Wrapping up Q1 earnings, we look at the numbers and key takeaways for the hardware & infrastructure stocks, including Super Micro (NASDAQ: SMCI) and its peers.

The Hardware & Infrastructure sector will be buoyed by demand related to AI adoption, cloud computing expansion, and the need for more efficient data storage and processing solutions. Companies with tech offerings such as servers, switches, and storage solutions are well-positioned in our new hybrid working and IT world. On the other hand, headwinds include ongoing supply chain disruptions, rising component costs, and intensifying competition from cloud-native and hyperscale providers reducing reliance on traditional hardware. Additionally, regulatory scrutiny over data sovereignty, cybersecurity standards, and environmental sustainability in hardware manufacturing could increase compliance costs.

The 9 hardware & infrastructure stocks we track reported a very strong Q1. As a group, revenues beat analysts’ consensus estimates by 7.3% while next quarter’s revenue guidance was in line.

Luckily, hardware & infrastructure stocks have performed well with share prices up 26.3% on average since the latest earnings results.

Super Micro (NASDAQ: SMCI)

Founded in Silicon Valley in 1993 and known for its modular "building block" approach to server design, Super Micro Computer (NASDAQ: SMCI) designs and manufactures high-performance, energy-efficient server and storage systems for data centers, cloud computing, AI, and edge computing applications.

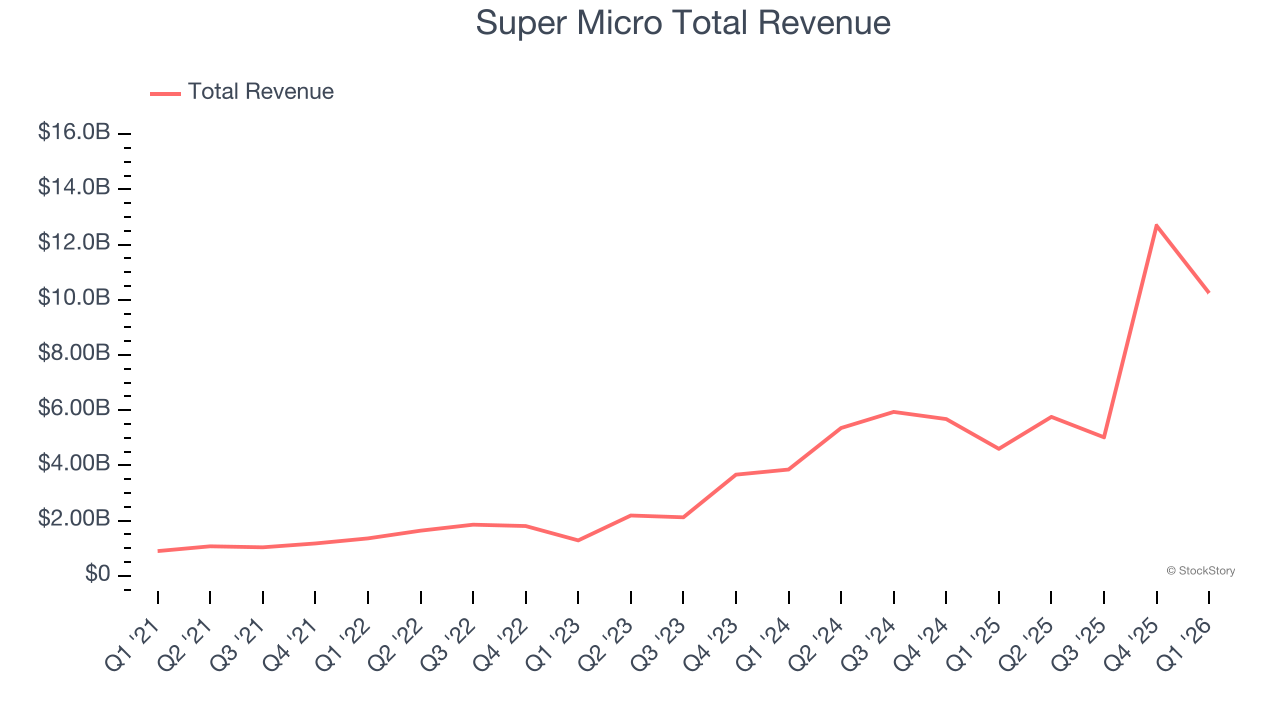

Super Micro reported revenues of $10.24 billion, up 123% year on year. This print fell short of analysts’ expectations by 17.3%, but it was still a strong quarter for the company with a beat of analysts’ EPS estimates.

Super Micro pulled off the highest full-year guidance raise but had the weakest performance against analyst estimates of the whole group. Unsurprisingly, the stock is up 57.1% since reporting and currently trades at $43.73.

Best Q1: Dell (NYSE: DELL)

Founded by Michael Dell in his University of Texas dorm room in 1984 with just $1,000, Dell Technologies (NYSE: DELL) provides hardware, software, and services that help organizations build their IT infrastructure, manage cloud environments, and enable digital transformation.

