United Rentals, Inc. (NYSE: URI) today provided an update on the company’s response to the ongoing coronavirus pandemic ("COVID-19") and announced financial results for the first quarter of 2020.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20200429005845/en/

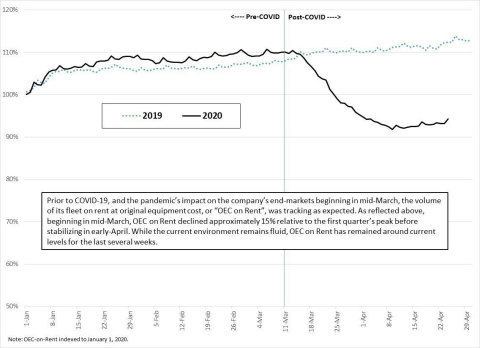

Year-to-date indexed OEC on Rent trends through April 24: 2020 vs. 2019* Source: Company data.

Update on Business Response to COVID-19

Prior to mid-March, the company’s first quarter performance was largely in line with its expectations. In early-March, the company initiated contingency planning ahead of the impact of COVID-19 on its end-markets. This planning has focused on five key work-streams that are the basis for the company’s crisis response plan:

- Ensuring employee safety and well-being: Above all else, United Rentals is committed to ensuring the health, safety and well-being of its employees and customers. The company has implemented a variety of COVID-19 safety measures, including ensuring that branches have sufficient and adequate personal protection equipment. The company has also implemented appropriate social distancing practices, and increased disinfecting of equipment and facilities.

- Leveraging its competitive advantages to support the needs of customers: All branches in the U.S. and Canada remain open to provide essential services, with seven of its 11 European branches also operating. The company has made modifications to enhance safety measures in its operating processes and protocols that support the needs of its customers. Additionally, the company’s digital capabilities allow customers to perform fully contactless transactions.

- Disciplined capital expenditures: The company has a substantial degree of flexibility in managing its capital expenditures and fleet capacity. While the current environment remains fluid, the company expects that its 2020 capital expenditures will be down significantly year-over-year.

- Controlling core operating expenses: A significant portion of the company’s cash operating costs are variable in nature. Since March, the company has significantly reduced overtime and temporary labor primarily in response to the impact of COVID-19. Furthermore, the company continues to leverage its current capacity to reduce the need for third-party delivery and repair services, and minimize discretionary expenses across general and administrative areas.

- Proactively managing the balance sheet with a focus on liquidity: The company is focused on ensuring that it maintains ample liquidity to meet its business needs as the impact of COVID-19 evolves. As a result, its share repurchase program was paused in mid-March. At March 31, 2020, total liquidity was $3.083 billion, including $513 million in cash and cash equivalents. Additionally, the company has no long-term debt maturities until 2025.

CEO Comment

Matthew Flannery, chief executive officer of United Rentals, said, “I’m incredibly proud of the way our team has responded to the COVID-19 crisis, and I want to thank them for their extraordinary efforts during this challenging period. Our highest priority is to ensure the safety of our employees and customers in our workplaces and at jobsites. The modifications we’ve made to our operating protocols preserve our ability to serve the needs of thousands of communities, while retaining critical capacity for the return of end-market demand.”

Flannery continued, “Our business tracked as we expected through early March, when the outlook for 2020 became far more uncertain due to the pandemic. While we’ve withdrawn our guidance at this time, we're confident in our ability to leverage the resiliency inherent in our business model. We’re in the strongest position in our history to respond to this crisis and to prepare for the recovery to come. This includes the strength of our balance sheet and cash flow, as we remain focused on disciplined capital allocation and cost management. We expect our free cash flow to remain substantially positive in 2020, even in our worst-case scenarios.”

Summary of First Quarter 2020 Financial Results

Total revenue increased 0.4% to $2.125 billion and rental revenue decreased 0.7% to $1.783 billion. On a GAAP basis, the company reported net income of $173 million, or $2.33 per diluted share ("EPS"), compared with $175 million, or $2.19 per diluted share, for the same period in 2019. Diluted EPS for the quarter increased 6.4% year-over-year, and adjusted EPS1 increased 1.2% year-over-year to $3.35.

Adjusted EBITDA1 decreased 0.7% year-over-year to $915 million, while adjusted EBITDA margin decreased 40 basis points to 43.1%.

- Rental revenue2 was $1.783 billion, reflecting a decrease of 0.7% year-over-year. COVID-19 began to impact the company's operations in March. Through February, rental revenue was up slightly year-over-year. In March, rental revenue decreased year-over-year, primarily due to the impact of COVID-19.

- Fleet productivity3 decreased 1.2% year-over-year, primarily due to the impact of COVID-19 in March, when rental volume declined in response to shelter-in-place orders and other end-market restrictions. Through February, fleet productivity was flat year-over-year and in line with expectations.

