Aluminum has quietly become one of the more geopolitically sensitive industrial commodities. When shipping lanes are in danger, prices and regional premiums can sprint higher. Traders are already paying higher prices for metals, as concerns about Middle East supply-chain disruptions shift the risk calculus for global manufacturers.

That dynamic helps explain why Alcoa (AA) and Century Aluminum (CENX) are drawing fresh investor attention. Both names sit squarely in the path of any rally triggered by tighter seaborne flows. Fears that the Strait of Hormuz could see continued disruptions, after reported incidents near facilities run by Emirates Global Aluminium and Aluminium Bahrain, helped push aluminum futures higher on the London Metal Exchange.

News outlets such as Bloomberg and analyst notes from Citi warn that regional disruptions could reshuffle flows, a setup that could create a buying opportunity in AA and CENX for risk-tolerant investors.

Alcoa Corporation (AA)

Alcoa is a major U.S. aluminum producer. Rising U.S.-Iran tensions have threatened the Strait of Hormuz shipping lane, prompting a surge in aluminum futures. If Middle Eastern output is disrupted, higher metal prices could potentially benefit Alcoa’s shares.

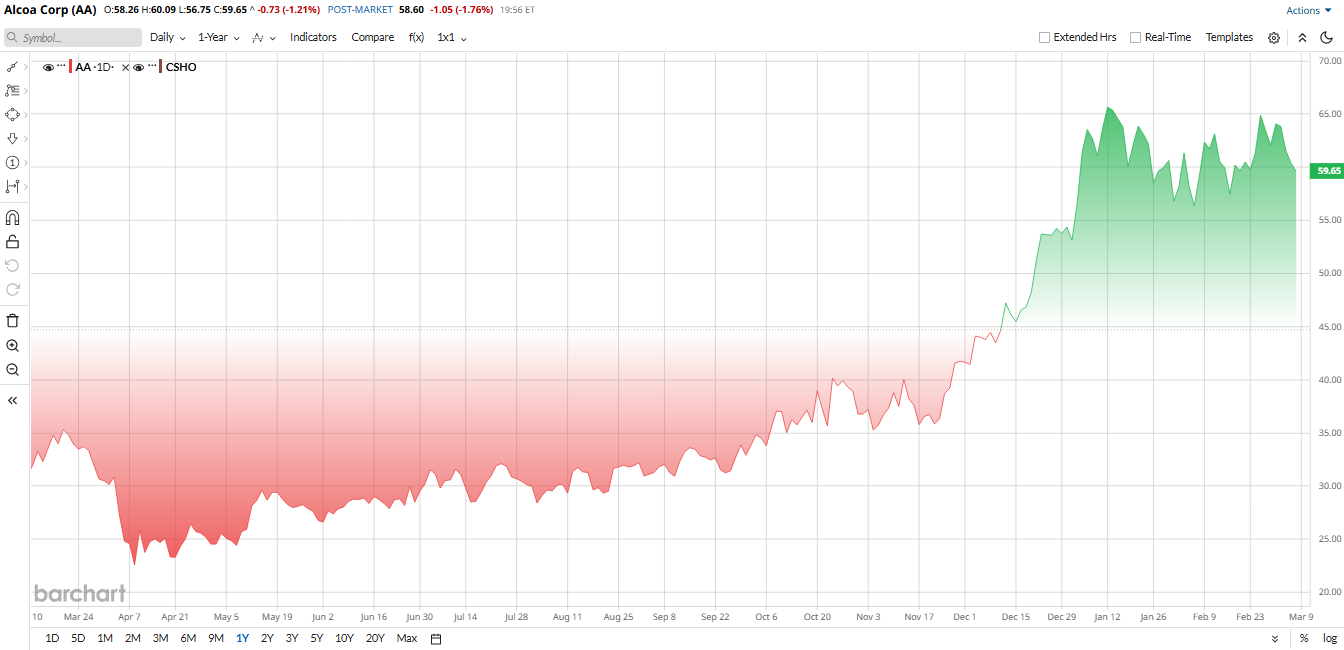

Valued at a market cap of about $16 billion, AA’s stock has rallied strongly, trading in the mid-to-low-$60s versus the low-$20s a year ago on booming aluminum prices and U.S. regional premiums. The Iran war and higher tariffs have driven much of this rally, pushing the stock up roughly 97% over the past year.

