In a recent piece, I had highlighted how Morgan Stanley believes that the “exceptional” demand for memory chips will normalize, and consequently Nvidia (NVDA) will be the one to come out on the winning side because of this. Yet, even in a so-called normalized situation, the demand for memory chips will continue to grow. Agreed, the pace of growth may go through its own motions, subject to market cycles, but memory remains a crucial and undeniable component of the wider AI picture, keeping demand intact.

Financial services major BNP Paribas thinks the same as well. In a recent note to clients, the broker said, “Our analysis of CQ1 contract prices of 50+ [dynamic random access memory] SKUs and 75+ NAND SKUs leads us to estimate overall [dynamic random access memory average selling prices] can advance 90% Q/Q in CQ1, followed by a 6% Q/Q increase in CQ2 as increasing AI server demand is driving a wider supply-demand imbalance that’s exerting upward pricing pressure. For NAND, we estimate CQ1 prices could increase 55% Q/Q, followed by 5% Q/Q increase in CQ2 predominantly driven by supply-side dynamics as NAND suppliers continue to shift capacity to enterprise storage products while remaining prudent on capacity additions.”

Based on this analysis, BNP Paribas remains “Overweight” on Sandisk (SNDK) with a price target of $650, which implies an upside potential of 23% from current levels.

About Sandisk

Founded in 1988, Sandisk was, until recently, a niche name known only in the technology space for its memory prowess. However, as memory stocks went parabolic, Sandisk captured the imagination of a wide swath of the investing world. Established to commercialize flash memory storage technology, Sandisk is now a semiconductor storage company focused on NAND flash memory and solid-state storage solutions.

Valued at a market cap of $77.8 billion, SNDK stock is up a scarcely believable 921% over the past year.

Now, the bone of contention is whether Sandisk can keep this up or not. Truthfully, although BNP Paribas has made a case for investing in the stock, its opinion is based on short-term triggers. Has Sandisk got it in itself to be a bona fide wealth creator for years? Let's find out.

Financials Moving In The Right Direction

Sandisk has been in operation for less than a year in its current form after its spinoff from Western Digital (WDC). However, its results could not have been better in this period, with the bottom line surpassing estimates in each of the past four quarters. Notably, the results for the most recent quarter were blockbuster as well, with both revenue and earnings comfortably outpacing the consensus estimates.

Revenues for Q2 2026 stood at $3 billion, up 31% on a sequential basis. Revenues in the Edge segment, its largest and which focuses on its core specialty of flash memory and SSDs, went up by 21% in the same period to $1.7 billion. However, the fastest growth was experienced by the Datacenter segment, which soared by 64% quarter-over-quarter to $440 million.

Earnings, meanwhile, multiplied by more than five times quarterly to $6.20 per share. This was much above what the Street expected at $3.62 per share. Now, for Q3 2026, Sandisk expects EPS to be in the range of $12 to $14 per share. This would be a massive improvement from the year-ago period when the company reported a loss. On the other hand, revenues are forecasted to be between $4.40 and $4.80 billion, the midpoint of which would denote an annual growth rate of 170.6% on a year-over-year (YoY) basis.

Turning back to Q2 2026, net cash from operating activities for the quarter came in at $1 billion compared to just $95 million in the previous quarter, as Sandisk ended the quarter with a cash balance of $1.5 billion. This was much above its short-term debt levels of $20 million.

Additionally, the SNDK stock continues to trade at reasonable levels, too. While its forward P/E and P/CF of 13.24 and 15.13 are lower than the sector medians of 21.20 and 17.65, respectively, its forward P/S of 5.03 is not much higher than the sector median of 3.03.

Carving Its Own Memory In The Industry

Sandisk's spinoff from Western Digital could not have gone well, with the most stark evidence of that being the outsized rally in its share price. However, under the hood, it also marked a strategic pivot for the company to a pure-play NAND and SSD player, catapulting it to become a notable component in the AI infrastructure sector.

Delving deeper into its focus on NAND, Sandisk's message clarity to the market has boded well for the company. Enterprise customers, primarily LLM developers, prefer NAND memory for its long-term storage capabilities and non-volatile nature, meaning it keeps your data even when the power is turned off. Also, Sandisk's focused business model, centered on memory and storage rather than full-scale chip fabrication, keeps capital expenditure relatively low and avoids the all-or-nothing risks that pure-play manufacturers often face.

Additionally, the company's growth trajectory is supported by the ongoing increase in NAND content per device, a trend accelerated by the shift toward edge AI and decentralized inference. Chip designers are actively seeking ways to cut reliance on costly, power-hungry DRAM, turning instead to NAND for many storage-intensive workloads. The rise of edge AI further amplifies this tailwind, as more processing moves from centralized cloud servers to local devices and systems.

Notably, to keep pace with demand, Sandisk has deepened its long-standing collaboration with Kioxia (KXIAY). The recently extended joint venture includes a commitment from Sandisk to pay Kioxia $1.17 billion for additional manufacturing services, spread across annual installments from 2026 to 2029. This arrangement secures incremental greenfield capacity without requiring Sandisk to bear the full burden of new fab construction.