- Used equipment sales in the quarter generated $208 million of proceeds at a GAAP gross margin of 39.9% and an adjusted gross margin of 45.7%4; this compares with $192 million at a GAAP gross margin of 34.9% and an adjusted gross margin of 49.0% for the same period last year. The year-over-year increase in GAAP gross margin primarily reflects lower margin 2019 sales of fleet acquired in the acquisition of Vander Holding Corporation and its subsidiaries (“BlueLine”). The year-over-year decrease in adjusted gross margin was primarily due to changes in the mix of equipment sold, channel mix and pricing.

- General rentals segment had a 2.0% year-over-year decrease in rental revenue. Rental gross margin decreased by 310 basis points to 32.1%, with 260 basis points of the decline due to increased depreciation expense. Higher depreciation expense in the first quarter was primarily due to a $24 million, non-cash asset impairment charge, which was not related to COVID-19. The remaining 50 basis point decline in rental gross margin was primarily due to certain operating costs that increased as a percentage of revenue. Rental revenue declined primarily due to COVID-19.

- Specialty rentals segment, or Trench, Power and Fluid Solutions, generated increased rental revenue of 4.6% year-over-year, including an organic increase of 2.8%. The segment's increase in rental revenue reflected a 9.8 percent increase in average OEC, partially offset by the impact of COVID-19 that began in mid-March. Rental gross margin decreased by 60 basis points to 41.6%, primarily due to certain operating costs that, largely due to COVID-19, increased as a percentage of revenue.

- Cash flow from operating activities decreased 3.4% to $644 million for the first quarter, and free cash flow5, including aggregated merger and restructuring payments, increased 5.4% to $606 million. The increase in free cash flow was primarily due to decreased net rental capital expenditures (purchases of rental equipment less proceeds from sales of rental equipment), partially offset by lower net cash from operating activities. Net rental capital expenditures decreased $65 million year-over-year, reflecting reduced purchases of rental equipment partially offset by increased proceeds from the sales of rental equipment.

_______________

- Adjusted EPS (earnings per share) and adjusted EBITDA (earnings before interest, taxes, depreciation and amortization) are non-GAAP measures as defined in the tables below. See the tables below for amounts and reconciliations to the most comparable GAAP measures. Adjusted EBITDA margin represents adjusted EBITDA divided by total revenue.

- Rental revenue includes owned equipment rental revenue, re-rent revenue and ancillary revenue.

- Fleet productivity reflects the combined impact of changes in rental rates, time utilization and mix on owned equipment rental revenue. See the table below for more information.

- Used equipment sales adjusted gross margin excludes the impact of the fair value mark-up of acquired RSC, NES, Neff and BlueLine fleet that was sold.

- Free cash flow is a non-GAAP measure. See the table below for amounts and a reconciliation to the most comparable GAAP measure.

- Capital management in the quarter aligned with the company’s plan announced in June 2019, when the target leverage range was lowered to 2.0x-3.0x, from 2.5x-3.5x. The net leverage ratio was 2.5x at March 31, 2020, as compared to 2.6x at December 31, 2019. Year-to-date, the company has reduced its total net debt by $292 million and repurchased approximately $257 million of common stock under its current $500 million repurchase program, reducing the diluted share count by 0.7%. Further repurchases under the program have been paused, due to the COVID-19 pandemic, while the company assesses available sources and anticipated uses of cash.

- Total liquidity was $3.083 billion as of March 31, 2020, including $513 million of cash and cash equivalents, an increase of $940 million from December 31, 2019. Notably, the company has no long-term debt maturities until 2025.

- Return on invested capital (ROIC) was 10.3% for the 12 months ended March 31, 2020, compared with 10.9% for the 12 months ended March 31, 2019. ROIC exceeded the company’s current weighted average cost of capital of less than 8.0%. The company’s ROIC metric uses after-tax operating income for the trailing 12 months divided by average stockholders’ equity, debt and deferred taxes, net of average cash. To mitigate the volatility related to fluctuations in the company’s tax rate from period to period, the U.S. federal corporate statutory tax rate of 21% was used to calculate after-tax operating income.

Withdrawal of Full-Year 2020 Guidance

The operational and financial impacts on the company from the continuing, severe economic disruption caused by COVID-19 are uncertain at this time. As a result, the company has withdrawn its full-year 2020 financial guidance. The company will continue to assess the impact of COVID-19 on the company’s operations and will next provide guidance when it can reasonably estimate the pandemic’s impact on its business.

Share Repurchase Program

On January 28, 2020, the company's Board of Directors authorized a new $500 million share repurchase program. Through March 18, 2020, when the program was paused due to the COVID-19 pandemic, the company repurchased $257 million of common stock. At this time, the company is unable to estimate when, or if, the program will be restarted, and expects to provide an update at a future date.

