Globe Life Inc. (GL), headquartered in McKinney, Texas, provides various life and supplemental health insurance products, and annuities to lower middle- and middle-income families in the U.S. Valued at $12 billion by market cap, the company offers term, whole, and children's life insurance, as well as accidental benefits, mortgage protection, and medicare supplement plans.

Shares of insurance giant have outperformed the broader market over the past year. GL has gained 29.5% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 27.3%. In 2026, GL stock is up 10.5%, surpassing the SPX’s 9.6% rise on a YTD basis.

Zooming in further, GL’s outperformance is also apparent compared to the SPDR S&P Insurance ETF (KIE). The exchange-traded fund has declined about 3.2% over the past year. Moreover, GL’s low double-digit returns on a YTD basis outshine the ETF’s 6.5% losses over the same time frame.

Globe Life’s outperformance stemmed from growth in health premium revenue and double-digit NOI per share growth in seven of the last eight quarters, with CEO Frank Svoboda noting the model’s resilience despite economic pressure on working-class Americans. Looking ahead, management expects continued life and health premium growth. In addition, growth was fueled by Medicare supplement rate hikes and strong sales at United American and Family Heritage, while American Income saw higher agent productivity despite a temporary dip in headcount. The direct-to-consumer channel is lifting margins through higher-quality leads shared with agencies, and AI is being expanded across underwriting, distribution, and admin to boost efficiency. The company accelerated Q1 buybacks and plans to keep prioritizing share repurchases with excess cash after dividends.

On Apr. 22, GL shares closed up marginally after reporting its Q1 results. Its adjusted EPS of $3.43 did not meet Wall Street expectations of $3.46. The company’s revenue was $1.56 billion, missing Wall Street forecasts of $1.57 billion. GL expects full-year adjusted EPS in the range of $15.40 to $15.90.

For the current fiscal year, ending in December, analysts expect GL’s EPS to grow 7.2% to $15.56 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in two of the last four quarters while missing the forecast on two other occasions.

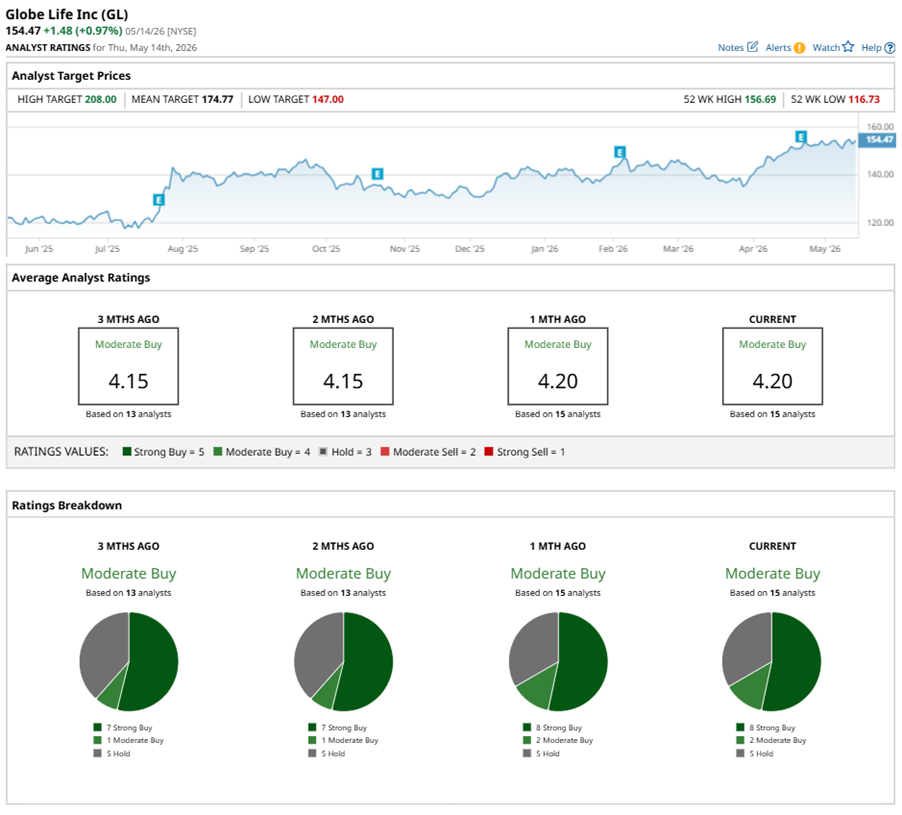

Among the 15 analysts covering GL stock, the consensus is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, two “Moderate Buys,” and five “Holds.”

This configuration is slightly more bullish than two months ago, with seven analysts suggesting a “Strong Buy.”

On Apr. 27, Keefe Bruyette analyst Ryan Krueger kept an “Outperform” rating on GL and raised the price target to $180, implying a potential upside of 16.5% from current levels.

The mean price target of $174.77 represents a 13.1% premium to GL’s current price levels. The Street-high price target of $208 suggests a notable upside potential of 34.7%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.