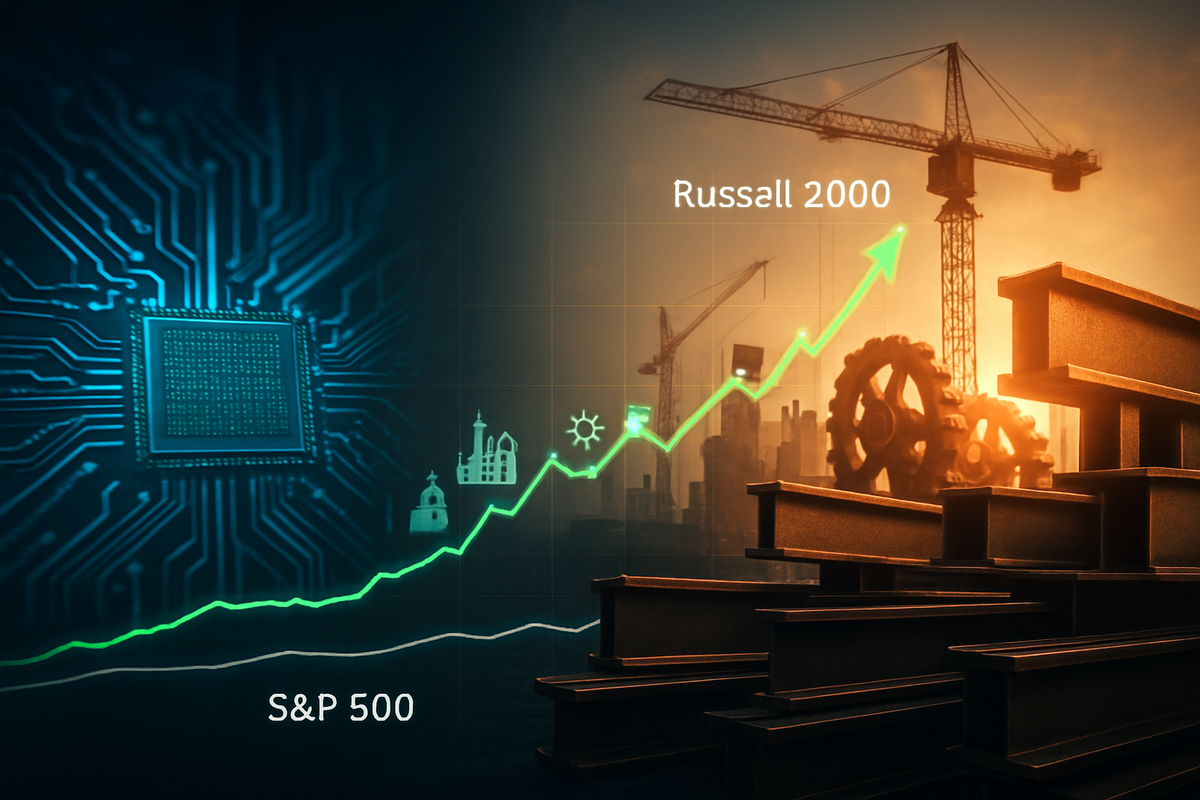

As of March 30, 2026, the long-awaited "Great Rotation" in the U.S. equity markets has transitioned from a theoretical prediction to a dominant market reality. In a striking reversal of the trends that defined the early 2020s, the Russell 2000 Index, representing small-cap stocks, has surged by 6.10% year-to-date. This robust performance stands in stark contrast to the sluggish 0.65% return posted by the S&P 500 over the same period, signaling a decisive move away from the mega-cap technology companies that previously carried the market on their shoulders.

This divergence marks the widest performance gap between small and large-cap indexes in over a decade. Investors are increasingly pivoting toward "underdog" stocks and cyclical sectors, driven by a stabilization in interest rates and a domestic manufacturing renaissance. As the "AI Capex Cliff" begins to weigh on the valuations of trillion-dollar tech titans, the broader market is finding fresh legs in the industrial heartland and the raw materials that fuel it.

From Silicon to Steel: The Mechanics of the 2026 Surge

The primary catalyst for this shift has been a fundamental re-evaluation of the American economic landscape. Throughout late 2025 and into early 2026, the Federal Reserve successfully navigated a "soft landing," bringing the federal funds rate to a neutral stance between 3.50% and 3.75%. This stability has acted as a massive relief valve for small-cap companies, which typically carry higher levels of floating-rate debt compared to their cash-rich large-cap peers. With the fear of further aggressive hikes off the table, the cost of capital for small businesses has finally become predictable, allowing for renewed expansion and hiring.

Simultaneously, the hype surrounding Artificial Intelligence has entered a "digestion phase." After years of massive infrastructure investment, investors are now demanding tangible returns from mega-cap tech, leading to a cooling of interest in stocks like NVIDIA (NASDAQ: NVDA) and Microsoft (NASDAQ: MSFT). This "AI Capex Cliff" has left a vacuum in the market, which has been rapidly filled by the "real economy" sectors. By mid-February 2026, the shift became undeniable as the Manufacturing PMI crossed back into expansionary territory, confirming that the industrial sector was once again growing.

The timeline of this resurgence can be traced back to the implementation of the "One Big Beautiful Bill" (OBBB), a significant fiscal stimulus package passed in 2025 that focused heavily on domestic infrastructure and energy transition. As these funds began hitting the balance sheets of smaller, specialized firms throughout the first quarter of 2026, the Russell 2000 began its steady climb. Market reactions were initially skeptical, but three consecutive months of small-cap outperformance have forced institutional funds to re-allocate billions into the space to avoid underperforming their benchmarks.