Conference Call

United Rentals will hold a conference call tomorrow, Thursday, April 30, 2020, at 11:00 a.m. Eastern Time. The conference call number is 855-458-4217 (international: 574-990-3618). The conference call will also be available live by audio webcast at unitedrentals.com, where it will be archived until the next earnings call. The replay number for the call is 404-537-3406, passcode is 1984473.

Non-GAAP Measures

Free cash flow, earnings before interest, taxes, depreciation and amortization (EBITDA), adjusted EBITDA, and adjusted earnings per share (adjusted EPS) are non-GAAP financial measures as defined under the rules of the SEC. Free cash flow represents net cash provided by operating activities less purchases of, and plus proceeds from, equipment. The equipment purchases and proceeds represent cash flows from investing activities. EBITDA represents the sum of net income, provision for income taxes, interest expense, net, depreciation of rental equipment and non-rental depreciation and amortization. Adjusted EBITDA represents EBITDA plus the sum of the merger related costs, restructuring charge, stock compensation expense, net, and the impact of the fair value mark-up of acquired fleet. Adjusted EPS represents EPS plus the sum of the merger related costs, restructuring charge, the impact on depreciation related to acquired fleet and property and equipment, the impact of the fair value mark-up of acquired fleet, merger related intangible asset amortization and asset impairment charge. The company believes that: (i) free cash flow provides useful additional information concerning cash flow available to meet future debt service obligations and working capital requirements; (ii) EBITDA and adjusted EBITDA provide useful information about operating performance and period-over-period growth, and help investors gain an understanding of the factors and trends affecting our ongoing cash earnings, from which capital investments are made and debt is serviced; and (iii) adjusted EPS provides useful information concerning future profitability. However, none of these measures should be considered as alternatives to net income, cash flows from operating activities or earnings per share under GAAP as indicators of operating performance or liquidity.

About United Rentals

United Rentals, Inc. is the largest equipment rental company in the world. The company has an integrated network of 1,170 rental locations in North America and 11 in Europe. In North America, the company operates in 49 states and every Canadian province. The company’s approximately 19,300 employees serve construction and industrial customers, utilities, municipalities, homeowners and others. The company offers approximately 4,000 classes of equipment for rent with a total original cost of $14.32 billion. United Rentals is a member of the Standard & Poor’s 500 Index, the Barron’s 400 Index and the Russell 3000 Index® and is headquartered in Stamford, Conn. Additional information about United Rentals is available at unitedrentals.com.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995, known as the PSLRA. These statements can generally be identified by the use of forward-looking terminology such as “believe,” “expect,” “may,” “will,” “should,” “seek,” “on-track,” “plan,” “project,” “forecast,” “intend” or “anticipate,” or the negative thereof or comparable terminology, or by discussions of vision, strategy or outlook. These statements are based on current plans, estimates and projections, and, therefore, you should not place undue reliance on them. No forward-looking statement can be guaranteed, and actual results may differ materially from those projected. Factors that could cause actual results to differ materially from those projected include, but are not limited to, the following: (1) uncertainty regarding the length of time it will take for the United States and the rest of the world to slow the spread of the novel strain of coronavirus (COVID-19) to the point where applicable governmental authorities are comfortable easing current “social distancing” policies, which have required closing many businesses deemed “non-essential”; such restrictions are designed to protect public health but also have the effect of significantly reducing demand for equipment rentals; (2) the extent to which businesses in and associated with the construction industry, including equipment rental service providers such as us, continue to be deemed “essential” for the purposes of “social distancing” policies in the regions in which we operate; (3) the impact of global economic conditions (including potential trade wars) and public health crises and epidemics, such as COVID-19, on us, our customers and our suppliers, in the United States and the rest of the world; (4) the possibility that companies that we have acquired or may acquire, including BakerCorp and BlueLine, could have undiscovered liabilities or involve other unexpected costs, may strain our management capabilities or may be difficult to integrate; (5) the cyclical nature of our business, which is highly sensitive to North American construction and industrial activities; if construction or industrial activity decline, our revenues and, because many of our costs are fixed, our profitability may be adversely affected; (6) our significant indebtedness, which requires us to use a substantial portion of our cash flow for debt service and can constrain our flexibility in responding to unanticipated or adverse business conditions; (7) the inability to refinance our indebtedness on terms that are favorable to us (including as a result of current volatility and uncertainty in capital markets due to COVID-19), or at all; (8) the incurrence of additional debt, which could exacerbate the risks associated with our current level of indebtedness; (9) noncompliance with financial or other covenants in our debt agreements, which could result in our lenders terminating the agreements and requiring us to repay outstanding borrowings; (10) restrictive covenants and amount of borrowings permitted in our debt instruments, which can limit our financial and operational flexibility; (11) overcapacity of fleet in the equipment rental industry, including as a result of reduced demand for fleet due to the impacts of COVID-19 on our customers; (12) inability to benefit from government spending, including spending associated with infrastructure projects; (13) fluctuations in the price of our common stock and inability to complete stock repurchases in the time frame and/or on the terms anticipated (for example, due to COVID-19); (14) rates we charge and time utilization we achieve being less than anticipated (including as a result of COVID-19); (15) inability to manage credit risk adequately or to collect on contracts with a large number of customers; (16) inability to access the capital that our businesses or growth plans may require (including as a result of uncertainty in capital markets due to COVID-19); (17) the incurrence of impairment charges; (18) trends in oil and natural gas could adversely affect the demand for our services and products; (19) the fact that our holding company structure requires us to depend in part on distributions from subsidiaries and such distributions could be limited by contractual or legal restrictions; (20) increases in our loss reserves to address business operations or other claims and any claims that exceed our established levels of reserves; (21) incurrence of additional expenses (including indemnification obligations) and other costs in connection with litigation, regulatory and investigatory matters; (22) the outcome or other potential consequences of regulatory matters and commercial litigation; (23) shortfalls in our insurance coverage; (24) our charter provisions as well as provisions of certain debt agreements and our significant indebtedness may have the effect of making more difficult or otherwise discouraging, delaying or deterring a takeover or other change of control of us; (25) turnover in our management team and inability to attract and retain key personnel, as well as loss, absenteeism or the inability of employees to work or perform key functions in light of public health crises or epidemics (including COVID-19); (26) costs we incur being more than anticipated and the inability to realize expected savings in the amounts or time frames planned; (27) our dependence on key suppliers to obtain equipment and other supplies for our business on acceptable terms; (28) inability to sell our new or used fleet in the amounts, or at the prices, we expect; (29) competition from existing and new competitors; (30) risks related to security breaches, cybersecurity attacks, failure to protect personal information, compliance with data protection laws and other significant disruptions in our information technology systems; (31) the costs of complying with environmental, safety and foreign laws and regulations, as well as other risks associated with non-U.S. operations, including currency exchange risk (including as a result of Brexit), and tariffs; (32) labor disputes, work stoppages or other labor difficulties, which may impact our productivity, and potential enactment of new legislation or other changes in law affecting our labor relations and operations generally; (33) increases in our maintenance and replacement costs and/or decreases in the residual value of our equipment; and (34) the effect of changes in tax law. For a more complete description of these and other possible risks and uncertainties, please refer to our Annual Report on Form 10-K for the year ended December 31, 2019, as well as to our subsequent filings with the SEC. The forward-looking statements contained herein speak only as of the date hereof, and we make no commitment to update or publicly release any revisions to forward-looking statements in order to reflect new information or subsequent events, circumstances or changes in expectations.

