Headquartered in Monett, Missouri, Jack Henry & Associates, Inc. (JKHY) is a financial technology company serving banks and credit unions. Commanding a market cap of approximately $11.5 billion, the company delivers core processing platforms that manage deposits, loans, and customer data.

It also enables secure payments across Automated Teller Machine (ATM), cards, Automated Clearing House (ACH), and mobile bill pay channels, while strengthening digital banking, treasury, fraud prevention, and integrated lending solutions.

Over the past 52 weeks, JKHY stock has declined 5.6%, while the S&P 500 Index ($SPX) gained nearly 13% in the same stretch. Year-to-date (YTD), the stock has fallen 12.8%, whereas the broader index managed a marginal uptick.

When we widen the lens, the comparison grows more nuanced. The Global X FinTech ETF (FINX) has dropped 27.1% over the past 52 weeks and slid 19.1% YTD. Against that backdrop, JKHY’s pullback looks far less severe.

Momentum shifted sharply after earnings. The stock climbed 4.6% on Feb. 4, just a day after management reported Q2 fiscal 2026 results, wherein revenue increased 7.9% year over year to $619.3 million, surpassing the Street’s $609.4 million estimate. Meanwhile, EPS jumped 28.6% to $1.72, comfortably ahead of the projected $1.43.

Building on this, management reinforced the optimism with upgraded guidance. The company has lifted its full-year GAAP revenue growth to a range of 5.6% to 6.3% and expects GAAP EPS of $6.61 to $6.72, reflecting growth of 6% to 8%.

For fiscal year 2026, ending in June, analysts expect diluted EPS to rise 5.3% year over year to $6.57, reflecting steady earnings momentum. Importantly, Jack Henry has topped EPS estimates in each of the past four quarters, reinforcing confidence in its execution and forward visibility.

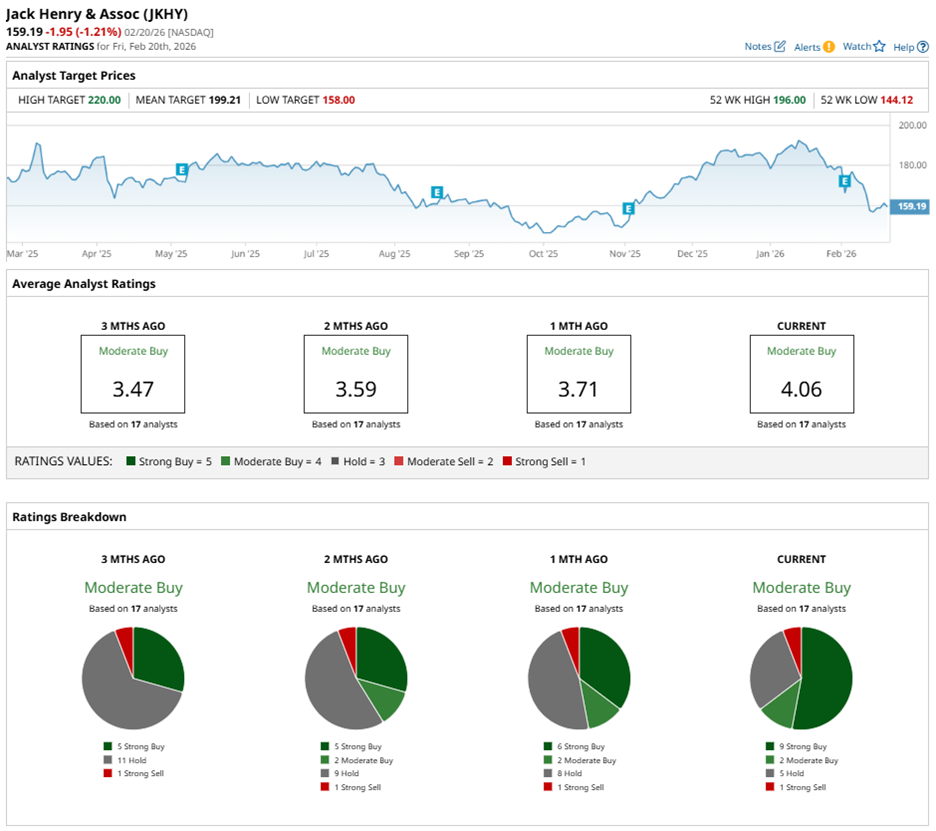

Wall Street currently assigns JKHY stock an overall rating of “Moderate Buy.” Among 17 analysts covering the stock, nine recommend “Strong Buy,” two suggest “Moderate Buy,” five advise “Hold,” while one has flagged a “Strong Sell.”

Analyst sentiment has largely improved from three months ago, when five analysts assigned “Strong Buy” ratings to JKHY stock.

Analyst backing has remained firm and deliberate. On Feb. 4, DA Davidson analyst Peter Heckmann reiterated his “Buy” rating and held his $216 price target steady. Only days earlier, on Jan. 29, he had reaffirmed the same rating while raising the target from $190 to $216. Such sequential reinforcement underscores sustained confidence in long-term growth.

Price targets continue to suggest untapped potential. The mean price target of $199.21 implies potential upside of 25.1%, while the Street-high target of $220 represents a gain of 38.2% from current levels.

On the date of publication, Aanchal Sugandh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart