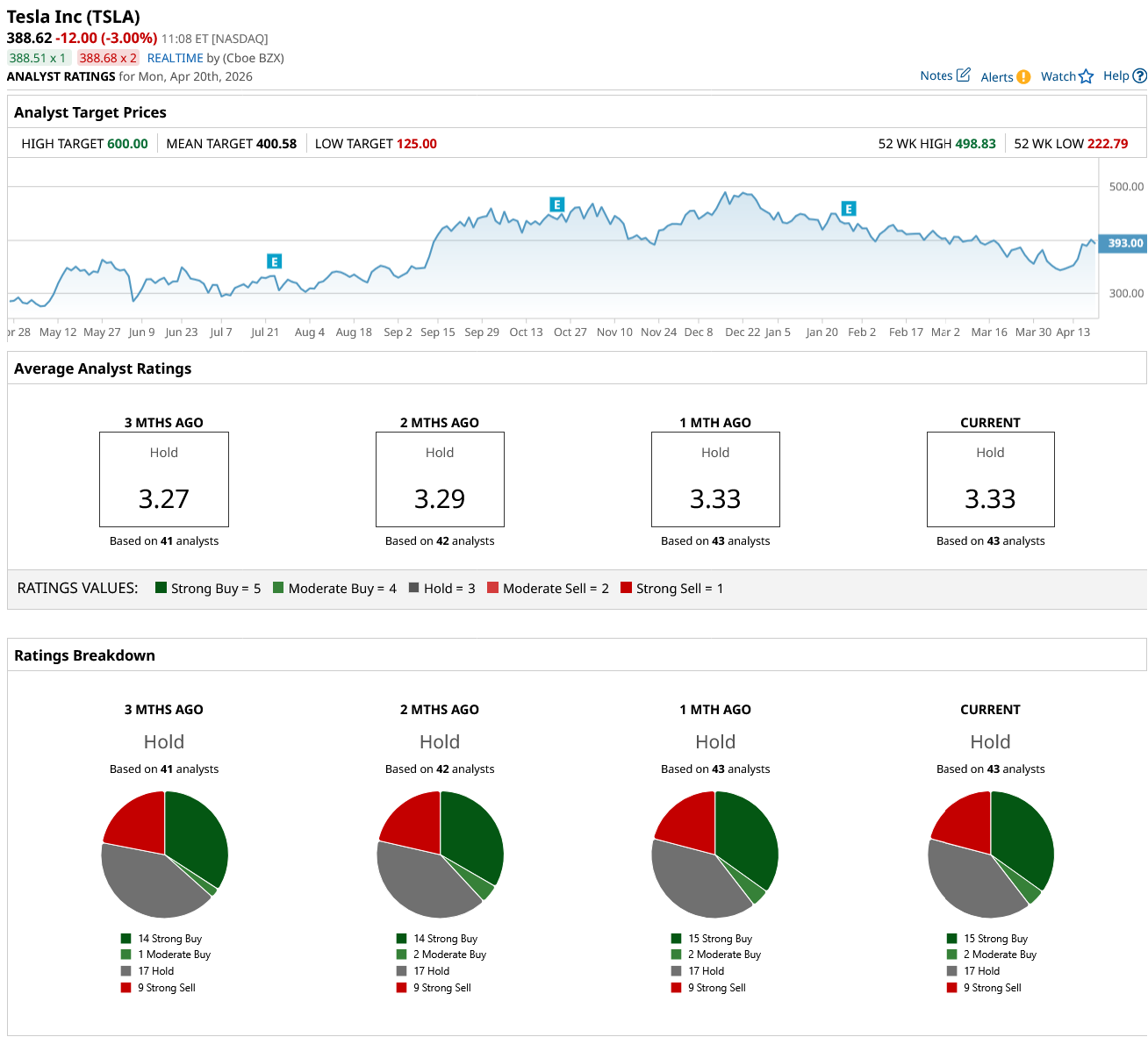

TSLA has been trading very close to its average price target of $400.58. However, the high price estimate of $600 implies that the stock can rise by 55% in the next 12 months. Reaching $600 by 2027 is not an impossible target. If Tesla delivers on all of Musk's ambitious claims, its increased valuation may be justified. Tesla has never lacked ambition. But only time will tell if such innovation leads to scalable, profitable businesses.

Tesla remains a high-risk, high-reward bet. Investors that still have faith in the company’s long-term goals might want to grab the stock on the dip now before its Q1 earnings release on April 22.

On Wall Street, TSLA stock is an overall “Hold.” Out of the 43 analysts covering the stock, 15 rate it a “Strong Buy,” two recommend a “Moderate Buy,” 17 rate it a “Hold,” and nine recommend a “Strong Sell.”

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Tilray Stock Pops on New Trump-Driven Cannabis Hopes. Should You Chase the Rally?

- Tim Cook Is Stepping Down as Apple CEO, AAPL Stock Dips in After-Hours Trading

- Save This Psychedelic Stock Watchlist After Trump’s Latest Executive Order

- BlackBerry Stock Is Soaring on a New Nvidia Deal. Does That Make BB a Buy Here?