UNITED RENTALS, INC. CONDENSED CONSOLIDATED STATEMENTS OF INCOME (UNAUDITED) (In millions, except per share amounts) | |||||||

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Revenues: | |||||||

Equipment rentals | $ | 1,783 | $ | 1,795 | |||

Sales of rental equipment | 208 | 192 | |||||

Sales of new equipment | 62 | 62 | |||||

Contractor supplies sales | 25 | 24 | |||||

Service and other revenues | 47 | 44 | |||||

Total revenues | 2,125 | 2,117 | |||||

Cost of revenues: | |||||||

Cost of equipment rentals, excluding depreciation | 747 | 742 | |||||

Depreciation of rental equipment | 426 | 395 | |||||

Cost of rental equipment sales | 125 | 125 | |||||

Cost of new equipment sales | 54 | 54 | |||||

Cost of contractor supplies sales | 18 | 17 | |||||

Cost of service and other revenues | 28 | 23 | |||||

Total cost of revenues | 1,398 | 1,356 | |||||

Gross profit | 727 | 761 | |||||

Selling, general and administrative expenses | 267 | 280 | |||||

Merger related costs | — | 1 | |||||

Restructuring charge | 2 | 8 | |||||

Non-rental depreciation and amortization | 100 | 104 | |||||

Operating income | 358 | 368 | |||||

Interest expense, net | 136 | 151 | |||||

Other income, net | (4 | ) | (3 | ) | |||

Income before provision for income taxes | 226 | 220 | |||||

Provision for income taxes | 53 | 45 | |||||

Net income | $ | 173 | $ | 175 | |||

Diluted earnings per share | $ | 2.33 | $ | 2.19 | |||

UNITED RENTALS, INC. CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED) (In millions) | |||||||