For income-focused investors, Alcoa currently offers a forward dividend yield of about 0.67%, paying $0.10 per share quarterly, with a low 10.6% payout ratio that suggests the company prioritizes reinvesting cash into growth and defense technology.

On the valuation side, Barchart data said Alcoa’s forward price-to-earnings (P/E) is about 11.4x, well below the sector median of 25x, indicating a relatively cheap valuation. However, the price-to-book ratio of 2.5x is just slightly below the sector median of 2.6x. Analysts warn the stock looks “expensive” given its growth outlook, implying only limited upside without continued price support.

Operational performance has also supported investor interest. In Q4 2025, Alcoa posted $3.45 billion in revenue, up 15% sequentially. GAAP net income was $226 million, and adjusted net income came to $1.26 per share, well above estimates. Stronger realized aluminum prices lifted the aluminum segment sales by 21%, more than offsetting higher U.S. tariffs. Plus, the company generated about $537 million in operating cash, versus $66 million in Q3. It ended Q4 with $1.6 billion in cash. Notably, Alcoa set production records at several smelters and closed strategic deals, such as selling its Saudi JV stake, during the quarter.

Beyond the numbers, Alcoa is making investments in its operations. In late 2025, it secured a 10-year power contract with New York’s grid operator and announced a $60 million upgrade to its smelter in Massena, New York. This deal delivers 240 MW of cheap renewable energy and a modernized anode furnace, which should lower Alcoa’s future energy costs and support higher output.

Looking ahead, Analysts expect Alcoa’s next quarter (Q1) to show roughly flat revenue and modest earnings per share (EPS) growth, assuming current metal prices hold. Seasonal factors and the ramp-up of new projects imply only moderate growth. Consensus calls for breakeven sales and slightly higher margins year-over-year.

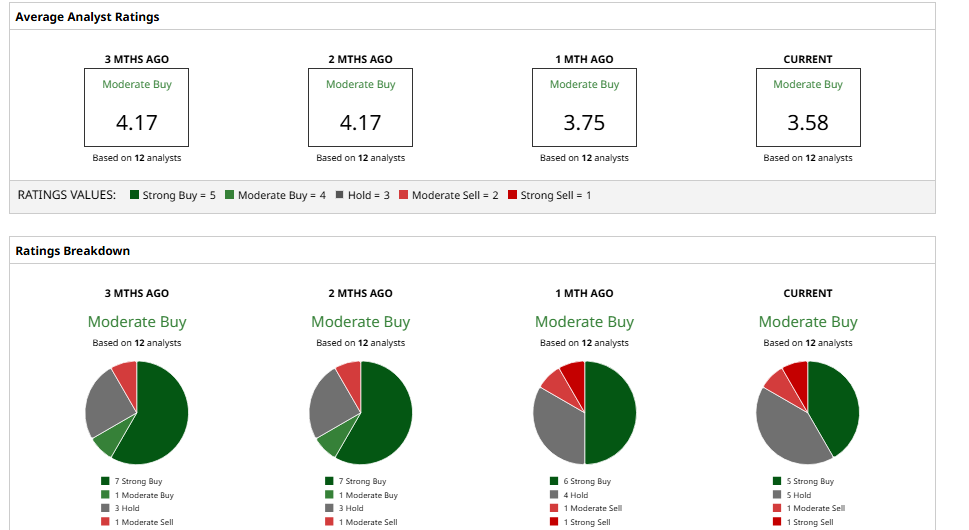

Barchart’s consensus rating on AA is “Moderate Buy.” The average 12-month price target is about $60.18, which implies limited upside.

