The war in Iran and rising oil prices are driving up pump prices. The problem is that oil is an integral part of transportation, manufacturing, and other essential parts of the economy; it helps keep everything moving.

While inconvenient, it certainly raises a question about energy stocks and whether now is the right time to cycle in. And when investors look for big names in the sector, Exxon Mobil and Chevron are usually at the top of the list. Both are oil giants, but their approach is somewhat different. But how different, exactly? And how does that difference factor into which stock is a better choice for income investors?

Let’s find out.

Exxon Mobil (XOM)

First is Exxon Mobil, the larger of the two companies. It operates in oil production, refining, and chemicals, giving it one of the strongest footholds in the energy market. With a market cap of around $656 billion, it is one of the biggest energy companies in the world.

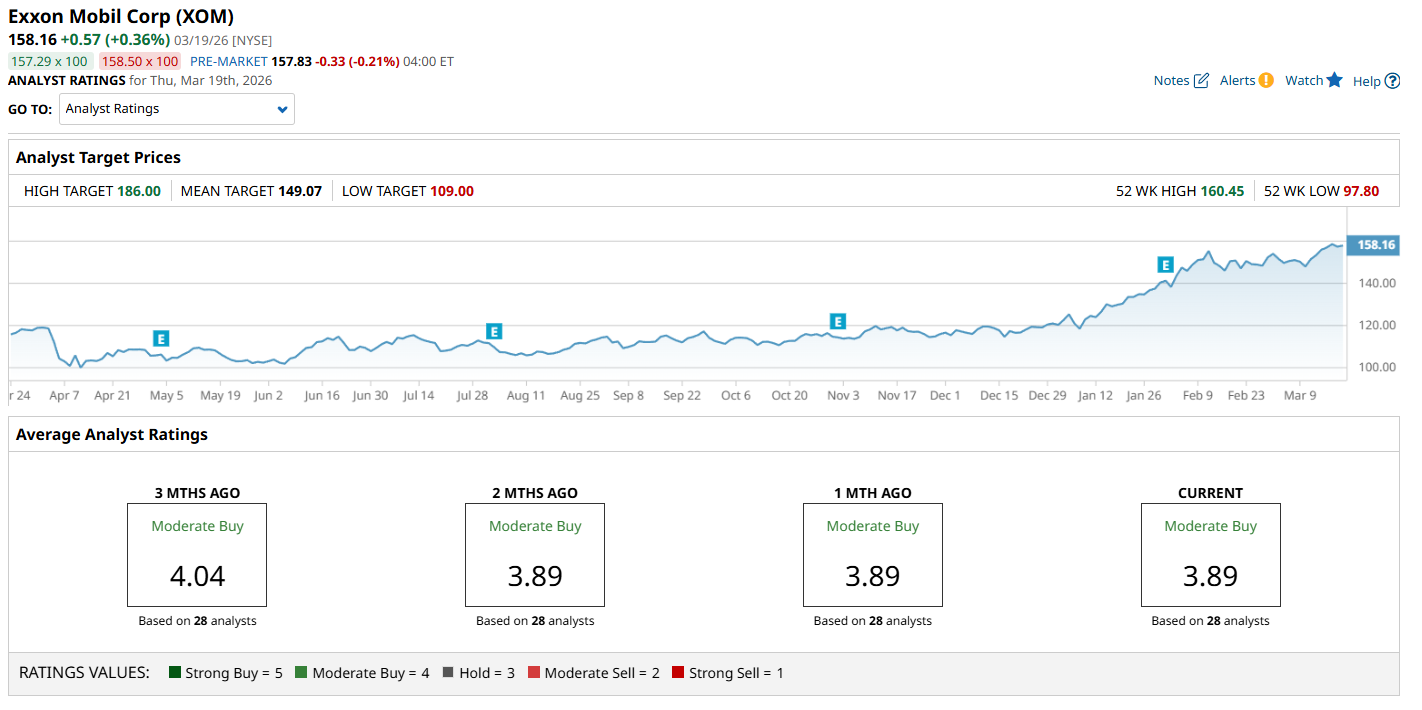

ExxonMobil stock is trading at approximately $158, and it is up nearly 37% year-to-date.

Chevron (CVX)

Second is Chevron, nearly half the size of its rival, but still one of the most recognizable names in the sector. Like Exxon Mobil, it operates in oil and gas production and refining. With a market cap of around $396 billion, Chevron remains one of the largest energy companies in the world.