March 31, 2020 | December 31, 2019 | ||||||

ASSETS | |||||||

Cash and cash equivalents | $ | 513 | $ | 52 | |||

Accounts receivable, net | 1,413 | 1,530 | |||||

Inventory | 115 | 120 | |||||

Prepaid expenses and other assets | 173 | 140 | |||||

Total current assets | 2,214 | 1,842 | |||||

Rental equipment, net | 9,422 | 9,787 | |||||

Property and equipment, net | 600 | 604 | |||||

Goodwill | 5,122 | 5,154 | |||||

Other intangible assets, net | 823 | 895 | |||||

Operating lease right-of-use assets | 666 | 669 | |||||

Other long-term assets | 21 | 19 | |||||

Total assets | $ | 18,868 | $ | 18,970 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

Short-term debt and current maturities of long-term debt | $ | 854 | $ | 997 | |||

Accounts payable | 484 | 454 | |||||

Accrued expenses and other liabilities | 658 | 747 | |||||

Total current liabilities | 1,996 | 2,198 | |||||

Long-term debt | 10,743 | 10,431 | |||||

Deferred taxes | 1,878 | 1,887 | |||||

Operating lease liabilities | 530 | 533 | |||||

Other long-term liabilities | 86 | 91 | |||||

Total liabilities | 15,233 | 15,140 | |||||

Common stock | 1 | 1 | |||||

Additional paid-in capital | 2,435 | 2,440 | |||||

Retained earnings | 5,448 | 5,275 | |||||

Treasury stock | (3,957 | ) | (3,700 | ) | |||

Accumulated other comprehensive loss | (292 | ) | (186 | ) | |||

Total stockholders’ equity | 3,635 | 3,830 | |||||

Total liabilities and stockholders’ equity | $ | 18,868 | $ | 18,970 | |||

UNITED RENTALS, INC. CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) (In millions) | |||||||

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Cash Flows From Operating Activities: | |||||||

Net income | $ | 173 | $ | 175 | |||

Adjustments to reconcile net income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 526 | 499 | |||||

Amortization of deferred financing costs and original issue discounts | 4 | 4 | |||||

Gain on sales of rental equipment | (83 | ) | (67 | ) | |||

Gain on sales of non-rental equipment | (1 | ) | (2 | ) | |||

Gain on insurance proceeds from damaged equipment | (6 | ) | (7 | ) | |||

Stock compensation expense, net | 13 | 15 | |||||

Merger related costs | — | 1 | |||||

Restructuring charge | 2 | 8 | |||||

Increase in deferred taxes | 1 | 21 | |||||

Changes in operating assets and liabilities: | |||||||

Decrease in accounts receivable | 105 | 73 | |||||

Decrease (increase) in inventory | 5 | (9 | ) | ||||

(Increase) decrease in prepaid expenses and other assets | (30 | ) | 12 | ||||

Increase in accounts payable | 33 | 18 | |||||

Decrease in accrued expenses and other liabilities | (98 | ) | (74 | ) | |||

Net cash provided by operating activities | 644 | 667 | |||||

Cash Flows From Investing Activities: | |||||||

Purchases of rental equipment | (208 | ) | (257 | ) | |||

Purchases of non-rental equipment | (53 | ) | (42 | ) | |||

Proceeds from sales of rental equipment | 208 | 192 | |||||

Proceeds from sales of non-rental equipment | 9 | 8 | |||||

Insurance proceeds from damaged equipment | 6 | 7 | |||||

Purchases of other companies, net of cash acquired | — | (173 | ) | ||||

Purchases of investments | (1 | ) | — | ||||

Net cash used in investing activities | (39 | ) | (265 | ) | |||

Cash Flows From Financing Activities: | |||||||

Proceeds from debt | 2,517 | 1,427 | |||||

Payments of debt | (2,375 | ) | (1,572 | ) | |||

Payments of financing costs | (9 | ) | (9 | ) | |||

Proceeds from the exercise of common stock options | 1 | 4 | |||||

Common stock repurchased (1) | (276 | ) | (243 | ) | |||

Net cash used in financing activities | (142 | ) | (393 | ) | |||

Effect of foreign exchange rates | (2 | ) | — | ||||

Net increase in cash and cash equivalents | 461 | 9 | |||||

Cash and cash equivalents at beginning of period | 52 | 43 | |||||

Cash and cash equivalents at end of period | $ | 513 | $ | 52 | |||

Supplemental disclosure of cash flow information: | |||||||

Cash paid for income taxes, net | $ | 3 | $ | 4 | |||

Cash paid for interest | 174 | 179 | |||||

| (1) | We have an open $500 million share repurchase program that commenced in 2020. As discussed above, we have decided to pause repurchases under the program, due to the COVID-19 pandemic, while we assess our available sources and anticipated uses of cash. At this time, we are unable to estimate when, or if, the program will be restarted, and expect to provide an update at a future date. |

UNITED RENTALS, INC.

RENTAL REVENUE

Fleet productivity is a comprehensive metric that provides greater insight into the decisions made by our managers in support of growth and returns. Specifically, we seek to optimize the interplay of rental rates, time utilization and mix in driving rental revenue. Fleet productivity aggregates, in one metric, the impact of changes in rates, utilization and mix on owned equipment rental revenue.