From my perspective, Alcoa is viewed as an opportunity as it offers a hedge on supply disruptions, but the valuation leaves little margin without a fresh spike in metal prices.

Century Aluminum (CENX)

Century Aluminum operates several U.S. smelters. The same supply concerns that have driven aluminum prices higher are bullish for Century. For example, aluminum futures recently jumped 1.7% to multi-month highs on March 2, as the Iran conflict threatened exports through the Strait of Hormuz.

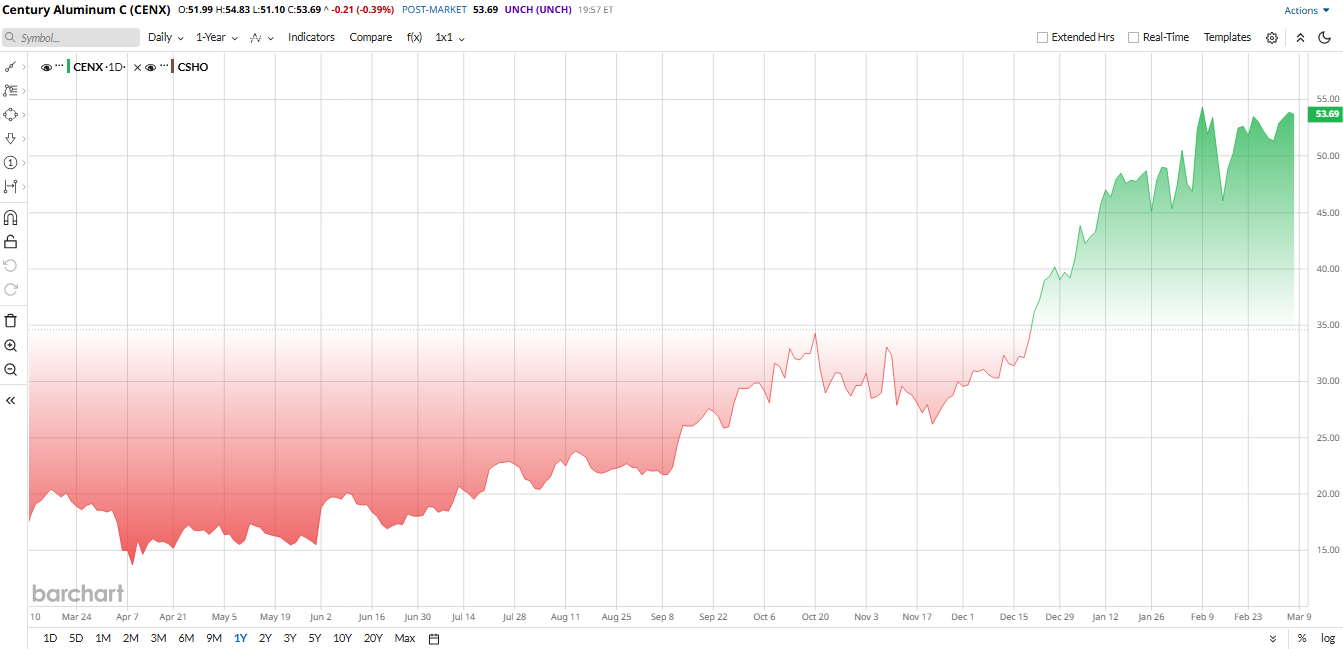

Just like Alcoa, CENX stock has enjoyed a historic rally. It’s trading just slightly below $54, up from $13 a year ago, and it is currently up more than 220% over the past year, driven by surging aluminum prices and higher U.S. premiums amid tight supply. That sharp rise is also supported by the improved profitability of aluminum producers over the last year.