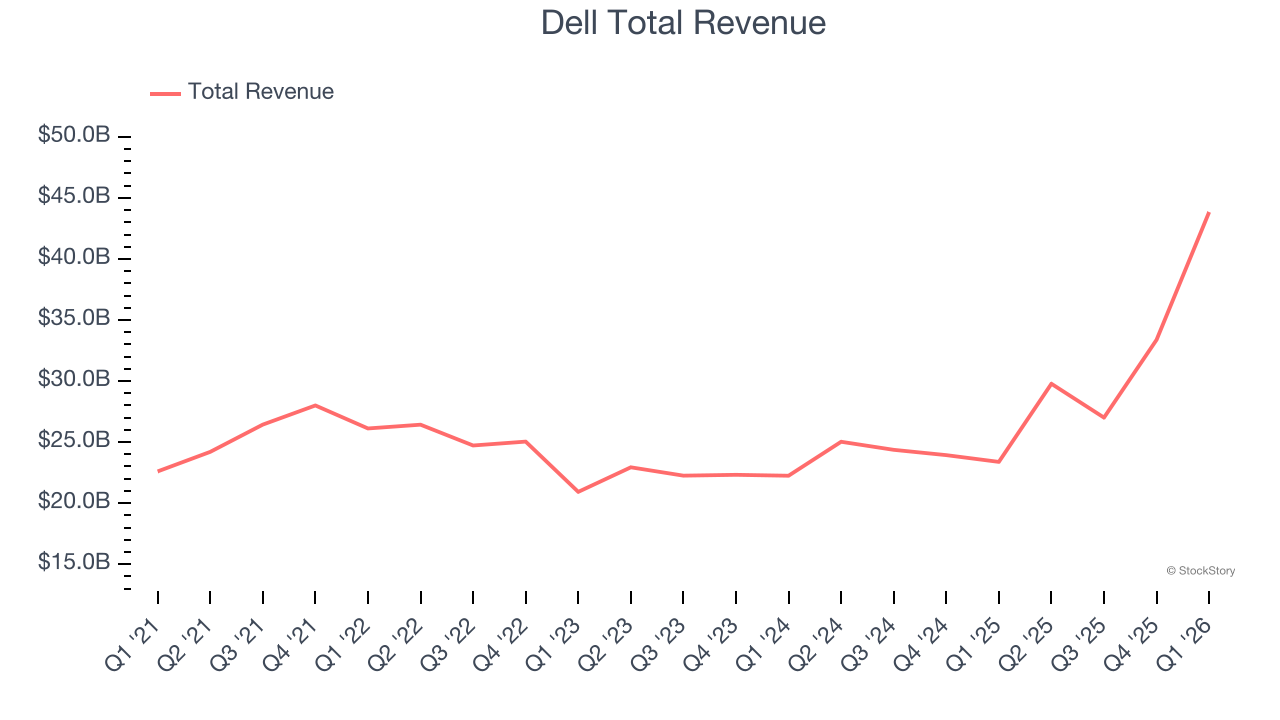

Dell reported revenues of $43.84 billion, up 87.5% year on year, outperforming analysts’ expectations by 21.5%. The business had an incredible quarter with a beat of analysts’ EPS estimates.

The market seems happy with the results as the stock is up 25.5% since reporting. It currently trades at $397.96.

Is now the time to buy Dell? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Xerox (NASDAQ: XRX)

Pioneering the modern office copier and inventing technologies like Ethernet and the laser printer, Xerox (NASDAQ: XRX) provides document management systems, printing technology, and workplace solutions to businesses of all sizes across the globe.

Xerox reported revenues of $1.85 billion, up 26.7% year on year, exceeding analysts’ expectations by 6.6%. Still, it was a slower quarter as it posted a significant miss of analysts’ EPS estimates and full-year revenue guidance slightly missing analysts’ expectations.

Interestingly, the stock is up 127% since the results and currently trades at $3.56.

Read our full analysis of Xerox’s results here.

Everpure (NYSE: P)

Founded in 2009 as a pioneer in enterprise all-flash storage technology, Everpure (NYSE: P) provides all-flash data storage hardware and software that helps organizations manage their data more efficiently across on-premises and cloud environments.

Everpure reported revenues of $1.05 billion, up 35.2% year on year. This result surpassed analysts’ expectations by 5%. It was a stunning quarter as it also put up a solid beat of analysts’ billings and EPS estimates.

The stock is down 13.9% since reporting and currently trades at $73.80.

Read our full, actionable report on Everpure here, it’s free.

Diebold Nixdorf (NYSE: DBD)

With roots dating back to 1859 and a presence in over 100 countries, Diebold Nixdorf (NYSE: DBD) provides automated self-service technology, software, and services that help banks and retailers digitize their customer transactions.

Diebold Nixdorf reported revenues of $888.2 million, up 5.6% year on year. This print topped analysts’ expectations by 3.5%. Overall, it was a strong quarter as it also logged a solid beat of analysts’ revenue and EPS estimates.

Diebold Nixdorf had the slowest revenue growth among its peers. The stock is down 2% since reporting and currently trades at $81.30.

Read our full, actionable report on Diebold Nixdorf here, it’s free.

Market Update

Late in 2025 into early 2026, there was hand-wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.