We believe that this metric is useful in assessing the effectiveness of our decisions on rates, time utilization and mix, particularly as they support the creation of shareholder value. The table below shows the components of the year-over-year change in rental revenue using the fleet productivity methodology:

Year-over-

| Assumed year-

| Fleet

| Contribution

| Total

| |||||

Three Months Ended March 31, 2020 | 2.2% | (1.5)% | (1.2)% | (0.2)% | (0.7)% |

Please refer to our First Quarter 2019 Investor Presentation for additional detail on fleet productivity.

| (1) | Reflects the estimated impact of inflation on the revenue productivity of fleet based on OEC, which is recorded at cost. |

| (2) | Reflects the combined impact of changes in rental rates, time utilization and mix on owned equipment rental revenue. Changes in customers, fleet, geographies and segments all contribute to changes in mix. |

| (3) | Reflects the combined impact of changes in other types of equipment rental revenue: ancillary and re-rent (excludes owned equipment rental revenue). |

UNITED RENTALS, INC. SEGMENT PERFORMANCE ($ in millions) | |||||

Three Months Ended | |||||

March 31, | |||||

2020 | 2019 | Change | |||

General Rentals | |||||

Reportable segment equipment rentals revenue | $1,394 | $1,423 | (2.0)% | ||

Reportable segment equipment rentals gross profit | 448 | 501 | (10.6)% | ||

Reportable segment equipment rentals gross margin | 32.1% | 35.2% | (310) bps | ||

Trench, Power and Fluid Solutions | |||||

Reportable segment equipment rentals revenue | $389 | $372 | 4.6% | ||

Reportable segment equipment rentals gross profit | 162 | 157 | 3.2% | ||

Reportable segment equipment rentals gross margin | 41.6% | 42.2% | (60) bps | ||

Total United Rentals | |||||

Total equipment rentals revenue | $1,783 | $1,795 | (0.7)% | ||

Total equipment rentals gross profit | 610 | 658 | (7.3)% | ||

Total equipment rentals gross margin | 34.2% | 36.7% | (250) bps | ||

UNITED RENTALS, INC. DILUTED EARNINGS PER SHARE CALCULATION (In millions, except per share data) | |||||||

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Numerator: | |||||||

Net income available to common stockholders | $ | 173 | $ | 175 | |||

Denominator: | |||||||

Denominator for basic earnings per share—weighted-average common shares | 74.0 | 79.4 | |||||

Effect of dilutive securities: | |||||||

Employee stock options | — | 0.3 | |||||

Restricted stock units | 0.3 | 0.3 | |||||

Denominator for diluted earnings per share—adjusted weighted-average common shares | 74.3 | 80.0 | |||||

Diluted earnings per share | $ | 2.33 | $ | 2.19 | |||

UNITED RENTALS, INC.

ADJUSTED EARNINGS PER SHARE GAAP RECONCILIATION

We define “earnings per share – adjusted” as the sum of earnings per share – GAAP, as-reported plus the impact of the following special items: merger related costs, merger related intangible asset amortization, impact on depreciation related to acquired fleet and property and equipment, impact of the fair value mark-up of acquired fleet, restructuring charge and asset impairment charge. Management believes that earnings per share - adjusted provides useful information concerning future profitability. However, earnings per share - adjusted is not a measure of financial performance under GAAP. Accordingly, earnings per share - adjusted should not be considered an alternative to GAAP earnings per share. The table below provides a reconciliation between earnings per share – GAAP, as-reported, and earnings per share – adjusted.

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Earnings per share - GAAP, as-reported | $ | 2.33 | $ | 2.19 | |||

After-tax impact of: | |||||||

Merger related costs (2) | — | 0.01 | |||||

Merger related intangible asset amortization (3) | 0.59 | 0.64 | |||||

Impact on depreciation related to acquired fleet and property and equipment (4) | 0.03 | 0.14 | |||||

Impact of the fair value mark-up of acquired fleet (5) | 0.12 | 0.25 | |||||

Restructuring charge (6) | 0.02 | 0.07 | |||||

Asset impairment charge (7) | 0.26 | 0.01 | |||||

Earnings per share - adjusted | $ | 3.35 | $ | 3.31 | |||

Tax rate applied to above adjustments (1) | 25.2 | % | 25.4 | % | |||

(1) | The tax rates applied to the adjustments reflect the statutory rates in the applicable entities. | |