Despite the strong rally, valuation metrics still appear relatively favorable. Century’s valuation remains attractive after the rally. CENX’s forward P/E is only 7.9x as of now, far below the industry median of 13.9x. In other words, the stock is trading on depressed current earnings, implying room for upside if profits rebound.

In Q4 2025, Century generated $633.7 million in sales and net income of just $1.8 million, or $0.02 per share, which was a sharp sequential improvement. Shipments fell 14% due to an Iceland smelter outage, yet higher aluminum prices and premiums kept revenue roughly flat. The company ended the quarter with $134 million in cash and $418 million in total liquidity, leaving a strong financial base for expansion.

Century is also expanding capacity as part of its longer-term strategy. In January 2026, it announced a JV with Emirates Global Aluminium to build a new U.S. smelter in Oklahoma, the first greenfield project since 1980. It also agreed to sell its idled smelter in Hawesville, Kentucky, and restart 50,000 metric tons at its Mt. Holly, South Carolina, plant by mid-2026. These moves significantly boost long-term output.

Looking forward, analysts expect a robust Q1 2026. Management guided Q1 adjusted EBITDA of about $215 million to 235 million, implying strong year-over-year growth. Consensus forecasts high-single-digit to double-digit revenue and EPS gains, assuming aluminum prices hold at current levels. In other words, street estimates call for continued profit growth as new capacity comes online.

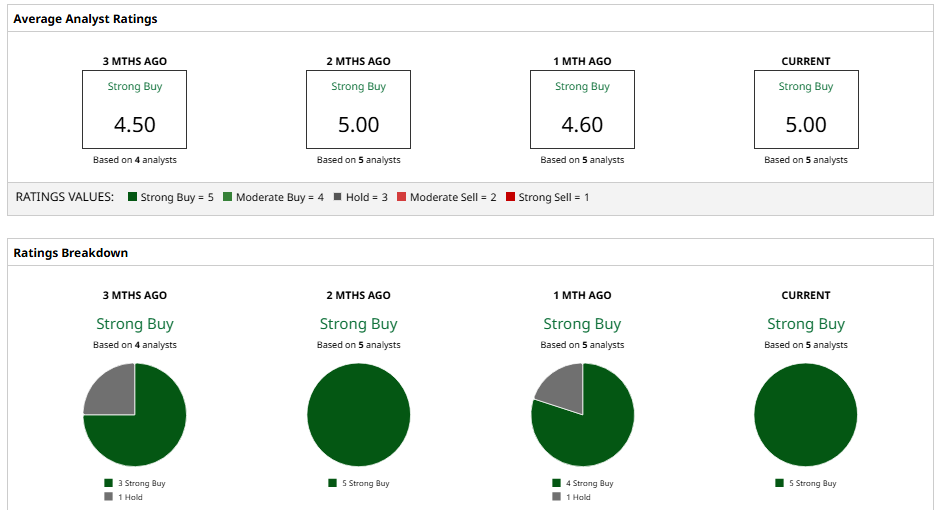

Analysts are generally bullish, expecting 2026 earnings well above last year’s levels, thanks to higher metal prices and these capacity catalysts. Among Wall Street analysts covering the stock, CENX has a unanimous “Strong Buy” rating, with the average 12-month target price sitting at roughly $63, implying about 18% upside.

In my opinion, Century is seen as a growth play on the aluminum rally. At its low valuation and with significant expansion projects underway, the stock has substantial upside potential if U.S.-Iran tensions keep prices elevated.

On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The ‘Flight to Quality’ Isn’t Working as the S&P 500 Stalls Out. This ETF Shows Why.

- A $30 Million Reason to Buy Penny Stock Longeveron Today

- Warren Buffett Told New CEO Greg Abel ‘Once You Start Fooling Your Shareholders, You Will Soon Believe Your Own Baloney.’ What Did Abel Tell Shareholders About Q4?

- This Esports ETF Is Trying to Make an Epic Comeback. Should You Play the Game Here?