Farmington, Connecticut-based Otis Worldwide Corporation (OTIS) manufactures, installs, and services building systems. Valued at $28.1 billion by market cap, the company offers elevators, escalators, and other moving products.

Shares of elevator giant have underperformed the broader market over the past year. OTIS has declined 23.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 27.3%. In 2026, OTIS stock is down 16.4%, compared to the SPX’s 9.6% rise on a YTD basis.

Narrowing the focus, OTIS’ underperformance is also apparent compared to the State Street Industrial Select Sector SPDR ETF (XLI). The exchange-traded fund has gained about 24.1% over the past year. Moreover, the ETF’s 12.5% returns on a YTD basis outshine the stock’s losses over the same time frame.

On Apr. 22, OTIS shares closed down more than 1% after reporting its Q1 results. Its adjusted EPS of $0.89 fell short of Wall Street expectations of $0.91. The company’s revenue was $3.6 billion, topping Wall Street forecasts of $3.5 billion. OTIS expects full-year adjusted EPS in the range of $4.20 to $4.24, and revenue in the range of $15.1 billion to $15.3 billion.

For the current fiscal year, ending in December, analysts expect OTIS’ EPS to grow 3.5% to $4.19 on a diluted basis. The company’s earnings surprise history is mixed. It beat or matched the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

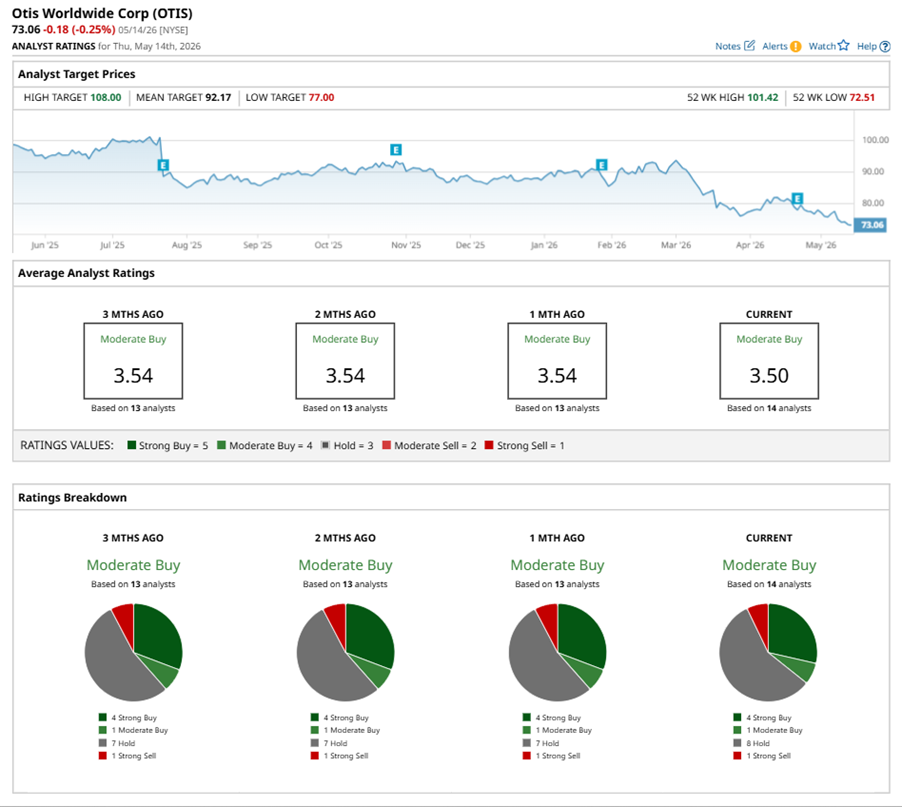

Among the 14 analysts covering OTIS stock, the consensus is a “Moderate Buy.” That’s based on four “Strong Buy” ratings, one “Moderate Buy,” eight “Holds,” and one “Strong Sell.”

The configuration has been relatively stable over the past three months.

On Apr. 24, Morgan Stanley (MS) kept an “Equal Weight” rating on OTIS and lowered the price target to $88, implying a potential upside of 20.4% from current levels.

The mean price target of $92.17 represents a 26.2% premium to OTIS’ current price levels. The Street-high price target of $108 suggests an ambitious upside potential of 47.8%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Marvell Technology Has a Hidden Growth Engine That Could Cause MRVL Stock to Skyrocket

- Salesforce Received a New $72 Million Contract From the U.S. Air Force. It’s Exciting, But Not a Game-Changer for CRM Stock.

- The $100 Million Reason Gemini Stock Is Up Today

- POET Stock Jumped on $500 Million Deal With Lumilens. Its Financials Have a Long Way to Go.