(2) | Reflects transaction costs associated with the BakerCorp International Holdings, Inc. (“BakerCorp”) and BlueLine acquisitions that were completed in 2018. We have made a number of acquisitions in the past and may continue to make acquisitions in the future. Merger related costs only include costs associated with major acquisitions that significantly impact our operations. The acquisitions that have included merger related costs are RSC, which had annual revenues of approximately $1.5 billion prior to the acquisition, National Pump, which had annual revenues of over $200 million prior to the acquisition, NES, which had annual revenues of approximately $369 million prior to the acquisition, Neff, which had annual revenues of approximately $413 million prior to the acquisition, BakerCorp, which had annual revenues of approximately $295 million prior to the acquisition and BlueLine, which had annual revenues of approximately $786 million prior to the acquisition. | |

(3) | Reflects the amortization of the intangible assets acquired in the RSC, National Pump, NES, Neff, BakerCorp and BlueLine acquisitions. | |

(4) | Reflects the impact of extending the useful lives of equipment acquired in the RSC, NES, Neff, BakerCorp and BlueLine acquisitions, net of the impact of additional depreciation associated with the fair value mark-up of such equipment. | |

(5) | Reflects additional costs recorded in cost of rental equipment sales associated with the fair value mark-up of rental equipment acquired in the RSC, NES, Neff and BlueLine acquisitions and subsequently sold. | |

(6) | Primarily reflects severance and branch closure charges associated with our closed restructuring programs and our current restructuring program. We only include such costs that are part of a restructuring program as restructuring charges. Since the first such restructuring program was initiated in 2008, we have completed five restructuring programs. We have cumulatively incurred total restructuring charges of $335 million under our restructuring programs. | |

(7) | Reflects write-offs of leasehold improvements and other fixed assets. 2020 includes a $26 million asset impairment charge, which was not related to COVID-19, primarily associated with the discontinuation of certain equipment programs. |

UNITED RENTALS, INC.

EBITDA AND ADJUSTED EBITDA GAAP RECONCILIATIONS

(In millions)

EBITDA represents the sum of net income, provision for income taxes, interest expense, net, depreciation of rental equipment, and non-rental depreciation and amortization. Adjusted EBITDA represents EBITDA plus the sum of the merger related costs, restructuring charge, stock compensation expense, net, and the impact of the fair value mark-up of acquired fleet. These items are excluded from adjusted EBITDA internally when evaluating our operating performance and for strategic planning and forecasting purposes, and allow investors to make a more meaningful comparison between our core business operating results over different periods of time, as well as with those of other similar companies. The EBITDA and adjusted EBITDA margins represent EBITDA or adjusted EBITDA divided by total revenue. Management believes that EBITDA and adjusted EBITDA, when viewed with the Company’s results under GAAP and the accompanying reconciliation, provide useful information about operating performance and period-over-period growth, and provide additional information that is useful for evaluating the operating performance of our core business without regard to potential distortions. Additionally, management believes that EBITDA and adjusted EBITDA help investors gain an understanding of the factors and trends affecting our ongoing cash earnings, from which capital investments are made and debt is serviced.

The table below provides a reconciliation between net income and EBITDA and adjusted EBITDA.

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Net income | $ | 173 | $ | 175 | |||

Provision for income taxes | 53 | 45 | |||||

Interest expense, net | 136 | 151 | |||||

Depreciation of rental equipment | 426 | 395 | |||||

Non-rental depreciation and amortization | 100 | 104 | |||||

EBITDA (A) | $ | 888 | $ | 870 | |||

Merger related costs (1) | — | 1 | |||||

Restructuring charge (2) | 2 | 8 | |||||

Stock compensation expense, net (3) | 13 | 15 | |||||

Impact of the fair value mark-up of acquired fleet (4) | 12 | 27 | |||||

Adjusted EBITDA (B) | $ | 915 | $ | 921 | |||

A) Our EBITDA margin was 41.8% and 41.1% for the three months ended March 31, 2020 and 2019, respectively.

B) Our adjusted EBITDA margin was 43.1% and 43.5% for the three months ended March 31, 2020 and 2019, respectively.

(1) | Reflects transaction costs associated with the BakerCorp and BlueLine acquisitions that were completed in 2018. We have made a number of acquisitions in the past and may continue to make acquisitions in the future. Merger related costs only include costs associated with major acquisitions that significantly impact our operations. The acquisitions that have included merger related costs are RSC, which had annual revenues of approximately $1.5 billion prior to the acquisition, National Pump, which had annual revenues of over $200 million prior to the acquisition, NES, which had annual revenues of approximately $369 million prior to the acquisition, Neff, which had annual revenues of approximately $413 million prior to the acquisition, BakerCorp, which had annual revenues of approximately $295 million prior to the acquisition and BlueLine, which had annual revenues of approximately $786 million prior to the acquisition. | ||

(2) | Primarily reflects severance and branch closure charges associated with our closed restructuring programs and our current restructuring program. We only include such costs that are part of a restructuring program as restructuring charges. Since the first such restructuring program was initiated in 2008, we have completed five restructuring programs. We have cumulatively incurred total restructuring charges of $335 million under our restructuring programs. | ||

(3) | Represents non-cash, share-based payments associated with the granting of equity instruments. | ||

(4) | Reflects additional costs recorded in cost of rental equipment sales associated with the fair value mark-up of rental equipment acquired in the RSC, NES, Neff and BlueLine acquisitions and subsequently sold. |

UNITED RENTALS, INC.