Winners and Losers in the New Industrial Age

In the Materials sector, small-cap players have turned into high-flyers. Rayonier Advanced Materials (NYSE: RYAM) has emerged as a standout winner, seeing its stock price jump significantly as global demand for high-purity cellulose recovered alongside the broader economy. Similarly, Tronox Holdings (NYSE: TROX) has capitalized on a tightening market for titanium dioxide, leveraging its vertically integrated structure to outpace larger, less nimble competitors. These companies are no longer viewed as peripheral "value traps" but as essential components of a modernized supply chain.

The Industrials sector has seen an even more dramatic re-rating. Companies like Gorman-Rupp Co. (NYSE: GRC), a specialist in pumping systems, have seen accelerated earnings growth as municipal and industrial infrastructure projects ramp up across the country. Willdan Group (NASDAQ: WLDN) has also become a darling of the 2026 market, with its focus on energy efficiency and infrastructure consulting perfectly aligning with the current fiscal priorities of the U.S. government. These firms are winning because they provide the physical tools and expertise required for "re-shoring"—the multi-year trend of bringing manufacturing back to American soil.

Conversely, the "losers" of early 2026 are found within the previously untouchable realms of software-as-a-service (SaaS) and high-multiple growth stocks. While these companies haven't necessarily collapsed, their lack of relative growth compared to the surging cyclical sectors has led to a stagnant quarter for the S&P 500. Large-cap tech firms are finding it difficult to maintain their 2024-level growth rates, and the market is no longer willing to pay a premium for "potential" when tangible earnings are available in the industrial and materials sectors at much lower valuations.

Policy, Infrastructure, and the Broader Trend

The current market environment is a direct reflection of broader shifts in global trade and domestic policy. The transition from "globalization" to "regionalization" has necessitated a massive buildup of domestic production capacity. This "Silicon to Steel" trend fits into a larger narrative where the physical constraints of the world—energy, raw materials, and logistics—have become more critical than digital scaling. This is not just a temporary blip; it is a structural realignment of the economy toward tangible assets and physical infrastructure.

Historically, this rotation bears a striking resemblance to the early 2000s, following the collapse of the dot-com bubble. Much like then, the current market is moving away from overvalued technology and toward "old economy" stocks that had been neglected for nearly a decade. The difference in 2026 is the role of government policy. The OBBB and previous infrastructure acts have created a long-term "floor" for demand in materials and industrials, making this rotation feel more durable than previous cyclical upturns.

Furthermore, the stabilization of inflation at roughly 2.7% has created a "Goldilocks" environment for cyclical sectors. It is low enough to prevent further rate hikes, but high enough to maintain the pricing power of companies in the materials space. As long as the "supercore" inflation remains supported by strong service and manufacturing demand, these cyclical companies will likely continue to see margin expansion, a luxury that many large-cap tech firms are currently losing as their input costs rise and consumer spending shifts toward physical goods.

Navigating the Road Ahead: Scenarios for the Rest of 2026

Looking toward the second half of 2026, the primary question is whether this small-cap lead is sustainable. In the short term, many analysts expect a "mean reversion" where large-cap tech finds a bottom, but the strategic pivot toward cyclicals appears to have institutional staying power. Smaller firms will need to adapt by reinvesting their current windfalls into automation and workforce development to stay ahead of persistent labor shortages, which remain the single largest hurdle for the industrial sector.

A potential challenge may emerge if the Fed decides that the economy is running "too hot," sparked by the very success of the industrial resurgence. If the Russell 2000 continues to outpace the broader market at its current rate, it could trigger concerns about a new inflationary spiral. However, the prevailing scenario is one of continued "broadening out." Investors should expect the market to move away from a handful of dominant names and toward a more democratic distribution of gains across sectors that have been undervalued for years.

The most likely outcome for the remainder of the year is a continued narrowing of the valuation gap between the Russell 2000 and the S&P 500. As more "passive" money is forced to rebalance into small-caps to match the shifting index weights, the momentum for the "underdogs" could carry well into 2027. This represents a massive opportunity for active managers who have been underweight cyclicals and are now scrambling to find quality names in the materials and industrials space before valuations reach parity with the rest of the market.

Summary of a Market in Motion

The first quarter of 2026 has provided a definitive answer to the question of what follows the AI-driven tech boom: a return to the fundamentals of the physical economy. The Russell 2000's 6.10% gain versus the S&P 500's 0.65% is more than just a statistic; it is a signal of a major regime change. With interest rates stabilized and a massive wave of infrastructure spending hitting the real economy, the "underdogs" of the materials and industrials sectors have finally taken center stage.

Moving forward, the market appears poised for a period of healthy, albeit different, growth. The dominance of the "Magnificent Seven" is being replaced by a more diversified list of winners that includes chemical manufacturers, industrial engineers, and raw material suppliers. This rebalancing is a sign of a maturing economic cycle that has moved past the initial excitement of new technologies into the hard work of building and sustaining a modernized industrial base.

For investors, the coming months will require a shift in focus. The "buy the dip" strategy for tech may still hold some merit, but the real alpha is currently being generated in the small-cap and cyclical arenas. Watching for continued strength in Manufacturing PMI data and monitoring the rollout of federal infrastructure funds will be key to determining the longevity of this trend. For now, 2026 remains the year of the small-cap, as the market rediscovers the value of the companies that build, move, and power the world.

This content is intended for informational purposes only and is not financial advice.