Looking to 2026, Sandisk's strongest competitive advantage appears in the ultra-high-capacity segment, particularly for AI data centers. While competitors such as Micron (MU) and SK Hynix have concentrated on high-bandwidth memory (HBM), Sandisk has established clear leadership in high-density enterprise SSDs (eSSDs). Its newly introduced 256TB UltraQLC NVMe SSD, built on BiCS8 QLC NAND, nearly doubles the capacity of Micron's 128TB offerings. The BiCS8 technology employs a CMOS Bonded to Array (CBA) architecture that enables industry-leading 4.8 Gb/s I/O speeds as of early 2026, along with roughly 30% lower power consumption compared with Samsung's conventional monolithic designs. These performance characteristics position Sandisk favorably in the high-margin, performance-critical segments of the AI storage market.

Analyst Opinion of SNDK Stock

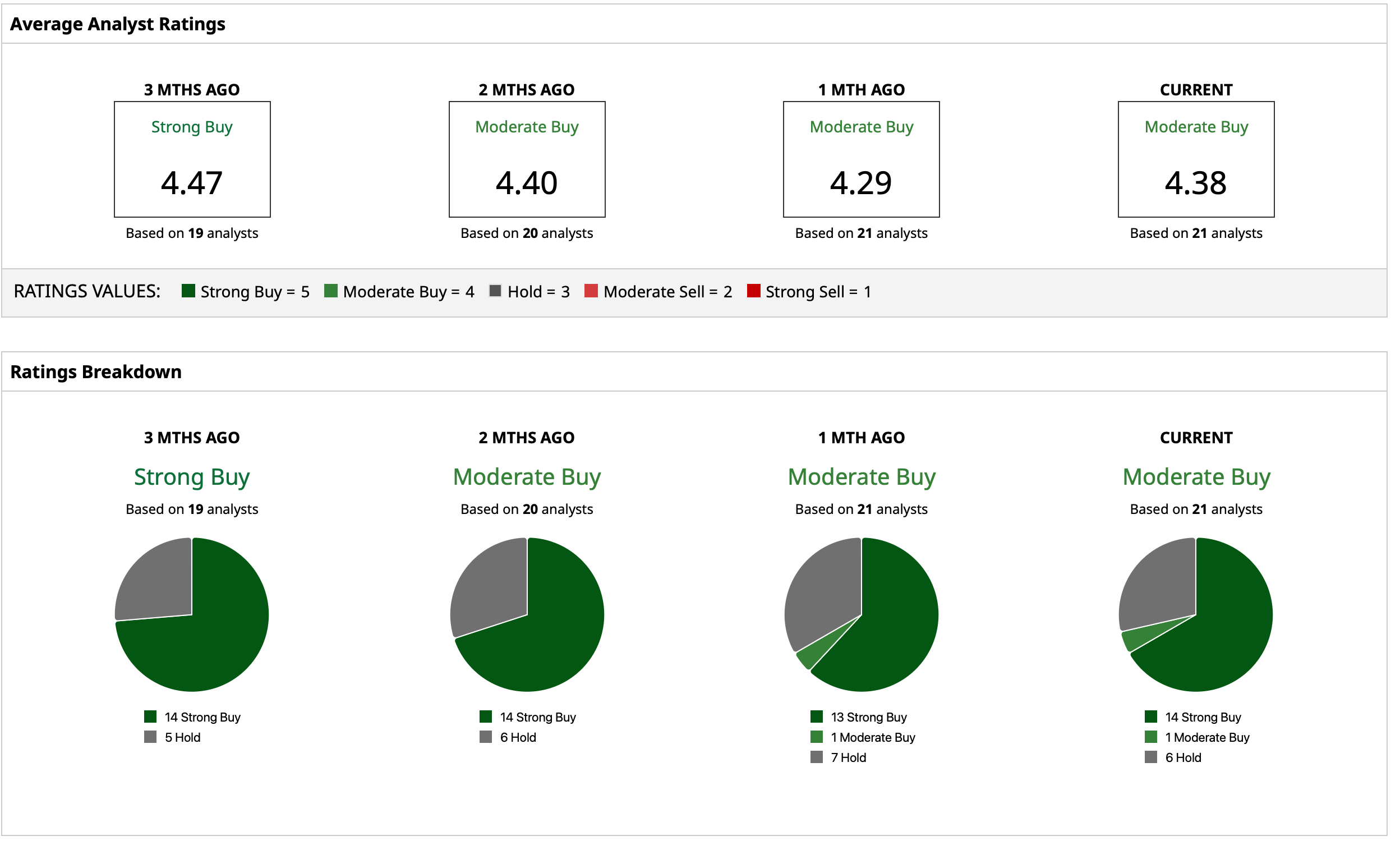

Taking all of this into account, analysts have deemed SNDK stock a consensus “Moderate Buy,” with a mean target price of $700.94. This indicates an upside potential of about 32% from current levels. Out of 21 analysts covering the stock, 14 have a “Strong Buy” rating, one has a “Moderate Buy” rating, and six have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Drone Contract Wins Are Sending Red Cat Stock Higher. Should You Buy RCAT Here?

- This Software Stock Is Shrugging Off Apocalypse Fears. Should You Chase the Rally Here?

- Berkshire Hathaway Is Buying Back Stock. Why That’s a Key Signal for Investors to Watch Now.

- Palantir Stock Up 17% in 1 Month as Iran Tensions Ignite Defense AI Boom