EBITDA AND ADJUSTED EBITDA GAAP RECONCILIATIONS (continued)

(In millions)

The table below provides a reconciliation between net cash provided by operating activities and EBITDA and adjusted EBITDA.

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Net cash provided by operating activities | $ | 644 | $ | 667 | |||

Adjustments for items included in net cash provided by operating activities but excluded from the calculation of EBITDA: | |||||||

Amortization of deferred financing costs and original issue discounts | (4 | ) | (4 | ) | |||

Gain on sales of rental equipment | 83 | 67 | |||||

Gain on sales of non-rental equipment | 1 | 2 | |||||

Gain on insurance proceeds from damaged equipment | 6 | 7 | |||||

Merger related costs (1) | — | (1 | ) | ||||

Restructuring charge (2) | (2 | ) | (8 | ) | |||

Stock compensation expense, net (3) | (13 | ) | (15 | ) | |||

Changes in assets and liabilities | (4 | ) | (28 | ) | |||

Cash paid for interest | 174 | 179 | |||||

Cash paid for income taxes, net | 3 | 4 | |||||

EBITDA | $ | 888 | $ | 870 | |||

Add back: | |||||||

Merger related costs (1) | — | 1 | |||||

Restructuring charge (2) | 2 | 8 | |||||

Stock compensation expense, net (3) | 13 | 15 | |||||

Impact of the fair value mark-up of acquired fleet (4) | 12 | 27 | |||||

Adjusted EBITDA | $ | 915 | $ | 921 | |||

(1) | Reflects transaction costs associated with the BakerCorp and BlueLine acquisitions that were completed in 2018. We have made a number of acquisitions in the past and may continue to make acquisitions in the future. Merger related costs only include costs associated with major acquisitions that significantly impact our operations. The acquisitions that have included merger related costs are RSC, which had annual revenues of approximately $1.5 billion prior to the acquisition, National Pump, which had annual revenues of over $200 million prior to the acquisition, NES, which had annual revenues of approximately $369 million prior to the acquisition, Neff, which had annual revenues of approximately $413 million prior to the acquisition, BakerCorp, which had annual revenues of approximately $295 million prior to the acquisition and BlueLine, which had annual revenues of approximately $786 million prior to the acquisition. | |

(2) | Primarily reflects severance and branch closure charges associated with our closed restructuring programs and our current restructuring program. We only include such costs that are part of a restructuring program as restructuring charges. Since the first such restructuring program was initiated in 2008, we have completed five restructuring programs. We have cumulatively incurred total restructuring charges of $335 million under our restructuring programs. | |

(3) | Represents non-cash, share-based payments associated with the granting of equity instruments. | |

(4) | Reflects additional costs recorded in cost of rental equipment sales associated with the fair value mark-up of rental equipment acquired in the RSC, NES, Neff and BlueLine acquisitions and subsequently sold. |

UNITED RENTALS, INC.

FREE CASH FLOW GAAP RECONCILIATION

(In millions)

We define “free cash flow” as net cash provided by operating activities less purchases of, and plus proceeds from, equipment. The equipment purchases and proceeds are included in cash flows from investing activities. Management believes that free cash flow provides useful additional information concerning cash flow available to meet future debt service obligations and working capital requirements. However, free cash flow is not a measure of financial performance or liquidity under GAAP. Accordingly, free cash flow should not be considered an alternative to net income or cash flow from operating activities as an indicator of operating performance or liquidity. The table below provides a reconciliation between net cash provided by operating activities and free cash flow.

Three Months Ended | |||||||

March 31, | |||||||

2020 | 2019 | ||||||

Net cash provided by operating activities | $ | 644 | $ | 667 | |||

Purchases of rental equipment | (208 | ) | (257 | ) | |||

Purchases of non-rental equipment | (53 | ) | (42 | ) | |||

Proceeds from sales of rental equipment | 208 | 192 | |||||

Proceeds from sales of non-rental equipment | 9 | 8 | |||||

Insurance proceeds from damaged equipment | 6 | 7 | |||||

Free cash flow (1) | $ | 606 | $ | 575 | |||

| (1) | Free cash flow included aggregate merger and restructuring related payments of $2 million and $8 million for the three months ended March 31, 2020 and 2019, respectively. |

View source version on businesswire.com: https://www.businesswire.com/news/home/20200429005845/en/

Contacts:

(203) 618-7122

Cell: (203) 399-8951

tgrace@ur.com