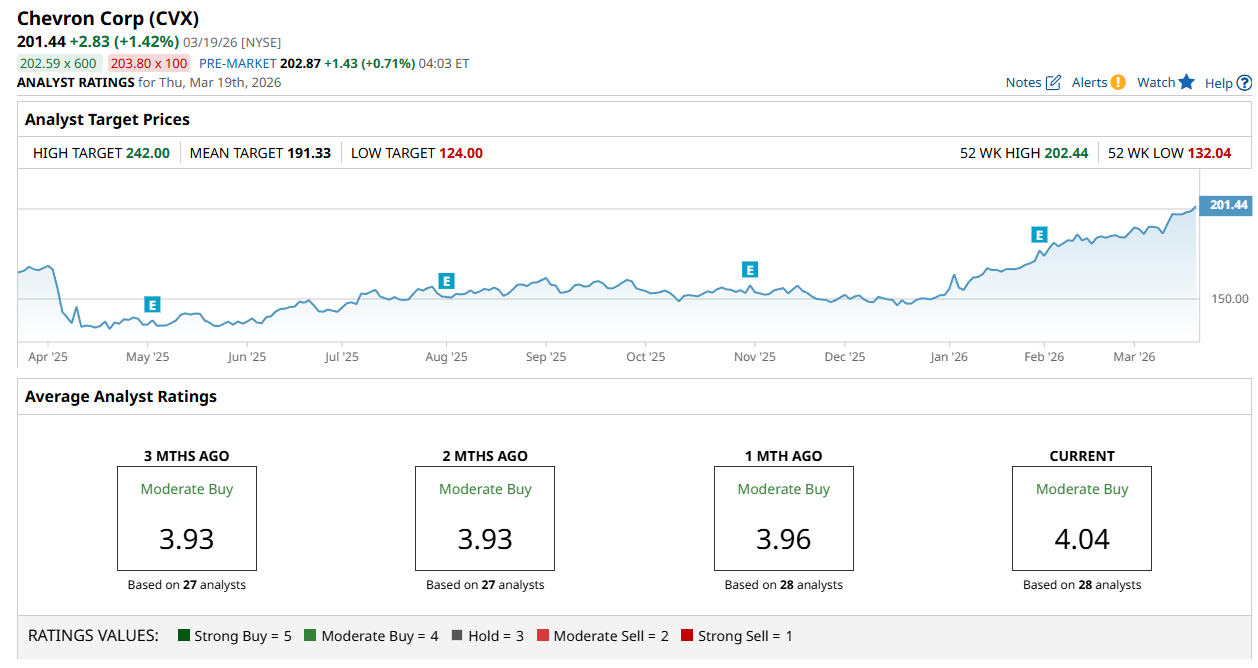

Chevron stock is trading at about $201, and it is up roughly 32% year to date.

Business model comparison: Exxon vs Chevron

Exxon makes money from producing oil and gas, refining crude into fuels and other products, and selling petrochemicals. It has a great presence on the value energy chain, which makes its positioning more balanced. So in short, Exxon produces, processes, and sells oil-based products.

Meanwhile, Chevron is very similar, but with a slightly different emphasis. It also produces oil and gas and operates in refining, but its business is generally more centered on production than Exxon's. This difference gives Chevron a somewhat simpler setup while also tying it more closely to the ups and downs of oil and gas prices.

Put simply, Exxon looks more balanced across the energy chain, while Chevron is more closely tied to production.

How these two energy giants stack up financially

Here’s what the numbers look like based on their latest financial reports:

| Metric (Latest quarter) | Exxon Mobil | Chevron |

| Sales | $82.3 billion | $46.9 billion |

| Net Income | $6.5 billion | $2.8 billion |

| Operating Cash Flow | $52.0 billion | $33.9 billion |

| Forward Price/Earnings (P/E) | 22.54 | 27.32 |

Right away, last quarter, we can see Exxon has more sales, coming in at $82.3 billion, well ahead of Chevron’s $46.9 billion. Not only that, but net income is also higher for Exxon at $6.5 billion versus Chevron’s $2.8 billion.

Cash flow tells pretty much the same story. Operating cash flow, a metric that tells how much cash a company generates from its core business operations, favors Exxon with roughly $52 billion, compared with Chevron’s $33.9 billion.

Now let's talk valuation. The price-to-earnings ratio, or P/E, compares a company’s stock price with its earnings, helping investors decide whether a stock is expensive, cheap, or reasonably priced. Lower is generally better, but it only really means something when compared with the broader sector.

The energy sector has a median forward P/E of around 16. As a result, both stocks look expensive based on that metric, though Exxon looks a bit cheaper than Chevron. This may be because investors are willing to pay a premium now, expecting solid performance going forward.

Overall, if you are looking for the better value play between the two, Exxon appears to be the better buy because it has a lower P/E ratio and stronger results across sales, earnings, and cash flow.

Dividend comparison

For income-focused investors, this is what you might be waiting for.

Exxon pays a forward annual dividend of $4.12, translating to a yield of around 2.6%. It has a dividend payout ratio of 56%, meaning it pays out only 56% of its earnings to shareholders. The company has increased dividends for 43 consecutive years, and payouts have increased 15% over the last five years.

Meanwhile, Chevron pays $7.12 yearly, translating to an approximate 3.5% yield. That’s almost 1% higher than Exxon. Chevron has also increased its dividend for 39 consecutive years and boasts a higher 5-year increase at 33%. However, all this comes with an astronomically high dividend payout ratio of 95%.

Based on the dividend data, I’m leaning more towards Exxon as it has far more room to grow the dividend in the future. The yield and growth are lower, yes, but the company has a much bigger headroom to continue and increase its dividends more reliably.

What does Wall Street say?

So, how does Wall Street rate these stocks?

A consensus among 28 analysts rates Exxon a Moderate Buy” with an average score of 3.89 out of 5. The $186 high target price suggests up to 18% potential upside.

On the other hand, a consensus of the same number of analysts rates Chevron a “Moderate Buy,” with a slightly higher average score of 4.04. The high target price of $242 suggests a 20% upside potential.

Verdict: Exxon vs Chevron

When all is said and done, both Exxon and Chevron look like solid picks in the energy sector. And frankly, the better stock depends on what matters more to you.

Exxon stands out for its larger scale, stronger financial results, and a better ability to grow its dividend in the future. It also has a broader business mix, which gives it a more balanced setup across different parts of the energy market. Meanwhile, Chevron could look better to investors who place a greater premium on higher yield today, at the expense of reduced dividend growth in the future.

On the date of publication, Rick Orford did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart